Select your investor profile:

This content is only for the selected type of investor.

Individual investors?

Bund yields don't herald another Japan

Bund yields have hit new lows. But this doesn't mean Germany is turning Japanese.

Written by

Luca Paolini

Chief Strategist

Germany isn't turning Japanese. Which is why the relentless decline in German government bond yields is unjustified.

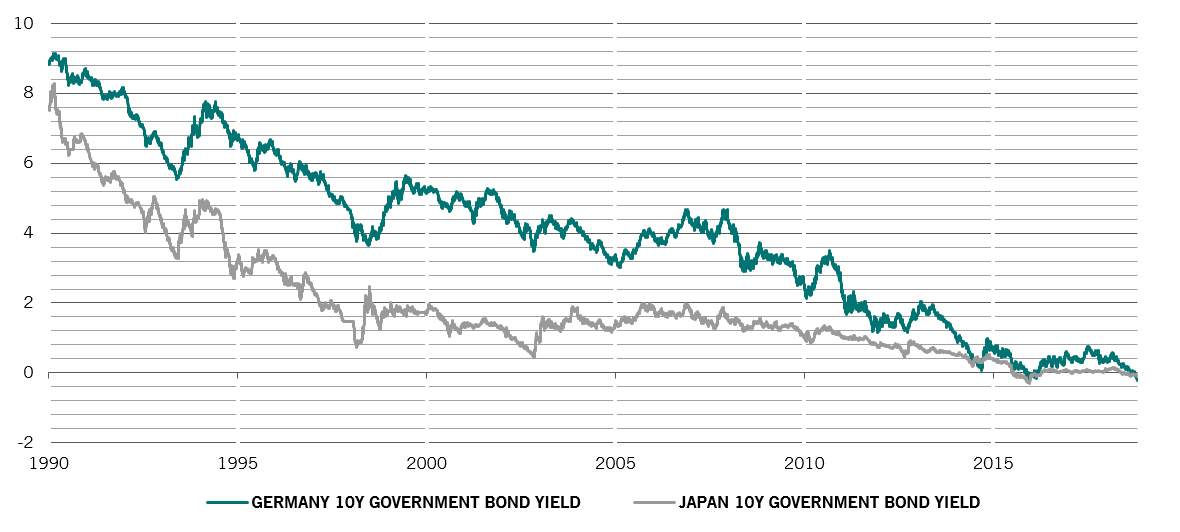

The yield on 10-year bunds – German government bonds – fell to an all-time low of -0.21 per cent on the last day of May as global markets panicked about US President Donald Trump’s threat to impose tariffs on Mexico. The flight to safety boosted most safe haven assets – US Treasury bonds, Japanese government bonds (JGBs) and gold also rallied.

But the move in bunds was particularly eye-catching, not least because 10-year yields are below their JGB equivalents.

Nor is the German bond market’s strength just a recent phenomenon. During the past decade, 10-year bunds have generated annual returns of around 6 per cent, while 30-year bonds have delivered 11 per cent, against around 10 per cent returns from the German equity market.

All of which makes it unsurprising that investors are increasingly wondering whether bunds have turned Japanese, a crucial question when one considers that over the past 30 years Japanese bonds have outperformed Japanese equities by more than 4 per cent a year, for a cumulative 250 per cent.

Japan’s decades of lacklustre growth, chronic deflation and policymakers’ efforts at jump-starting the economy with quantitative easing underpinned domestic demand for its bonds.

crossing over

10-year German and Japanese government bond yields, %

But Germany is very different from Japan of the 1990s. It hasn’t seen a bubble in either financial markets nor property prices; its exchange rate is not overvalued; Germany’s bank lending growth is running at a respectable pace of more than 3 per cent, as opposed to Japan’s which contracted by 30 per cent over the decade to 2005; Germany is experiencing 3 per cent wage inflation compared to Japan’s decade of deflating wages; and the necessity to preserve the monetary union has resulted in a very accommodative monetary policy for Germany. By the same token, though it’s hard to see where the next boost for bunds is likely to come from. The market doesn’t expect the European Central Bank to raise rates until 2022 at the earliest.

Bund yields have fallen not because of weak growth but because of a flight to safety from debt-ridden peripheral European economies. Indeed, that’s particularly relevant given that bond yields tend to move in line with nominal GDP growth over the long run. On that measure, bunds are trading at a record 3 percentage points below trend GDP growth, whereas until 2013, JGB yields were above Japan’s growth rate.

