Select your investor profile:

This content is only for the selected type of investor.

Individual investors?

Inspiring innovation: private equity's role in developing environmental technology

Increased global commitment to climate goals presents an attractive opportunity for investors, especially in private markets.

Written by

Nicolas Thomas

Private Equity Investment Manager

The fight against climate change is gaining momentum among governments and consumers, with 92 per cent of global GDP now covered by net-zero targets. Yet these commitments cannot be met by behavioural change alone. Much will also depend on the deployment of existing technologies as well as the development of new ones. Adoption has been a problem. The penetration of cleantech is currently too low.

But there are grounds for optimism. The International Energy Agency estimates that most of the cleantech needed to achieve the world’s net-zero commitments by 2030 is already market-ready. Moreover, the environmental technologies market is forecast to more than double in size from USD4.9 trillion in 2020 to USD12.1 trillion by 2030.

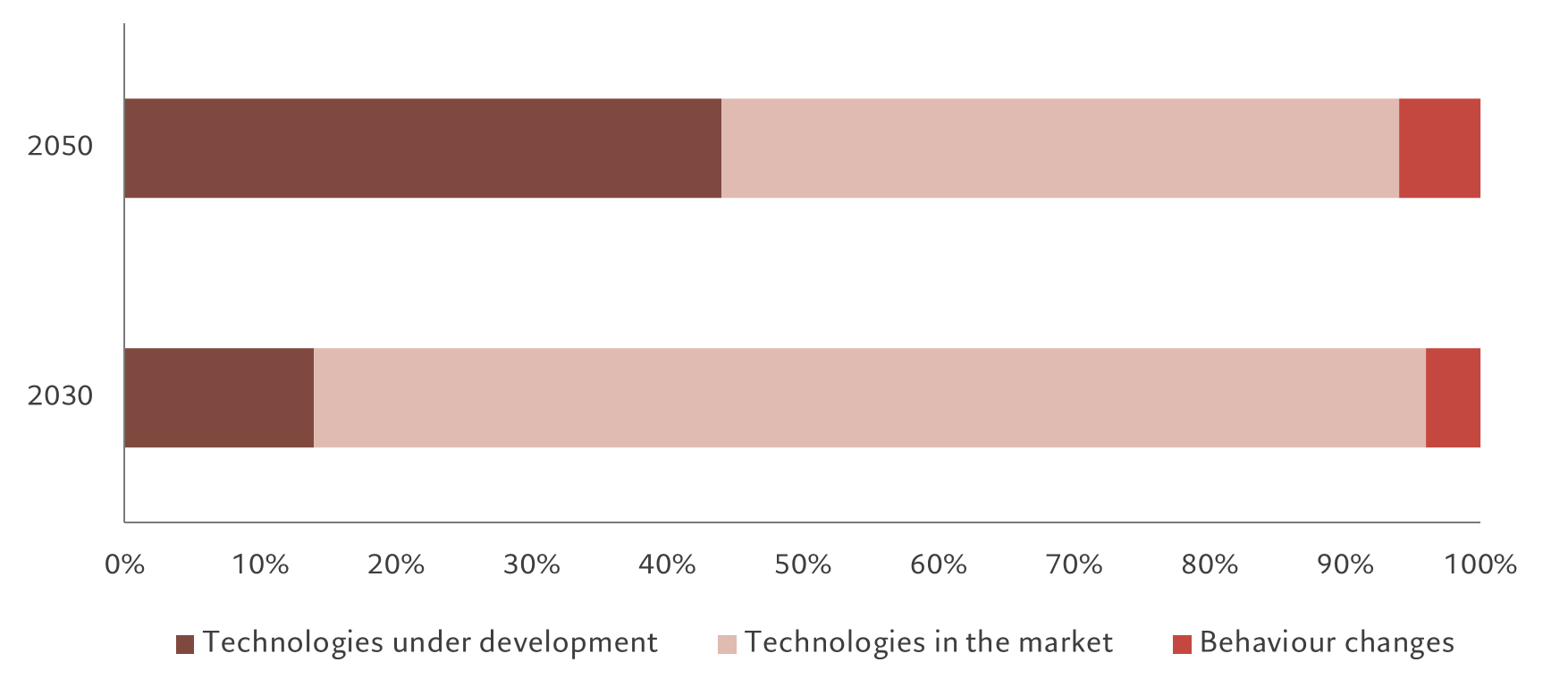

Fig. 1 - Powerful technologies

The proportion of the total emissions savings achieved through technologies (new and existing) and by behavioural change, %, relative to 2020

Source: International Energy Agency (IEA) as of 31.12.2021. For illustration purposes only.

