Powerful weapon – helicopter money

So has the BOJ run out of options? We don’t think so. The central bank has yet to deploy its most powerful and, perhaps most controversial, tool – helicopter money.

An idea originally popularised by American economist Milton Friedman, helicopter money is defined as funding of fiscal expenditures via the creation of new base money and a promise that any increase in the monetary base will not be reversed.

Essentially, it means monetary authorities give people extra money in the form of a tax cut, vouchers or an increase in public spending. At the same time, the authorities make a "credible promise to be irresponsible"1 - pledging that they will not raise taxes at a later date to recoup this extra money. Assured that the extra money they receive will not be taken away later, people should then start spending that cash, boosting economic activity and inflation.

Let us suppose now that one day a helicopter flies over this community and drops an additional $1,000 in bills from the sky, which is, of course, hastily collected by members of the community. Let us suppose further that everyone is convinced that this is a unique event which will never be repeated.

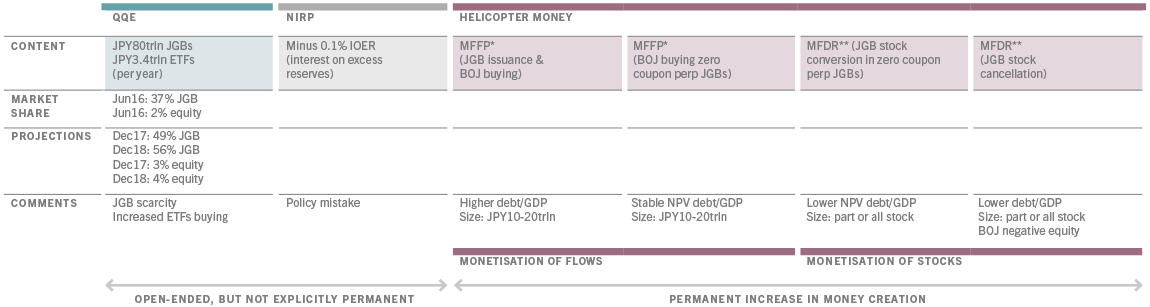

Helicopter money scenarios

How can the BOJ engage in a helicopter drop of money? Much of the discussion on helicopter money has centred on former US Federal Reserve Chairman Ben Bernanke’s idea for a money-financed fiscal programme (MFFP). This would involve either an increase in public spending or a tax cut that is financed with newly printed money by the central bank.

However, in the case of Japan, years of fiscal stimulus have failed to boost domestic demand and lift inflation as the public increased their savings in anticipation of higher tax rates to come.

What makes more sense, in our view, involves a sort of debt cancellation. Former Chairman of the UK Financial Services Authority Adair Turner has proposed that policy authorities convert some or all of the central bank’s JGB holdings into perpetual non-interest-bearing bonds, in what we call Money-Financed Debt Relief (MFDR).

We propose a more radical option of MFDR – an outright write-off (see chart above).

Essentially, the central bank prints money to buy a government bond. It then writes it off.

At first glance, that might seem radical. But that option looks far less extreme when set against where current policies are heading to.

We propose a more radical option of MFDR – an outright write-off .

