Real yields' warning to riskier fixed income

Developments in real bond yields and breakeven rates on inflation-protected bonds suggest how the rest of the fixed income market will perform. That's particularly relevant now.

Written by

Mickael Benhaim

Head of Fixed Income Investment Strategy & Solutions

Real yields always matter. But bond investors would do well to pay particular attention to what’s happening with them now. That’s because an environment of rising US real yields and falling breakeven rates on index-linked US Treasury bonds suggests fixed income and currency risk markets should brace for more pain.

Our model of US real yields versus index-linked inflation breakeven rates suggests that markets are destined for yet more US dollar appreciation, weakness in emerging market bonds and currencies, and declines in high yield bonds; investment grade and US Treasuries, by comparison, will likely remain rangebound.

Broadly speaking, the model outlines four different market regimes, depending on whether real yields and breakevens are falling or rising – more detail can be found in this article. Each of these regimes has different implications for fixed income assets and currencies (see Fig. 1).

Fig. 1 - Real yield regimes

So, for instance, during periods of falling real yields and rising breakeven rates – as occurred between September and November of last year on the back of rising inflation expectations amid pent-up demand and supply shocks – the dollar tends to weaken while risky bonds and credit tend to appreciate. Or, a period of rising real yields and rising breakeven rates – which happened in the wake of the Ukraine invasion and led the US Federal Reserve to abandon its ‘transitory inflation’ narrative and begin hiking rates – tend to lead to a rise in the dollar but falls in Treasuries and investment grade credit.

