Global market overview - Beware the flames of inflation

Winter is coming. But as temperatures fall across the Northern hemisphere, in the financial arena one element is heating up – inflation.

From the US in the West to China and Japan in the East, we see price pressures accelerating next year in virtually every major economy, with global inflation hitting a four-year high. In the US, Donald Trump’s victory in the presidential elections is likely to further stoke the fire as promises of extensive infrastructure spending and tax cuts pump billions of dollars into the economy and boost commodity prices.

In the UK, meanwhile, prices will be pushed up by the 12 per cent slump in sterling’s trade-weighted exchange rate since the June referendum vote to leave the European Union.

The change in the investment climate will also be characterised by heightened geopolitical risks and a looming reversal of one of the most potent investor-friendly trends of recent years – ample liquidity.

Politically, the spotlight is now on continental Europe. Following the surprises of the Brexit vote and Trump’s win, investors will be looking for any signs of similar anti-establishment feeling in Italy’s constitutional referendum this December, as well as in the German general election and French presidential polls in 2017.

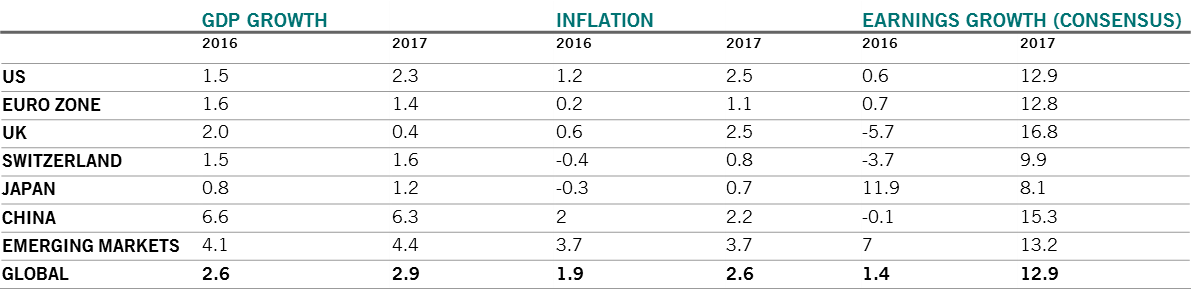

Economic and earnings forecasts for 2017, in %

Source: Pictet Asset Management, CEIC, Thomson Reuters Datastream, as at 16.11.2016

The liquidity path is, arguably, easier to predict. We now forecast three US Federal Reserve interest rate hikes by end-2017, starting this December. This is an increase from the previously expected two hikes as we think that Trump’s fiscal loosening will be counteracted by tighter monetary policy.

In the euro zone, the European Central Bank's quantitative easing programme will almost certainly be extended beyond March, but we expect that liquidity injections will be reduced by the end of next year to EUR60 billion per month as inflation and growth pick up.

In total, we believe that between them the Fed, the ECB and their counterparts in the UK, China and Japan will generate USD900 billion of net liquidity in 2017 – an almost 50 per cent decline on this year’s USD1.7trillion and compared to an average of USD1.2 trillion per annum over the past seven years.1

More positively, global corporate earnings should benefit from an acceleration in nominal gross domestic product (GDP) growth and could rise by as much as 13 per cent globally compared with a paltry 1 per cent this year. Bigger profits, in turn, could encourage companies to step up capital expenditure, enabling business investment to surpass consumer spending as the main source of economic growth.

The broader economic recovery – while still relatively muted – is becoming increasingly widespread. Leading indicators and global business confidence are rising in all major economies and we see scope for positive surprises in the US, euro zone and Japan on the back of more expansionary fiscal policy.

1 Central bank liquidity is the sum of asset purchases and credit operations net of sterilisation operations. Source: Thomson Reuters Datastream, Pictet Asset Management

02

Asset allocation - Liquidity drain a risk for all asset classes

Investors will need to buckle up in 2017. Political turmoil, rising inflation and tighter financing conditions look set to rub up against improving economic growth and rising corporate earnings. That adds up to a challenging environment for equities but potentially a pretty grim one for bonds and bond-like dividend-paying stocks.

