Diversifying investments across mainstream asset classes is generally viewed as an effective way to navigate the peaks and troughs of the financial markets. Yet while harvesting the risk premia of bonds and stocks can deliver rewards over time, this approach is not entirely failsafe. Its heavy reliance on two sources of return can become a liability, particularly when fixed income and equity markets decline in lockstep.

One way to mitigate the risks associated with a portfolio dominated by stocks and bonds is to allocate some of that capital to alternative investments. Provided such investments deliver returns that are genuinely uncorrelated with those of mainstream asset classes, their addition to a portfolio can help diversify sources of risk and return over the long run.

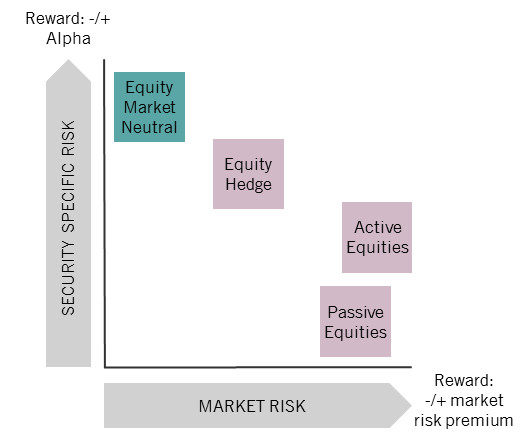

Market neutral strategies are alternative investments that exhibit such characteristics. Unlike other alternative investments, market neutral strategies aim to maintain low market risk, or limited sensitivity to shifts in the broader market, and high security-specific risk, or heightened exposure to the stock or bond selection skills of investment managers (Fig. 1).

FIG. 1 - MARKET NEUTRAL FOCUSES ON SECURITY-SPECIFIC RISK

Source: Pictet Asset Management

Their return objectives are consequently not tied to a reference benchmark; instead, they are usually expressed as a spread above a specific interest rate (eg Libor).

Managed well, such strategies can:

help investors secure returns that are not dependent on the trajectory of bond and stock markets

mitigate capital losses in a diversified portfolio during periods of market stress

improve the risk-adjusted return of a traditional balanced portfolio consisting of stocks and bonds

While the concept is not new, market neutral strategies can be expected to serve the needs of a broader group of investors in the future. This is largely because the deployment of ultra-loose monetary policy has caused profound changes across the investment landscape, transforming the risk-return profile of mainstream asset classes. Among the challenges investors face are:

Fixed income risk premia a potentially more volatile source of return.

Yields on developed market government bonds and investment grade credit sit well below the historical norm. But with inflation and interest rates unlikely to fall much further, returns from fixed income look set to be lower and more volatile than has been the case over the past 30 years.

High equity valuations may limit future returns.

Over the next five years, we expect inflation-adjusted returns for developed market stocks to be below average. Valuations – as measured by price-earnings ratios – are already high by historical standards in many developed stock markets, potentially limiting the scope for further gains. Moreover, corporate earnings growth can also be expected to be muted as real economic growth remains below par.