Yet for these technologies to reach their full potential, they still need significant investment. The Climate Policy Initiative calculates that, at a minimum, climate financing must increase by 590 per cent to meet the world’s declared climate objectives by 2030.

That's a challenging target, but it presents a potentially rewarding opportunity for investors.

Investing in the transition

In our view, there are five key areas where this investment can have the greatest effect:

- Greenhouse gas reduction: batteries and storage; energy efficiency; low/no carbon and carbon removal technologies; as well as renewable energy technologies and services.

- Sustainable consumption: agri-tech; food safety; supply-chain optimisation; and food tech.

- Pollution control: water quality; air quality; soil preservation; and waste treatment.

- The circular economy: the sharing economy; recycling; resource efficiency; and bio-based materials.

- Enabling technologies: sensors and data capture; the semiconductor value chain; design and engineering software; and green chemistry.

These solutions are already attracting interest from investors, and we believe the opportunity is particularly compelling in private markets, not least because private companies are at the cutting edge of these technologies. Globally, the cumulative number of private environmental companies with a valuation above USD1 billion, firms known as unicorns, has increased 14-fold since 2017. This compares with an increase of only four times in the number of total unicorns over the same period.

Such a boom in valuations is not surprising given that private companies are taking the lead in many areas of environmental technology. For example, the efficiency record for converting the sun’s rays into electricity via a commercial-sized panel was set in May by a private European company. Private companies also include some of the largest players in the electric-vehicle value chain, as well as leaders in recycling lithium-ion batteries. Investors that have built stakes in firms operating in these sectors have enjoyed healthy returns.

The co-investment approach

Of course, investing in private companies is not without risks. That's particularly the case for the environmental tech industry, where governments and regulators play an outsized role in shaping the competitive landscape.

However, there is one area within private equity (PE) which offers investors some degree of protection from such risks: co-investments. Through this structure, PE managers (known as general partners, or GPs) offer select investors (limited partners, LPs) the opportunity to invest directly alongside them in a specific transaction.

In the past two decades, co-investment funds have raised over USD175 billion. As PE continues to expand, we expect co-investments to grow too.

For GPs, the main benefit of co-investment is the ability to invest more in firms they consider attractive (GPs are often subject to concentration restrictions, limiting how much capital they themselves can invest in a single company.)

For LPs, meanwhile, one of the key advantages of co-investing is direct access to high quality private companies. Rather than investing in hundreds of firms through a fund-of-funds vehicle, a co-investment strategy is much more focused (typically in 25-30 companies) while retaining adequate diversification across GPs, countries and industries.

Another benefit is the fact that co-investments are deployed much more rapidly (usually over two to three years) than traditional PE funds of funds, which can take six to seven years to reach full investment. Earlier deployment can help mitigate the problem embodied by the J-curve, or the tendency for PE investments to report capital losses in the early years of their life before generating gains. This is borne out by our own 30 years’ experience of co-investing at Pictet.

Ultimately, the net return is boosted by the fact that GPs typically offer co-investments free of the usual management (1.5-2.0 per cent) and performance fees (20 per cent). This is significant in an asset class that tends to command considerably higher fees than listed assets.

We believe co-investment can thus be an attractive route to invest in private markets in general, and in environmental pioneers in particular.

Grounds for optimism

By funding innovation in the private sector, investors will have a major role to play in putting the world economy on a sustainable footing.

History testifies to this.