For the US dollar, the path is more nuanced. Upward forces from Fed’s rate hikes and Trump’s economic stimulus are likely to triumph in the short-term, but over a longer time horizon they will be counteracted by the currency’s increasingly stretched valuation and – potentially – by reduced foreign investor appetite for US assets.

The winners in the current climate should include cyclical shares as well as traditional hedges against volatility and inflation, such as gold, the VIX and inflation-linked bonds. We also think it is prudent to go into next year with ample holdings of cash – both as insurance against market falls and, arguably more importantly, to be ready to take advantage of any dislocations and mispricing that could follow from political upsets or policy actions.

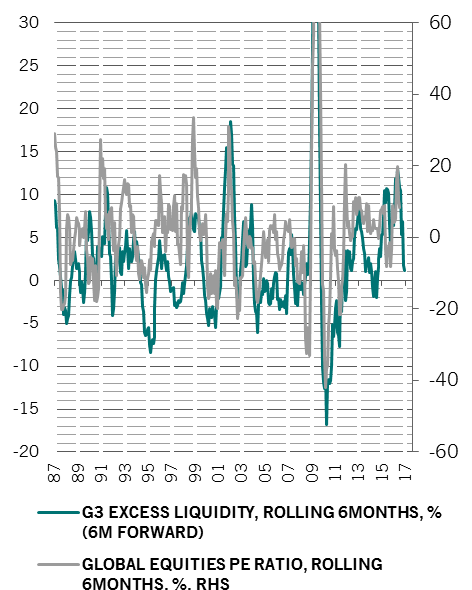

US dollar liquidity – as measured by the US monetary base and foreign official assets denominated in US dollars held at the Fed – is already falling at a rate of 5 per cent year-on-year. The drain is likely to accelerate in 2017 thanks to more hikes from the Fed, continued falls in emerging market foreign currency reserves and reduced bond purchases by both the ECB and the Bank of Japan.Historical correlation analysis suggests that lower liquidity will – with a six month lag – result in reduced earnings multiples (see chart).

Falling liquidity to push down PE ratios

Source: Thomson Reuters Datastream, Pictet Asset Management, as at 31.10.2016

That’s not to say the picture is universally negative for equities. One support for riskier asset classes will be better economic growth. Our business cycle indicators point to an accelerating – albeit still modest – economic expansion. The global manufacturing PMI has risen to a two-year high, to levels consistent with 3.5 per cent annualised growth in industrial production. Activity picked up in 22 out of the 31 countries included in the index, suggesting that the recovery is widespread.

Within the developed world, we have upgraded our growth forecast for the US economy. Trump’s plans to slash corporate tax rates to 15 per cent from 35 per cent, spend at least an additional USD500 billion on infrastructure and encourage multinationals to repatriate foreign earnings could add as much as 1 percentage point to GDP growth in the next two years (although the final policy mix is likely to be watered down significantly from the campaign promises). Fiscal easing will result in a longer economic cycle than we assumed a few months ago. The risk of a recession in the next 12-18 months now looks more remote, as long as private investment spending rises at a faster rate than GDP.

Growth-boosting fiscal policy is also on the cards in Europe and Japan. In the former, it will combine with pent-up demand, improving lending conditions and a competitive exchange rate.

In Japan, meanwhile, fiscal stimulus sits alongside rising exports, which have already helped annualised growth to smash expectations in the third quarter of 2016 with a 2.2 per cent reading versus consensus forecast of 0.8per cent.

China is one of the few countries where we see growth easing next year, but only modestly. Protectionist policies from the US are a risk, but our base case scenario is that these are not imminent.

In terms of valuations, global equities look fairly valued at a 15.3 times the 12 month forward earnings. Bonds are still expensive but their recent sharp sell-off has cut the overvaluation by a third.

The equity risk premium (excess return over government bonds) is significantly above its 10-year average with the notable exception of the US. We would argue that this spread should remain wide, in line with elevated policy uncertainty

Note: G3 broad money minus value of domestic industrial production growth over the past 6 months (GDP-weighted). Forecast assumes that G3 industrial production will continue to rise at the same pace of the last 3 months, PPI will rise in line with the oil price (with a lag) and money supply growth will be at the bottom quintile since 2009 .