02

The mechanics of market neutral investing

Breaking down the return

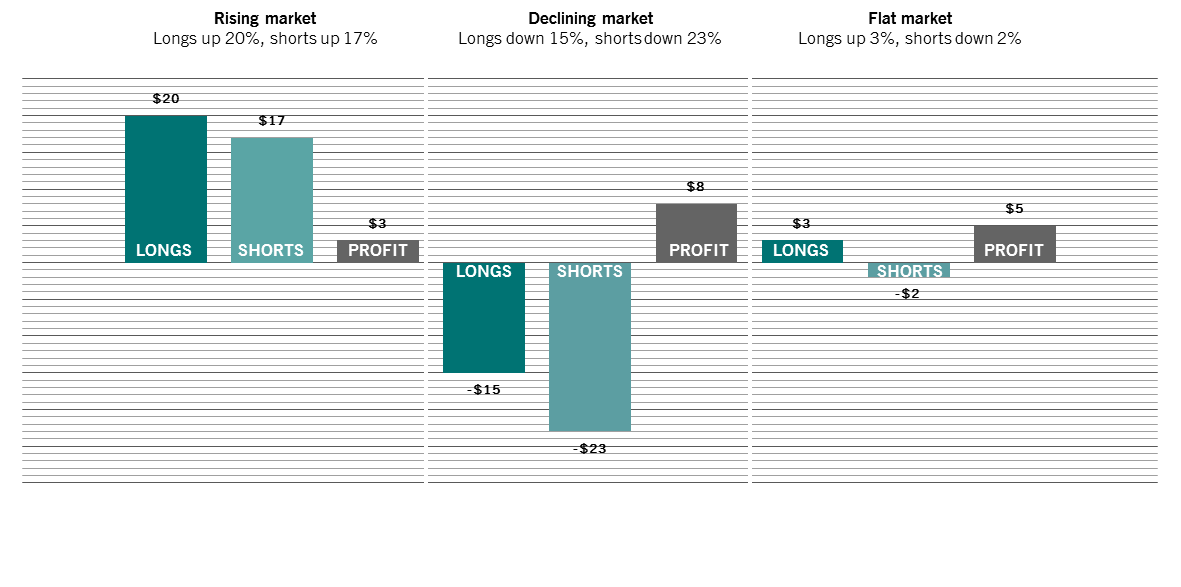

The return generated by a traditional long-only actively-managed portfolio has two components to it: beta, or the investment gain attributable to market returns, and alpha, the excess return that stems from the skill of the investment manager. Under a market neutral approach beta, or market risk, is minimised and alpha, or security-specific risk, is maximised by giving managers the discretion to build both long and short positions.

FIG. 2 - THE MECHANICS OF LONG/SHORT INVESTING

A hypothetical USD100 investment

Source: Pictet Asset Management

By enabling investment managers to express both positive and negative views, security selection skills are exploited to the full. There is a clear logic to this: high-quality investment research not only unearths the securities that will outperform, it identifies the future laggards too. In principle, the aggregate beta of the short positions in a market neutral portfolio should be roughly equal the aggregate beta of the long investments.

So, provided the investment manager has selected the right securities, the gains from the long positions should outweigh losses from the short investments in a rising market; if the market falls, the gains from short positions will be greater than the losses in the long investments (Fig.2).

The return of a market neutral strategy, then, is the difference in return between the long and short book – or spread.

03

Historic risk and return patterns for market neutral funds

Market neutral strategies exhibit distinct patterns of return

In seeking to generate investment gains almost exclusively from the performance of individual securities, market neutral strategies have acquired some distinctive characteristics.

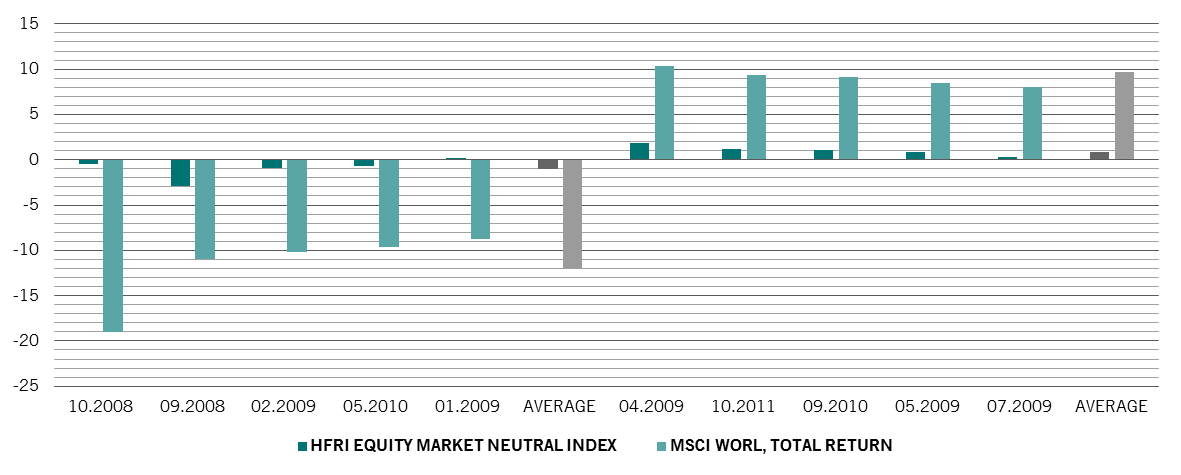

Market neutral strategies' returns are rarely in sync with those of mainstream asset classes (Fig. 3).