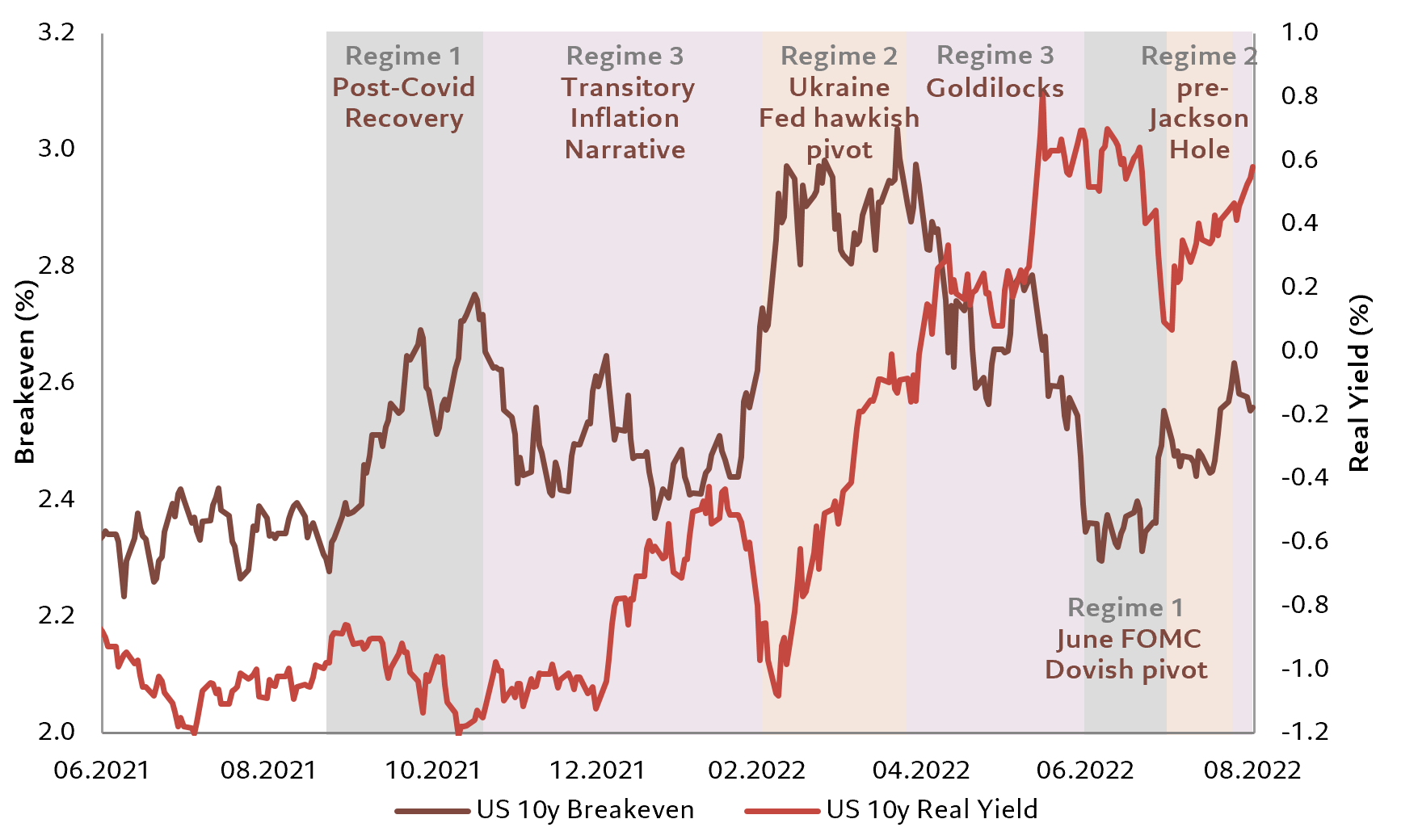

In normal times there might be slower transitions between longer-lasting regimes. But over the previous year we’ve seen dramatic changes in the macroeconomic and monetary narrative – from central bank hawkishness to dovishness and back again. Over this period, the upper bound of the US Federal Funds Target Rate has moved from 0.25 per cent to 2.5 per cent against a backdrop of consumer price inflation that peaked at 9.1 per cent, its highest since 1981. As a result, since August 2021, we have cycled through several regimes of our model {see Fig. 2].

Fig. 2 - Regime change

Real yield regimes vs US 10 year breakeven and US 10 year real yield, %

And then there was the latest shift. In August this year, Fed policymakers made it clear they were concerned that inflation wasn’t falling as fast as they’d anticipated and that they didn’t want to make the same the mistakes of the 1970s – when the Fed’s anti-inflation measures were repeatedly ended prematurely. This culminated in chairman Jerome Powell’s hawkish Jackson Hole speech. There he made it clear that the Fed’s overarching focus was to bring inflation back to its 2 per cent target. This, in turn, required a period of below trend growth and softening labour market conditions – “pain” in his words. Returning to a neutral rate of interest wasn’t sufficient. Instead, he argued, a restrictive policy stance would have to be maintained for some time.

That puts us in a regime of rising real yields and falling breakeven rates (regime 3 in Fig.1).

Investors hoping for a quick turnaround should take note. Recent history has had the Fed quickly reverse course on policy tightening in the face of weakening growth. But now, as long as inflation looks to resist returning to target in a reasonable time frame, it looks as though the Fed will turn a blind eye to rising unemployment and recession risks.

Important legal information

This marketing material is issued by Pictet Asset Management (Europe) S.A.. It is neither directed to, nor intended for distribution or use by, any person or entity who is a citizen or resident of, or domiciled or located in, any locality, state, country or jurisdiction where such distribution, publication, availability or use would be contrary to law or regulation. The latest version of the fund‘s prospectus, Pre-Contractual Template (PCT) when applicable, Key Information Document (KID), annual and semi-annual reports must be read before investing. They are available free of charge in English on www.assetmanagement.pictet or in paper copy at Pictet Asset Management (Europe) S.A., 6B, rue du Fort Niedergruenewald, L-2226 Luxembourg, or at the office of the fund local agent, distributor or centralizing agent if any.

The KID is also available in the local language of each country where the compartment is registered. The prospectus, the PCT when applicable, and the annual and semi-annual reports may also be available in other languages, please refer to the website for other available languages. Only the latest version of these documents may be relied upon as the basis for investment decisions.

The summary of investor rights (in English and in the different languages of our website) is available here and at www.assetmanagement.pictet under the heading "Resources", at the bottom of the page.

The list of countries where the fund is registered can be obtained at all times from Pictet Asset Management (Europe) S.A., which may decide to terminate the arrangements made for the marketing of the fund or compartments of the fund in any given country.

The information and data presented in this document are not to be considered as an offer or solicitation to buy, sell or subscribe to any securities or financial instruments or services.

Information, opinions and estimates contained in this document reflect a judgment at the original date of publication and are subject to change without notice. The management company has not taken any steps to ensure that the securities referred to in this document are suitable for any particular investor and this document is not to be relied upon in substitution for the exercise of independent judgment. Tax treatment depends on the individual circumstances of each investor and may be subject to change in the future. Before making any investment decision, investors are recommended to ascertain if this investment is suitable for them in light of their financial knowledge and experience, investment goals and financial situation, or to obtain specific advice from an industry professional.

The value and income of any of the securities or financial instruments mentioned in this document may fall as well as rise and, as a consequence, investors may receive back less than originally invested.

The investment guidelines are internal guidelines which are subject to change at any time and without any notice within the limits of the fund's prospectus. The mentioned financial instruments are provided for illustrative purposes only and shall not be considered as a direct offering, investment recommendation or investment advice. Reference to a specific security is not a recommendation to buy or sell that security. Effective allocations are subject to change and may have changed since the date of the marketing material.

Past performance is not a guarantee or a reliable indicator of future performance. Performance data does not include the commissions and fees charged at the time of subscribing for or redeeming shares.

Any index data referenced herein remains the property of the Data Vendor. Data Vendor Disclaimers are available on assetmanagement.pictet in the “Resources” section of the footer. This document is a marketing communication issued by Pictet Asset Management and is not in scope for any MiFID II/MiFIR requirements specifically related to investment research. This material does not contain sufficient information to support an investment decision and it should not be relied upon by you in evaluating the merits of investing in any products or services offered or distributed by Pictet Asset Management.

Pictet AM has not acquired any rights or license to reproduce the trademarks, logos or images set out in this document except that it holds the rights to use any entity of the Pictet group trademarks. For illustrative purposes only.