03

Equity region and sector allocation - Japan leads on valuation and prospects

Bad news for equities includes tightening liquidity conditions, political upheaval and the return of wage inflation. The risk of protectionism is extremely difficult to price but even a low-intensity trade war stoked by the new US administration can do long-term damage to equities, especially for emerging markets and for large-cap companies with substantial global supply chains.

History also suggests a cautious positioning – the first year of a US presidential term has traditionally been the worst for equity markets. Election years, in contrast, have been some of the best.

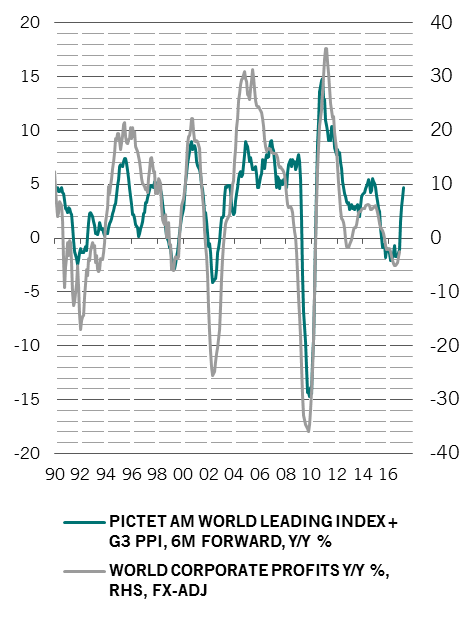

Good news comes in the form of an expected acceleration in corporate earnings growth. Globally, we see companies posting double-digit profit growth in 2017 after a virtually flat showing in many key markets this year. A move by the US administration to cut regulation and corporate taxes could offer further support. If all the tax cuts proposed by Trump are implemented – which is not a given – they could boost US equity values by 7-10 per cent.

Corporate profits to accelerate as nominal growth improves

Source: Thomson Reuters Datastream, Pictet Asset Management, as at 31.10.2016

However, US stocks are close to being the most expensive ever versus Japanese and European peers so a marked further outperformance is unlikely unless markets enter a risk-off phase or the dollar depreciates markedly.Europe, for example, is trading at a 24per cent discount to the US based on the 12-month price-to-earnings (PE) ratios, compared with a 10-year aver-age of 17 per cent.

That in itself, however, is not necessarily a reason to buy. While European equities could present an attractive investment opportunity in the medium term, for now there are good reasons for the hefty risk premium. The banking sector, where the potential for large scale recapitalisations is high, is one area of concern. An even bigger issue is regulation. In Europe more than elsewhere, domestic institutions, such as insurers, are restricted in their ability to sell bonds and buy equities. That means the impetus for a market rebound will need to come from foreign investors. This is unlikely to happen while there are still uncertainties over both ECB policy and the outcome of various European elections. By the second half of 2017, these risks may well have cleared, paving the way for a reversal in the extremely negative sentiment and thus for a market rally.

Japan, on the other hand, is worth buying now – not just because it is the cheapest developed stock market in our model but also because of its positive economic prospects. Although trade curbs are a risk in Japan, its exporters should win out as global growth improves. This will enable the Tokyo bourse to shrug off any negative implications of tighter global monetary policy and rising bond yields. Japan is also historically a market that benefits the most in a global reflation scenario.

Within Japan, some of the best opportunities can be found in financials. The gradual steeping of the Japanese bond yield curve may well boost banks’ lending spreads (the difference between the rate they charge on loans and the one they offer on deposits), while the improving economic outlook bodes well for credit demand.

We are bullish on the long-term outlook for emerging markets due to their attractive valuations, structural reforms, a recovery in commodity prices and healthy investment flows. However, the recent sell-off highlights the vulnerability of this asset class to trade concerns, a surging dollar and tighter financial conditions.

We are bullish on the long-term outlook for emerging markets.