FIG. 3 - MARKET NEUTRAL VS. GLOBAL EQUITIES

Returns, %, in 5 best and worst months for stocks since 2005

Source: Bloomberg, Pictet Asset Management. Returns in US dollars, covering period 30.04.2005-30.04.2015

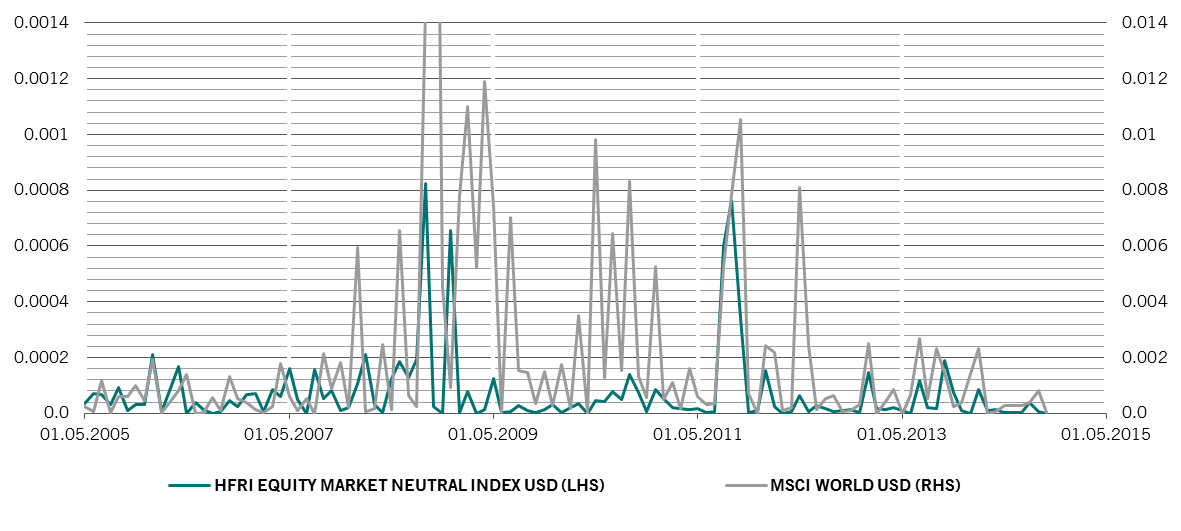

This is also laid bare in a comparison of the instantaneous variance of returns generated by market neutral strategies and global stocks. In this analysis, instantaneous variance is calculated by squaring monthly returns.

As Fig. 4 shows, market neutral and world equities experience spikes and troughs in variance at different times. This suggests that the factors responsible for the volatility of market neutral funds are different from those that influence equity markets.

FIG. 4 - RETURN VARIANCE: MARKET NEUTRAL VS WORLD STOCKS

Monthly returns, %, squared

Source: Bloomberg. Pictet Asset Management. Returns in USD; data covering period 30.04.2005-30.04-2015.

This distinct return pattern helps explain why market neutral strategies can diversify sources of risk and return in a broad portfolio. It is also a source of stability. History shows that market neutral portfolios can offer investors a considerable degree of capital protection during bear markets relative to mainstream asset classes.

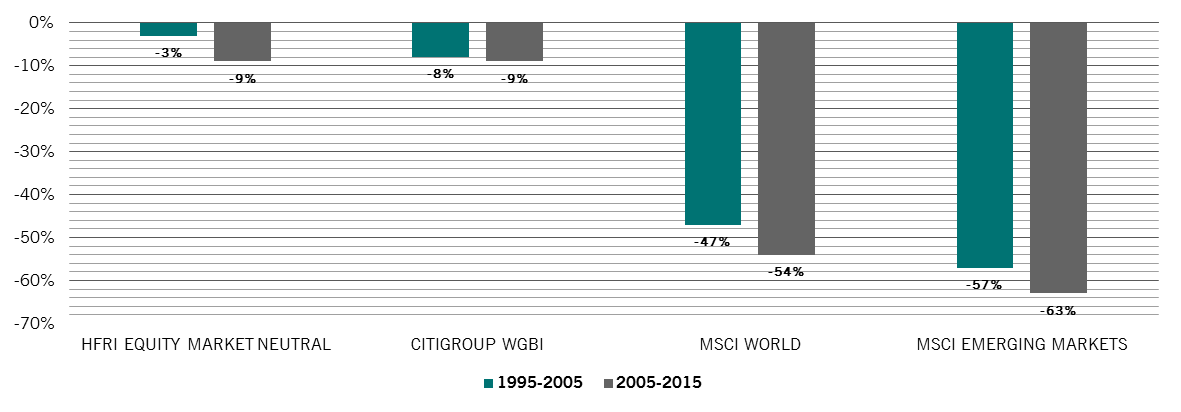

Over the past 20 years, the peak-to-trough loss, or drawdown, among market neutral strategies has been far shallower than that of equities and compares favourably to that of fixed income (Fig. 5).