It’s true that there are some similarities Germany now with Japan of the 1990s – poor demographics; large current account surplus; the wrong economic paradigm (“fiscal brake” for Germany, “strong yen” for Japan); excess dependence on exports and too great a focus on producing cars and other capital goods. But they still do not justify how far bund yields have fallen.

As a result, bunds have become the most expensive of all major asset classes, with yields standing at 240 basis points below US Treasury bonds and 100 basis points below what appears justified by Germany’s nominal GDP growth. At the same time technicals show that bunds are significantly overbought based on reliable historic metrics.

This is why our strategy unit is underweight euro zone government bonds and why it makes sense to look elsewhere for a fixed income allocation, including US Treasury bonds.

related articles

War and no peace

The effects of a full-scale trade war will extend far beyond the US and China threatening stagflation worldwide.

May 2019

Bad omen: what the yield curve says about stocks

The inversion of the US yield curve strengthens the bear case for the economy and stock markets.

August 2019

Important legal information

This marketing material is issued by Pictet Asset Management (Europe) S.A.. It is neither directed to, nor intended for distribution or use by, any person or entity who is a citizen or resident of, or domiciled or located in, any locality, state, country or jurisdiction where such distribution, publication, availability or use would be contrary to law or regulation. The latest version of the fund‘s prospectus, Pre-Contractual Template (PCT) when applicable, Key Information Document (KID), annual and semi-annual reports must be read before investing. They are available free of charge in English on www.assetmanagement.pictet or in paper copy at Pictet Asset Management (Europe) S.A., 6B, rue du Fort Niedergruenewald, L-2226 Luxembourg, or at the office of the fund local agent, distributor or centralizing agent if any.

The KID is also available in the local language of each country where the compartment is registered. The prospectus, the PCT when applicable, and the annual and semi-annual reports may also be available in other languages, please refer to the website for other available languages. Only the latest version of these documents may be relied upon as the basis for investment decisions.

The summary of investor rights (in English and in the different languages of our website) is available here and at www.assetmanagement.pictet under the heading "Resources", at the bottom of the page.

The list of countries where the fund is registered can be obtained at all times from Pictet Asset Management (Europe) S.A., which may decide to terminate the arrangements made for the marketing of the fund or compartments of the fund in any given country.

The information and data presented in this document are not to be considered as an offer or solicitation to buy, sell or subscribe to any securities or financial instruments or services.

Information, opinions and estimates contained in this document reflect a judgment at the original date of publication and are subject to change without notice. The management company has not taken any steps to ensure that the securities referred to in this document are suitable for any particular investor and this document is not to be relied upon in substitution for the exercise of independent judgment. Tax treatment depends on the individual circumstances of each investor and may be subject to change in the future. Before making any investment decision, investors are recommended to ascertain if this investment is suitable for them in light of their financial knowledge and experience, investment goals and financial situation, or to obtain specific advice from an industry professional.

The value and income of any of the securities or financial instruments mentioned in this document may fall as well as rise and, as a consequence, investors may receive back less than originally invested.

The investment guidelines are internal guidelines which are subject to change at any time and without any notice within the limits of the fund's prospectus. The mentioned financial instruments are provided for illustrative purposes only and shall not be considered as a direct offering, investment recommendation or investment advice. Reference to a specific security is not a recommendation to buy or sell that security. Effective allocations are subject to change and may have changed since the date of the marketing material.

Past performance is not a guarantee or a reliable indicator of future performance. Performance data does not include the commissions and fees charged at the time of subscribing for or redeeming shares.

Any index data referenced herein remains the property of the Data Vendor. Data Vendor Disclaimers are available on assetmanagement.pictet in the “Resources” section of the footer. This document is a marketing communication issued by Pictet Asset Management and is not in scope for any MiFID II/MiFIR requirements specifically related to investment research. This material does not contain sufficient information to support an investment decision and it should not be relied upon by you in evaluating the merits of investing in any products or services offered or distributed by Pictet Asset Management.

Pictet AM has not acquired any rights or license to reproduce the trademarks, logos or images set out in this document except that it holds the rights to use any entity of the Pictet group trademarks. For illustrative purposes only.