Forty years ago, one of the planet’s foremost environmental concerns was the hole growing in the ozone layer. Activism led to the 1989 Montreal Protocol on phasing out ozone-depleting substances, such as chlorofluorocarbons (CFCs), and then the wider Kyoto Protocol in 1997. Businesses, backed by investors, developed a host of alternatives to CFCs.

Today, stratospheric ozone levels are among the few of the nine Planetary Boundaries that humanity hasn't breached.

Technological innovation, supported by private finance, can help restore the planet and deliver healthy investment returns.

read more about private equity investing

Private equity's embrace of ESG

A lack of reliable data has been a major hurdle to the adoption of ESG in private equity. But the industry is beginning to catch up.

September 2023

Why investors in Europe can no longer afford to ignore private equity

Investors in European equities are missing out if they just focus on listed stocks, particularly when it comes to the mid-cap sector.

September 2023

Healthcare's starring role in private equity

The healthcare industry's Covid-inspired technological revolution could open up new opportunities for investors in private markets.

March 2022

Important legal information

This marketing material is issued by Pictet Asset Management (Europe) S.A.. It is neither directed to, nor intended for distribution or use by, any person or entity who is a citizen or resident of, or domiciled or located in, any locality, state, country or jurisdiction where such distribution, publication, availability or use would be contrary to law or regulation. The latest version of the fund‘s prospectus, Pre-Contractual Template (PCT) when applicable, Key Information Document (KID), annual and semi-annual reports must be read before investing. They are available free of charge in English on www.assetmanagement.pictet or in paper copy at Pictet Asset Management (Europe) S.A., 6B, rue du Fort Niedergruenewald, L-2226 Luxembourg, or at the office of the fund local agent, distributor or centralizing agent if any.

The KID is also available in the local language of each country where the compartment is registered. The prospectus, the PCT when applicable, and the annual and semi-annual reports may also be available in other languages, please refer to the website for other available languages. Only the latest version of these documents may be relied upon as the basis for investment decisions.

The summary of investor rights (in English and in the different languages of our website) is available here and at www.assetmanagement.pictet under the heading "Resources", at the bottom of the page.

The list of countries where the fund is registered can be obtained at all times from Pictet Asset Management (Europe) S.A., which may decide to terminate the arrangements made for the marketing of the fund or compartments of the fund in any given country.

The information and data presented in this document are not to be considered as an offer or solicitation to buy, sell or subscribe to any securities or financial instruments or services.

Information, opinions and estimates contained in this document reflect a judgment at the original date of publication and are subject to change without notice. The management company has not taken any steps to ensure that the securities referred to in this document are suitable for any particular investor and this document is not to be relied upon in substitution for the exercise of independent judgment. Tax treatment depends on the individual circumstances of each investor and may be subject to change in the future. Before making any investment decision, investors are recommended to ascertain if this investment is suitable for them in light of their financial knowledge and experience, investment goals and financial situation, or to obtain specific advice from an industry professional.

The value and income of any of the securities or financial instruments mentioned in this document may fall as well as rise and, as a consequence, investors may receive back less than originally invested.

The investment guidelines are internal guidelines which are subject to change at any time and without any notice within the limits of the fund's prospectus. The mentioned financial instruments are provided for illustrative purposes only and shall not be considered as a direct offering, investment recommendation or investment advice. Reference to a specific security is not a recommendation to buy or sell that security. Effective allocations are subject to change and may have changed since the date of the marketing material.

Past performance is not a guarantee or a reliable indicator of future performance. Performance data does not include the commissions and fees charged at the time of subscribing for or redeeming shares.

Any index data referenced herein remains the property of the Data Vendor. Data Vendor Disclaimers are available on assetmanagement.pictet in the “Resources” section of the footer. This document is a marketing communication issued by Pictet Asset Management and is not in scope for any MiFID II/MiFIR requirements specifically related to investment research. This material does not contain sufficient information to support an investment decision and it should not be relied upon by you in evaluating the merits of investing in any products or services offered or distributed by Pictet Asset Management.

Pictet AM has not acquired any rights or license to reproduce the trademarks, logos or images set out in this document except that it holds the rights to use any entity of the Pictet group trademarks. For illustrative purposes only.