On balance we think that EM stocks should outperform next year on improving fundamentals and we would look to selectively add to our exposure there. Regionally, emerging Europe and Asia look the cheapest with Asia trading at a 10 per cent discount to Latin America – close to a record low and compared with a more typical 10 per cent premium.

When it comes to equity sectors, cyclical stocks are in general well-positioned for the coming year, despite their recent rally. If nominal GDP growth and corporate earnings accelerate as we expect, cyclical stocks should rally to trade in line with their long-term 10 per cent premium to defensive stocks.2 This compares to the current 4 per cent premium and 10 per cent discount in early July.

Capex related stocks should perform particularly well as corporations step up investment. Financials shares, meanwhile, are set to benefit the most from global reflation due to their cheap valuations and their tendency to respond positively to a steeper yield curve.

2 Based on cyclically adjusted PE ratios.

04

Fixed income and currencies - Valuations and tighter conditions cast shadow over US High Yield

For the bond market, the entwined threats of rising inflation and tightening monetary policy are more unequivocally negative than for other asset classes.

In the developed world, those forces are strongest in the US, where inflation is on track to top 2 per cent for the first time since 2014. Trump’s policies are likely to add to inflationary pressures through tax cuts and public spending increases.

Based on the projections of the non-partisan Committee for a Responsible Federal Budget, we estimate that the budget deficit will nearly double to average 6.1 per cent of GDP over the next decade if Trump’s policies are implemented. That is likely to prompt greater monetary policy tightening than previously expected from the Fed, in turn leading to higher US government bond yields and a steeper yield curve.

