Select your investor profile:

This content is only for the selected type of investor.

Individual investors?

Hex Romana

Italy may have a government but the country's problems haven't gone away. That's a worry for the euro zone.

Written by

Andrea Delitala

Head of Multi Asset Euro

Luca Paolini

Chief Strategist

Italy has a new government. For now, crisis has been averted. But that doesn’t mean the political and market turmoil is over. Like a virus, the threat of a euro zone break-up triggered by Italy will linger for years to come. And this risk is likely to remain factored into asset prices.

With the agreement of a coalition between the populist Northern League and Five Star Alliance, the febrile mood that infected Italian politics and markets has suddenly cooled. Now that talk of anti-euro policies is no longer making headlines, investors are able to turn their focus back to some of Italy’s more positive fundamentals. After years of stagnation, the economy is growing at more than 1 per cent in inflation adjusted terms. The current account is showing a surplus of more than 2 per cent of GDP. As is the fiscal balance, once adjusted for the economic cycle and interest costs. Reforms to the labour market and other areas of the economy are being implemented.

Italy’s debt profile is also not quite as troubling as the headlines suggest. The average duration of Italian government’s liabilities has lengthened, while domestic investors hold the lion’s share of this debt.

Finally, membership of the euro is popular among Italians – the latest survey shows 70 per cent support.

Italy, then, is no Greece. But over the long run, that’s precisely its problem. It would be too big to save if its debts became unsustainable. And there remains a residual risk that the euro zone’s third largest economy will end up triggering a break-up of the euro – whether by design or accident.

In part that’s because the Italian economy is still uncompetitive relative to the single currency’s other big hitters. Italy also has among the lowest ratios of working age to total population of all major developed countries, at under 65 per cent compared to an average of 66.4 per cent for the OECD overall. And with a low birth-rate and ageing population – 21 per cent of Italians are over 65 – that proportion will only get worse. Italy has one of the world’s worst labour productivity rates and only Greece has lower GDP per hour worked in the OECD. Our fair value estimates suggest that were Italy to adopt a new, floating currency, it would immediately have to devalue by up to 30 per cent to regain lost competitiveness.

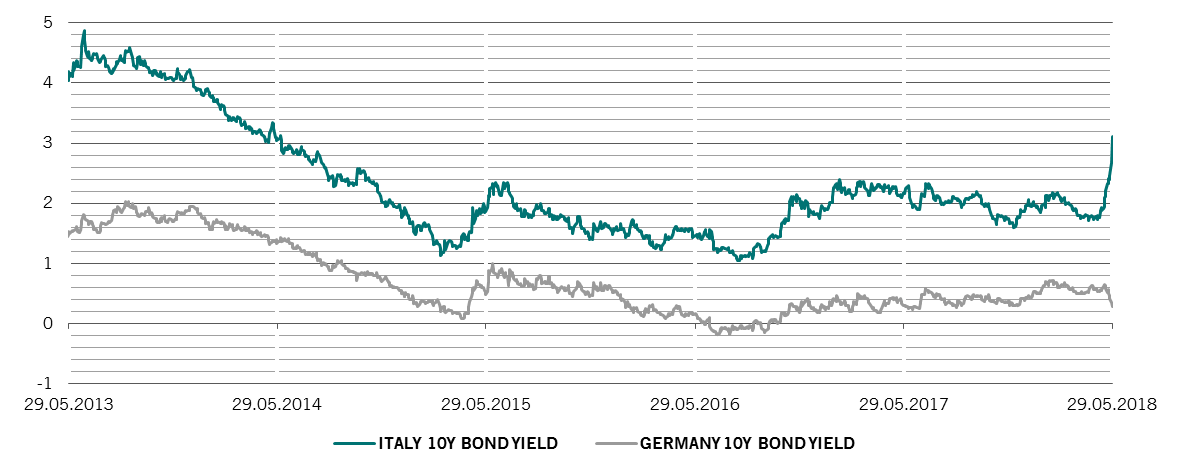

spreading fear

Italian and German 10-year government bond yields, %

Meanwhile, the rise of populism has in large part been a reaction to a flood of migrants and asylum seekers from Africa and the Levant.

These factors are likely to set Italy’s new government on a collision course with the European Commission. With domestic growth prospects relatively poor, it wants to pump the economy with a big fiscal spending programme, which means government budget deficits.The latest estimates are for an additional EUR120bn of spending, which is around 7 per cent of GDP.

This would necessitate EC approval – which is unlikely to be forthcoming given that Italy already has Europe’s highest debt to GDP ratio of over 130 per cent. Brussels – and most crucially Germany – is unlikely to tolerate deficits incompatible with the stability of Italy's debt to GDP ratio. Any drop in the country's primary surplus below around 0.6 per cent from the current 1.9 per cent is like to contravene the EU's fiscal compact. At the same time, the new Italian coalition will want the rest of the EU to take a bigger share of the migrant burden. This too is likely to be fraught, not least because the likes of Germany have also tilted towards populism in response to their own immigration problems.