FIG. 5 - DRAWDOWNS: MARKET NEUTRAL VERSUS BONDS AND STOCKS

Source: Bloomberg, Pictet Asset Management. Data covering period 30.04.1995-30.04.2015; returns in USD

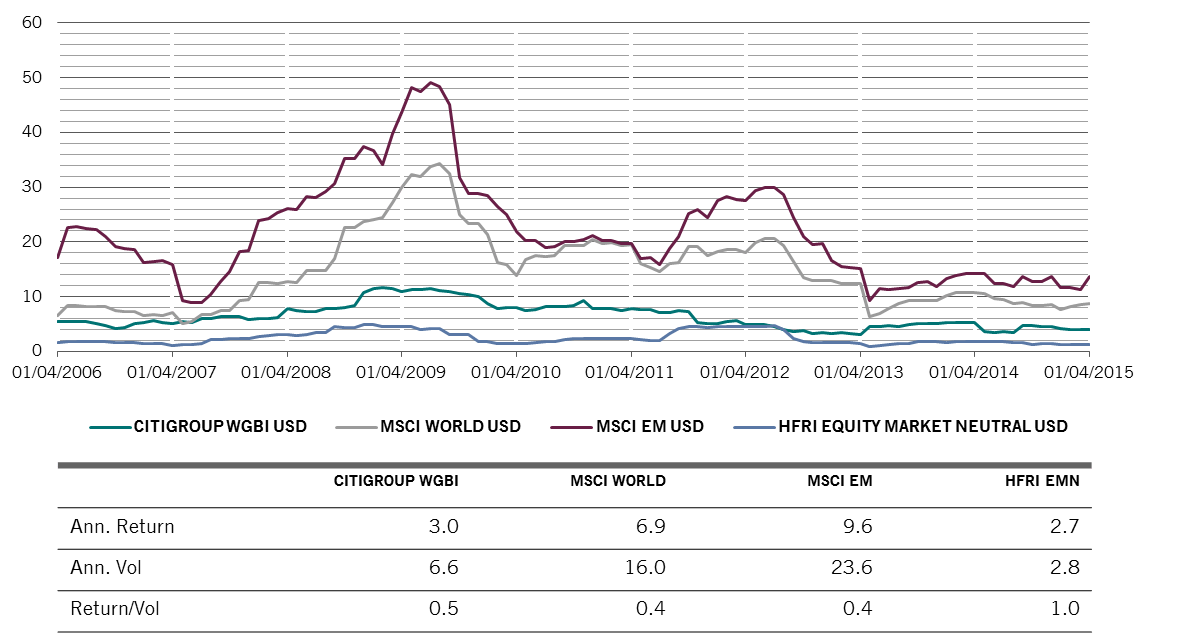

Market neutral funds have also experienced lower volatility than either bonds or stocks while their risk-adjusted returns have also been higher than mainstream assets over the long run (Fig. 6).

FIG. 6 - VOLATILITY AND RETURNS: MARKET NEUTRAL VS BONDS AND STOCKS

Data covering period 30.04.2005-30.04.2015; volatility calculated on a 12-month rolling basis, returns in USD

Source: Bloomberg, Pictet Asset Management

04

Market neutral investing – degrees of neutrality

Not every strategy that exhibits low beta can claim to be impervious to the fluctuations in the broader financial market. That is because beta and correlation are not perfect measures of market risk.

There are, in fact, a number of systematic-like risks that have a bearing on the returns of stocks but are not adequately captured by conventional indicators of neutrality such as beta.

Examples include country, sector, currency and style exposures.

Strategies run by investment managers that either ignore – or systematically harness – these risk factors may struggle to maintain their neutrality across all phases of the market cycle. For example, returns will suffer if a certain style falls out of favour.

Another risk that can taint a strategy’s neutrality is liquidity. Securities are not universally liquid, and history shows that illiquid stocks tend to outperform their more liquid counterparts over time. Skewing a portfolio’s long positions towards illiquid stocks might therefore have some appeal. But the strategy can land investors in trouble, particularly during episodes of market stress, as illiquid securities tend to suffer most in such instances.