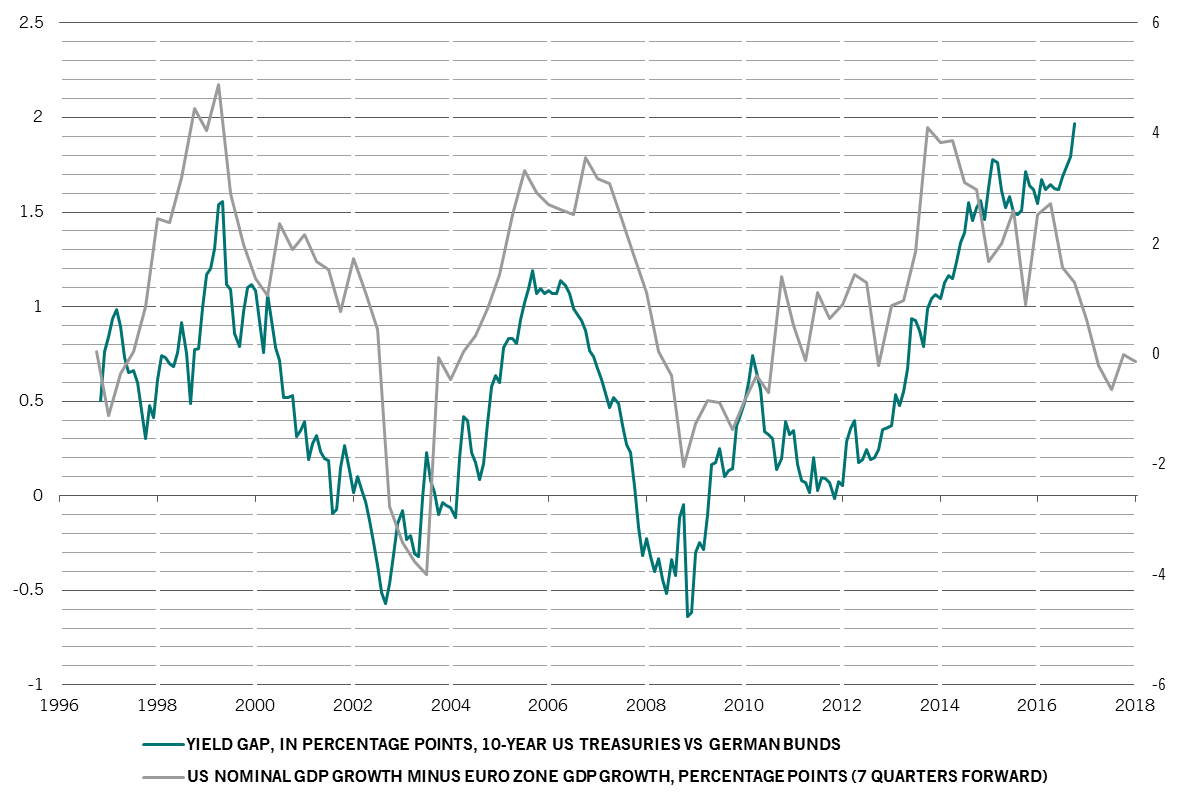

Historically, the transition from monetary easing/fiscal tightening to the opposite has been negative for bonds and the starting point today is unfavourable due to the asset class's high valuations. We see bond yields moving higher in 2017, especially in Europe where the risk of tighter central bank policy is underappreciated. European bonds also look very expensive compared to their US counterparts: the Treasuries-Bunds yield spread is at 194bps, the highest since 1990.

Having benefited from the 2016 rally in US high yield bonds, we have now turned neutral on this asset class. On our valuation models – where the cheapest level in history scores 100 and the most expensive scores zero – US high yield has retreated from 75 in February to 11 now. Debt ratios for non-financial companies are at historic peaks and the corporate default rate has risen to a six-year high of 4.8 per cent. These metrics suggest that we are past the peak in the credit cycle.

US bonds look attractive as Bund-Treasury yield gap underestimates Europe’s economic growth

Source: Dealogic, Pictet Asset Management, as at 31.10.2016

One notable bright spot in fixed income, particularly when it comes to valuations, is EM local currency debt. As well as offering some of the highest yields in mainstream fixed income, EMcorporate bonds tend to have shorter durations, making them less vulnerable to interest rate hikes. The opportunity is far from risk free, however – possible threats to performance include a stronger US dollar and Trump’s protectionist stance on global trade.

Among emerging markets, we prefer Latin America due to encouraging signs of progress on structural reform as well as the region's exposure to commodities and energy, whose prices should rise.

With global producer price inflation surging to five-year highs, inflation-linked bonds are starting to look attractive again but we continue to think that gold is a better hedge in the long-term. After the recent price fall, it is also more attractive from a tactical perspective.

In the currency markets, the dollar is indeed likely to strengthen in the coming months due to stronger US growth and the Fed signalling more hikes than are currently priced in. But over the course of 2017 as a whole we expect a very volatile, range-bound performance, with the dollar currently circa 20 per cent overvalued on our models.

Sterling, meanwhile, looks cheap following the steep depreciation since the Brexit vote. The exchange rate is now consistent with fairly dire economic growth. While weak growth may materialise eventually as Britain progresses with the EU exit, we believe that in the short term the UK economy and assets are more likely to exceed expectations, which in turn presents potentially attractive investment opportunities

05

Key takeaways

Annual outlook 2017

Global asset classes

Rising inflation and tightening monetary policy will prove tough for bonds in 2017, while cyclically-sensitive equity sectors should benefit from improving economic growth.

Equity regions and styles

Japanese equities rate strongly both on valuations and fundamentals. Selected emerging markets could also do well.

Fixed income

Inflation-linked bonds are starting to look attractive again, while high yield bonds (particularly in the US) merit a more cautious approach.

About

Pictet Asset Management Strategy Unit

The Pictet Asset Management Strategy Unit (PSU) is the investment group responsible for providing asset allocation guidance across stocks, bonds, commodities and alternatives.

About

Luca Paolini

Luca Paolini joined Pictet Asset Management in

2012 as Chief Strategist. Before joining Pictet, Luca worked as an Equity

Strategist at Credit Suisse Securities, responsible

for asset, regional and sector allocation. From

2005 to 2007, he was Investment Strategist at

Union Investment. Luca started his career in 2001

at Allianz Dresdner Asset Management as a

assistant vice president, covering asset allocation

and investment strategy.

Luca holds a Master degree in International

Economics and Management from SDA Bocconi

School of Management in Milan, and a Laurea

Magistrale in Political Sciences from the University

of Bologna.

