Asset allocation: stimulus and vaccine offer enduring support

Economic growth has clearly slowed in recent months thanks in large part to the spread of the particularly infectious Delta variant of Covid. Still, with monetary stimulus in plentiful supply and vaccination rates holding firm, this dip could prove to be temporary.

Whether inflation will be transient is not so clear, however. So far, much of the increase in inflation results from distortions caused by changing consumer behaviour – a narrow group of items such as used cars and holiday accommodation accounts for most of the price increases seen in recent months – and base effects. A concern, though, is that price pressures are starting to seep into other areas, like services.

Making matters more complicated, policymakers aren't giving particularly clear signals.

The heated inflation debate taking place within the US Federal Reserve’s ranks has spilled out into the open, and investors are still waiting for an indication of when the central bank will start to wind down its USD120 billion monthly asset purchase programme or how long the process might take.

There are other risks for investors to consider.

While developed economies have started to get a grip on the pandemic, signs that outbreaks are possible despite mass vaccination programmes stand as a warning for what might happen this winter in the US and Europe. Meanwhile, regions that had previously been largely unaffected by Covid – like Southeast Asia – are bearing the brunt of the current wave.

An additional worry is China. Covid-driven lockdowns, a tightening of credit supply earlier this year and Beijing’s regulatory and market reforms have all dampened growth and raised uncertainty for the business community. A big puzzle facing the Chinese government is why households are spending so little and how to get them spending more. Taking all this into account, we have chosen to reduce exposure to some cyclical stocks (Japan) but maintain our overall neutral stance on all major asset classes.

Our business cycle analysis offers up a mixed picture. We are now less positive on the UK, Switzerland and Europe outside of the euro zone. However, we believe that weakness in the US is likely to be transitory, driven by a resurgence of the virus, which will merely postpone the pickup in consumption rather than undermine the underlying strength of the recovery.

In light of weakness in US consumption and construction we have lowered our GDP growth forecast for this year to 6.5 per cent from 7 per cent, but continue to expect a robust expansion of some 5.3 per cent for 2022.

The euro zone, meanwhile, has offered positive surprises. The leading indicator is very strong. Online indicators show that mobility is back above pre-pandemic levels, which suggests that Europeans have learned to live with Covid.

Our liquidity indicators show that Chinese credit growth peaked last autumn and then started to contract four months ago. This means that even though the People’s Bank of China’s recently cut its bank reserve requirement ratio, the lagged effects from prior tightening will linger for the rest of the year.

That said, global liquidity conditions in the coming months will be primarily determined by the pace of monetary tightening in the US. The major risk is that the US tightens too much too soon. For now, though, liquidity conditions worldwide remain supportive for riskier asset classes, with central banks still more generous than they were in the months following the global financial crisis a decade ago, while private liquidity creation in the form of loans remains at about its long run average.

Our valuation indicators show that even though global bonds have become expensive, particularly US Treasuries and euro zone bonds, equities are more expensive still.

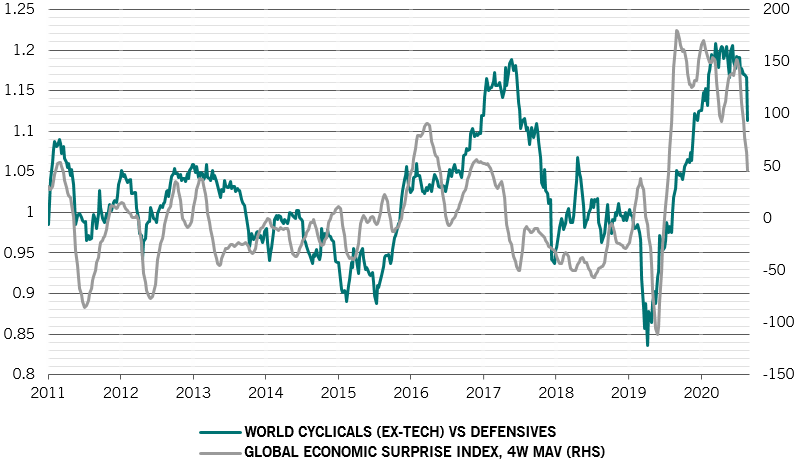

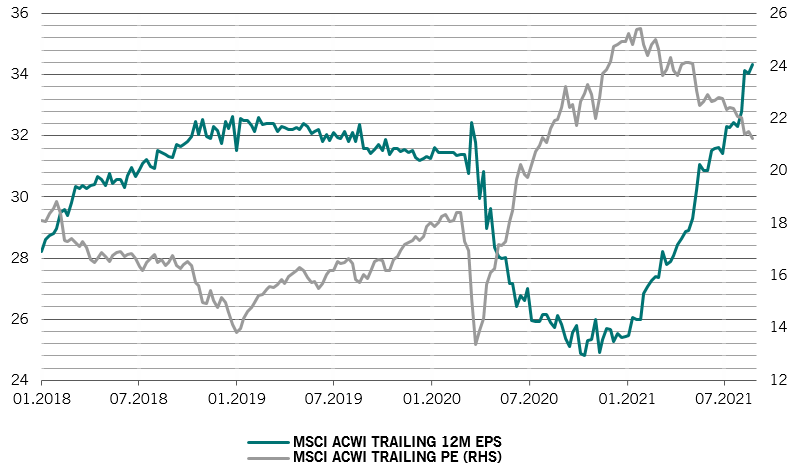

If liquidity conditions turn negative - in other words, if the rate of money supply expansion falls below the nominal rate of GDP growth - then global stocks' price to earnings ratios will come under pressure. That’s especially true because P/E ratios are very high for this stage of the cycle relative to earnings growth (see Fig. 2) – our models suggest these ratios will contract 5 to 10 per cent by the year end.

Our technical indicators show that equity sentiment remains neutral across all regions, while strong short-term trends support bonds. By contrast, a sharp loss of momentum is weighing on commodities.

Separately, investor risk appetite has pulled back from euphoric levels in mid-May across asset classes.