The introduction – or mismanagement – of systematic biases is perhaps one reason why the risk-return profile of market neutral strategies differs considerably from fund to fund.

For prospective investors, the lessons are clear: Some market neutral strategies are more neutral than others.

05

Key takeaways

Market neutral strategies can:

Help investors secure returns that are not dependent on the trajectory of bond and stock markets

Their returns are dependent on the skills of investment professionals, not on moves in the broader financial market.

Mitigate capital losses in a diversified portfolio during periods of market stress

By enabling investment managers to express both positive and negative views, security selection skills are exploited to the full.

Improve the risk-adjusted return of a traditional balanced portfolio consisting of stocks and bonds

Provided such investments deliver returns that are genuinely uncorrelated with those of mainstream asset classes, their addition to a portfolio can help diversify sources of risk and return over the long run.

This marketing material is issued by Pictet Asset Management (Europe) S.A.. It is neither directed to, nor intended for distribution or use by, any person or entity who is a citizen or resident of, or domiciled or located in, any locality, state, country or jurisdiction where such distribution, publication, availability or use would be contrary to law or regulation. The latest version of the fund‘s prospectus, Pre-Contractual Template (PCT) when applicable, Key Information Document (KID), annual and semi-annual reports must be read before investing. They are available free of charge in English on www.assetmanagement.pictet or in paper copy at Pictet Asset Management (Europe) S.A., 6B, rue du Fort Niedergruenewald, L-2226 Luxembourg, or at the office of the fund local agent, distributor or centralizing agent if any.

The KID is also available in the local language of each country where the compartment is registered. The prospectus, the PCT when applicable, and the annual and semi-annual reports may also be available in other languages, please refer to the website for other available languages. Only the latest version of these documents may be relied upon as the basis for investment decisions.

The summary of investor rights (in English and in the different languages of our website) is available here and at www.assetmanagement.pictet under the heading "Resources", at the bottom of the page.

The list of countries where the fund is registered can be obtained at all times from Pictet Asset Management (Europe) S.A., which may decide to terminate the arrangements made for the marketing of the fund or compartments of the fund in any given country.

The information and data presented in this document are not to be considered as an offer or solicitation to buy, sell or subscribe to any securities or financial instruments or services.

Information, opinions and estimates contained in this document reflect a judgment at the original date of publication and are subject to change without notice. The management company has not taken any steps to ensure that the securities referred to in this document are suitable for any particular investor and this document is not to be relied upon in substitution for the exercise of independent judgment. Tax treatment depends on the individual circumstances of each investor and may be subject to change in the future. Before making any investment decision, investors are recommended to ascertain if this investment is suitable for them in light of their financial knowledge and experience, investment goals and financial situation, or to obtain specific advice from an industry professional.

The value and income of any of the securities or financial instruments mentioned in this document may fall as well as rise and, as a consequence, investors may receive back less than originally invested.

The investment guidelines are internal guidelines which are subject to change at any time and without any notice within the limits of the fund's prospectus.

The mentioned financial instruments are provided for illustrative purposes only and shall not be considered as a direct offering, investment recommendation or investment advice. Reference to a specific security is not a recommendation to buy or sell that security. Effective allocations are subject to change and may have changed since the date of the marketing material.

Past performance is not a guarantee or a reliable indicator of future performance. Performance data does not include the commissions and fees charged at the time of subscribing for or redeeming shares.

Any index data referenced herein remains the property of the Data Vendor. Data Vendor Disclaimers are available on assetmanagement.pictet in the “Resources” section of the footer.

This document is a marketing communication issued by Pictet Asset Management and is not in scope for any MiFID II/MiFIR requirements specifically related to investment research. This material does not contain sufficient information to support an investment decision and it should not be relied upon by you in evaluating the merits of investing in any products or services offered or distributed by Pictet Asset Management.

Pictet AM has not acquired any rights or license to reproduce the trademarks, logos or images set out in this document except that it holds the rights to use any entity of the Pictet group trademarks. For illustrative purposes only.

Cookie Policy

This website uses cookies to enhance user navigation and to collect statistical data. To refuse the use of cookies, change your settings or for more information, please click on the following link: Cookies policy. By continuing to browse this website, you accept the use of cookies for the above purposes.