About

Olivier Ginguené

Olivier Ginguené is Chief Investment Officer for Asset Allocation and Quantitative Investments, Chairman of the Pictet Asset Management Strategy Unit and a member of the Executive Committee of Pictet Asset Management. He joined Pictet Asset Management in 2003.

Before joining Pictet, he headed the global equity team at Crédit Agricole Asset Management. Olivier began his investment career in 1993 at Crédit Lyonnais Asset Management in Paris where he was in charge of quantitative investments.

Olivier holds Master's degrees from the Ecole Polytechnique (Paris) and the Ecole Nationale Supérieure d'Administration Economique (Paris). He is a Chartered Financial Analyst (CFA) charterholder.

Share this article

Important legal information

This marketing material is issued by Pictet Asset Management (Europe) S.A.. It is neither directed to, nor intended for distribution or use by, any person or entity who is a citizen or resident of, or domiciled or located in, any locality, state, country or jurisdiction where such distribution, publication, availability or use would be contrary to law or regulation. The latest version of the fund‘s prospectus, Pre-Contractual Template (PCT) when applicable, Key Information Document (KID), annual and semi-annual reports must be read before investing. They are available free of charge in English on www.assetmanagement.pictet or in paper copy at Pictet Asset Management (Europe) S.A., 6B, rue du Fort Niedergruenewald, L-2226 Luxembourg, or at the office of the fund local agent, distributor or centralizing agent if any.

The KID is also available in the local language of each country where the compartment is registered. The prospectus, the PCT when applicable, and the annual and semi-annual reports may also be available in other languages, please refer to the website for other available languages. Only the latest version of these documents may be relied upon as the basis for investment decisions.

The summary of investor rights (in English and in the different languages of our website) is available here and at www.assetmanagement.pictet under the heading "Resources", at the bottom of the page.

The list of countries where the fund is registered can be obtained at all times from Pictet Asset Management (Europe) S.A., which may decide to terminate the arrangements made for the marketing of the fund or compartments of the fund in any given country.

The information and data presented in this document are not to be considered as an offer or solicitation to buy, sell or subscribe to any securities or financial instruments or services.

Information, opinions and estimates contained in this document reflect a judgment at the original date of publication and are subject to change without notice. The management company has not taken any steps to ensure that the securities referred to in this document are suitable for any particular investor and this document is not to be relied upon in substitution for the exercise of independent judgment. Tax treatment depends on the individual circumstances of each investor and may be subject to change in the future. Before making any investment decision, investors are recommended to ascertain if this investment is suitable for them in light of their financial knowledge and experience, investment goals and financial situation, or to obtain specific advice from an industry professional.

The value and income of any of the securities or financial instruments mentioned in this document may fall as well as rise and, as a consequence, investors may receive back less than originally invested.

The investment guidelines are internal guidelines which are subject to change at any time and without any notice within the limits of the fund's prospectus.

The mentioned financial instruments are provided for illustrative purposes only and shall not be considered as a direct offering, investment recommendation or investment advice. Reference to a specific security is not a recommendation to buy or sell that security. Effective allocations are subject to change and may have changed since the date of the marketing material.

Past performance is not a guarantee or a reliable indicator of future performance. Performance data does not include the commissions and fees charged at the time of subscribing for or redeeming shares.

Any index data referenced herein remains the property of the Data Vendor. Data Vendor Disclaimers are available on assetmanagement.pictet in the “Resources” section of the footer.

This document is a marketing communication issued by Pictet Asset Management and is not in scope for any MiFID II/MiFIR requirements specifically related to investment research. This material does not contain sufficient information to support an investment decision and it should not be relied upon by you in evaluating the merits of investing in any products or services offered or distributed by Pictet Asset Management.

Pictet AM has not acquired any rights or license to reproduce the trademarks, logos or images set out in this document except that it holds the rights to use any entity of the Pictet group trademarks. For illustrative purposes only.

Cookie Policy

This website uses cookies to enhance user navigation and to collect statistical data. To refuse the use of cookies, change your settings or for more information, please click on the following link: Cookies policy. By continuing to browse this website, you accept the use of cookies for the above purposes.