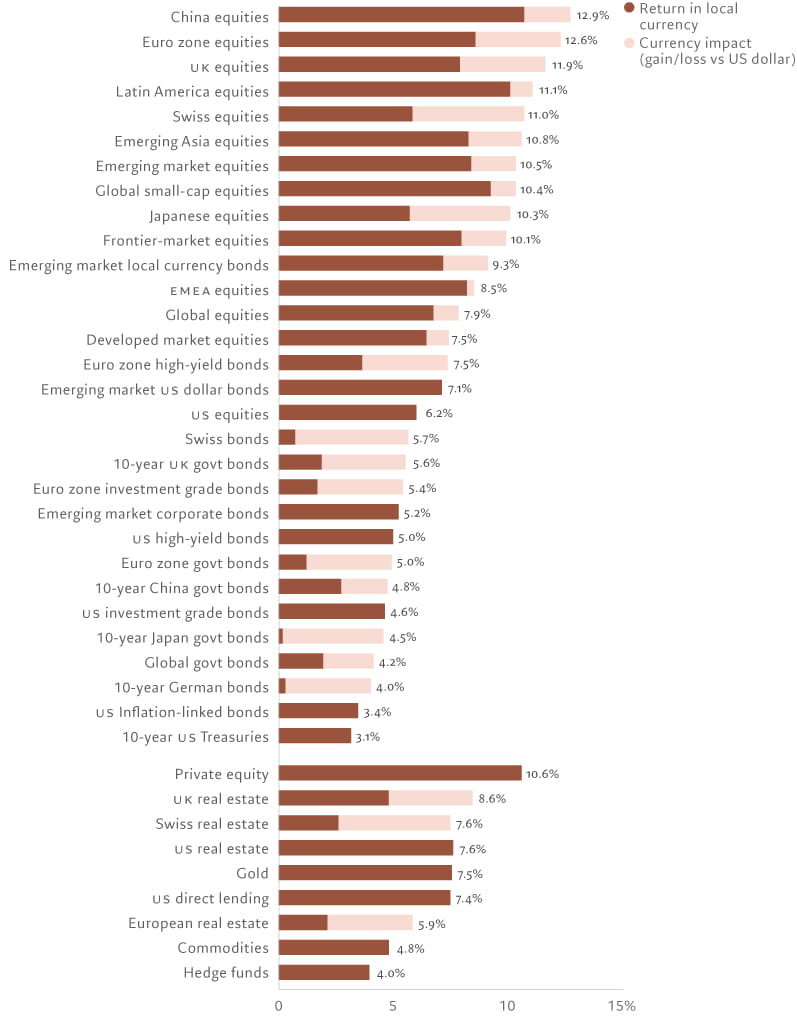

Overview: return projections in the next 5 years

Dividing a portfolio’s investments more or less evenly between developed market stocks and bonds has proved a rewarding strategy over the past few decades. The annualised return investors have secured by pursuing this approach has been in the high single digits – gains that have come courtesy of steady economic growth, an almost continuous fall in interest rates and inflation, and relatively calm financial market conditions.

Yet our forecasts covering the next five years indicate investors will need to plot a different course to achieve a similar result. This will involve allocating less capital to the developed world, increasing holdings of emerging market assets, and investing far more in alternatives, particularly commodities and gold.

A key finding from our research is that returns from equity markets will fall victim to an unfavourable shift in the business cycle. The global economy is approaching the end of its post-Covid expansionary phase. Tighter financial conditions, a peak in US jobs growth and large output gaps all point to a recession this year or next. This has significant investment implications. There is a considerable difference between making an allocation to stocks in the lead-up to a slump and doing the same once recovery begins to take root. And that’s true even for those who invest over long time horizons.

Our analysis of the past 100 years shows that an initial investment in developed market stocks after the end of a recession delivers a price return of 10 per cent a year for the following five years; investing before a recession, as would be the case today, has by comparison typically delivered only a 4 per cent annualised return – a shortfall of some 6 per cent per year.

Another obstacle for developed equity markets is a looming squeeze on corporate profit margins. With wages and raw materials prices rising, more stringent regulations adding to the costs of doing business and the prospect of a rise in corporate taxation, margins can be expected to fall by a cumulative 10 per cent over the next five years.

But it is not only developed market stocks that will struggle to match their past performance. Developed government bonds will also labour to deliver what investors require of them over the next five years. Such securities have traditionally served as an anchor for a diversified portfolio – a crucial source of income and capital protection during periods of economic uncertainty.

Yet outside the US – where initial valuations for government and investment grade bonds are becoming more attractive thanks to this year’s spike in yields – returns from developed market fixed income will fall below inflation over the next five years.

Source: Pictet Asset Management

To make up for the lacklustre returns and income on offer from the developed world, investors will have to strike a delicate balance. On the one hand, our analysis indicates that, on average, portfolios will require higher allocations to stocks and bonds from emerging markets, as well as commodities – riskier investments that offer higher prospective returns. On the other, it would be prudent to accompany this dialling up of risk with a higher allocation to assets that do not move in lockstep with mainstream stocks and bond markets, such as liquid alternatives, gold and private assets.

Within emerging markets, Chinese stocks look particularly attractive while emerging market bonds’ income-generating potential should grow, enhanced by what we believe will be a steady appreciation in developing world currencies.

Among alternatives, non-energy commodities look especially appealing; their returns should be in excess of inflation over the next half a decade.

Our analysis also shows real estate and private equity both outperforming developed market equities over our five-year forecast horizon. Allocations to gold and infrastructure, meanwhile, make sense at this juncture as a means to diversify risk and protect portfolios against the possibility of stubbornly high – or volatile – inflation.

Investors can remain faithful to the traditional balanced portfolio of mainstream bonds and stocks but, in doing so, accept a lower return and potentially higher volatility.