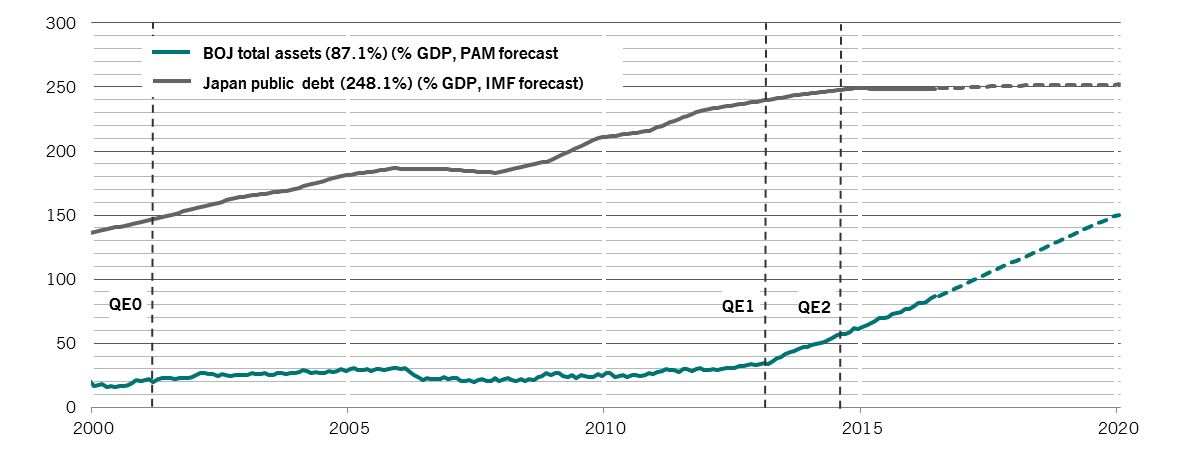

Assuming the BOJ’s debt buying programme runs into 2020 at the current pace, the BOJ’s total assets will have swollen to a record 150 per cent of GDP by mid-2020 (see Fig. 2). By then, its share of the JGB market will rise to a massive 63 per cent from 37 per cent today. Carrying on its purchases of exchange-traded equity funds at the present pace would take its share of Japan’s stock market – as measured by its total market capitalisation – to 10 per cent.

Cancelling even a small part of the public debt – let's say JPY10 trillion2 - can send a powerful message to the financial market and the wider public. In this case, the BOJ has permanently replaced JGBs with fresh base money worth JPY10 trillion.

We think MFDR should work well in highly indebted Japan. Debt write-offs will reduce the government’s outstanding debt and improve its credit profile. It can also promote private investment and consumption by incentivising businesses and households to reduce excess savings, leading to higher inflation.

Important legal information

This marketing material is issued by Pictet Asset Management (Europe) S.A.. It is neither directed to, nor intended for distribution or use by, any person or entity who is a citizen or resident of, or domiciled or located in, any locality, state, country or jurisdiction where such distribution, publication, availability or use would be contrary to law or regulation. The latest version of the fund‘s prospectus, Pre-Contractual Template (PCT) when applicable, Key Information Document (KID), annual and semi-annual reports must be read before investing. They are available free of charge in English on www.assetmanagement.pictet or in paper copy at Pictet Asset Management (Europe) S.A., 6B, rue du Fort Niedergruenewald, L-2226 Luxembourg, or at the office of the fund local agent, distributor or centralizing agent if any.

The KID is also available in the local language of each country where the compartment is registered. The prospectus, the PCT when applicable, and the annual and semi-annual reports may also be available in other languages, please refer to the website for other available languages. Only the latest version of these documents may be relied upon as the basis for investment decisions.

The summary of investor rights (in English and in the different languages of our website) is available here and at www.assetmanagement.pictet under the heading "Resources", at the bottom of the page.

The list of countries where the fund is registered can be obtained at all times from Pictet Asset Management (Europe) S.A., which may decide to terminate the arrangements made for the marketing of the fund or compartments of the fund in any given country.

The information and data presented in this document are not to be considered as an offer or solicitation to buy, sell or subscribe to any securities or financial instruments or services.

Information, opinions and estimates contained in this document reflect a judgment at the original date of publication and are subject to change without notice. The management company has not taken any steps to ensure that the securities referred to in this document are suitable for any particular investor and this document is not to be relied upon in substitution for the exercise of independent judgment. Tax treatment depends on the individual circumstances of each investor and may be subject to change in the future. Before making any investment decision, investors are recommended to ascertain if this investment is suitable for them in light of their financial knowledge and experience, investment goals and financial situation, or to obtain specific advice from an industry professional.

The value and income of any of the securities or financial instruments mentioned in this document may fall as well as rise and, as a consequence, investors may receive back less than originally invested.

The investment guidelines are internal guidelines which are subject to change at any time and without any notice within the limits of the fund's prospectus.

The mentioned financial instruments are provided for illustrative purposes only and shall not be considered as a direct offering, investment recommendation or investment advice. Reference to a specific security is not a recommendation to buy or sell that security. Effective allocations are subject to change and may have changed since the date of the marketing material.

Past performance is not a guarantee or a reliable indicator of future performance. Performance data does not include the commissions and fees charged at the time of subscribing for or redeeming shares.

Any index data referenced herein remains the property of the Data Vendor. Data Vendor Disclaimers are available on assetmanagement.pictet in the “Resources” section of the footer.

This document is a marketing communication issued by Pictet Asset Management and is not in scope for any MiFID II/MiFIR requirements specifically related to investment research. This material does not contain sufficient information to support an investment decision and it should not be relied upon by you in evaluating the merits of investing in any products or services offered or distributed by Pictet Asset Management.

Pictet AM has not acquired any rights or license to reproduce the trademarks, logos or images set out in this document except that it holds the rights to use any entity of the Pictet group trademarks. For illustrative purposes only.