The upshot is that the market is unlikely to return to previous complacency. As recently as April, bond investors were assigning virtually zero risk to breakup of the euro zone. By May 29, the gap in yields between Italian government bonds (BTPs) and their German equivalents had widened to effectively discount a one in five chance that Italy would leave the euro, according to our proprietary model. That may still only have been half the 40 per cent probability reached during the 2011-12 crisis, but it was significant. And though it’s shrunk with the subsequent rally, the risk won’t disappear altogether – the current spread is just over 200 basis points, leaving the probability of Italiexit at around 5 per cent.

Because Italian banks, while well capitalised, have large holdings of Italian government bonds, even this gauge might underestimate the potential for euro zone fragmentation. According to the Bank for International Settlements, BTPs account for 20 per cent of Italian bank assets. That’s among the highest levels in the world.

Our estimates suggest that every 100 basis point widening in the BTP/Bund yield spread reduces Italian banks’ capital by 30 basis points. A 300 basis point widening could begin to cause the sector serious discomfort, not least because sovereign bond losses could spark deposit outflows and make it difficult for banks to sell on non-performing loans.

Whatever happens, a lasting Pax Romana seems unlikely.

related articles

The case for a Swiss defence

Why Switzerland's equities could benefit if the cyclical stock rally runs out of steam

May 2018

Protectionism populism and despots: why investing just got harder

How political upheaval in the US Italy and China could redraw the economic and investment landscape.

March 2018

Important legal information

This marketing material is issued by Pictet Asset Management (Europe) S.A.. It is neither directed to, nor intended for distribution or use by, any person or entity who is a citizen or resident of, or domiciled or located in, any locality, state, country or jurisdiction where such distribution, publication, availability or use would be contrary to law or regulation. The latest version of the fund‘s prospectus, Pre-Contractual Template (PCT) when applicable, Key Information Document (KID), annual and semi-annual reports must be read before investing. They are available free of charge in English on www.assetmanagement.pictet or in paper copy at Pictet Asset Management (Europe) S.A., 6B, rue du Fort Niedergruenewald, L-2226 Luxembourg, or at the office of the fund local agent, distributor or centralizing agent if any.

The KID is also available in the local language of each country where the compartment is registered. The prospectus, the PCT when applicable, and the annual and semi-annual reports may also be available in other languages, please refer to the website for other available languages. Only the latest version of these documents may be relied upon as the basis for investment decisions.

The summary of investor rights (in English and in the different languages of our website) is available here and at www.assetmanagement.pictet under the heading "Resources", at the bottom of the page.

The list of countries where the fund is registered can be obtained at all times from Pictet Asset Management (Europe) S.A., which may decide to terminate the arrangements made for the marketing of the fund or compartments of the fund in any given country.

The information and data presented in this document are not to be considered as an offer or solicitation to buy, sell or subscribe to any securities or financial instruments or services.

Information, opinions and estimates contained in this document reflect a judgment at the original date of publication and are subject to change without notice. The management company has not taken any steps to ensure that the securities referred to in this document are suitable for any particular investor and this document is not to be relied upon in substitution for the exercise of independent judgment. Tax treatment depends on the individual circumstances of each investor and may be subject to change in the future. Before making any investment decision, investors are recommended to ascertain if this investment is suitable for them in light of their financial knowledge and experience, investment goals and financial situation, or to obtain specific advice from an industry professional.

The value and income of any of the securities or financial instruments mentioned in this document may fall as well as rise and, as a consequence, investors may receive back less than originally invested.

The investment guidelines are internal guidelines which are subject to change at any time and without any notice within the limits of the fund's prospectus. The mentioned financial instruments are provided for illustrative purposes only and shall not be considered as a direct offering, investment recommendation or investment advice. Reference to a specific security is not a recommendation to buy or sell that security. Effective allocations are subject to change and may have changed since the date of the marketing material.

Past performance is not a guarantee or a reliable indicator of future performance. Performance data does not include the commissions and fees charged at the time of subscribing for or redeeming shares.

Any index data referenced herein remains the property of the Data Vendor. Data Vendor Disclaimers are available on assetmanagement.pictet in the “Resources” section of the footer. This document is a marketing communication issued by Pictet Asset Management and is not in scope for any MiFID II/MiFIR requirements specifically related to investment research. This material does not contain sufficient information to support an investment decision and it should not be relied upon by you in evaluating the merits of investing in any products or services offered or distributed by Pictet Asset Management.

Pictet AM has not acquired any rights or license to reproduce the trademarks, logos or images set out in this document except that it holds the rights to use any entity of the Pictet group trademarks. For illustrative purposes only.