Trump’s triumph – running the rule over the next US President

Trump's plans to deliver fiscal stimulus and tax cuts could provide a boost to growth but his views on global trade should concern investors.

Written by

Pictet Asset Management Strategy Unit

Share this article

Looking beyond the initial shock

The most divisive and bitter US presidential election campaign in living memory ended with Americans unexpectedly voting to upend the establishment, handing populist Donald Trump the keys to the White House.

The Republican candidate, whose proposed policies include building a wall along the Mexican border, raising barriers to global trade and slashing corporation tax, triumphed over his Democratic rival Hillary Clinton by securing far more than the 270 Electoral College votes he needed to become the 45th US President.

Longer term, there are reasons for investors to be both discouraged and encouraged by a Trump presidency.

Key to Trump’s electoral success were victories in the battleground states of Florida, Iowa, North Carolina and Ohio. Hammering home their advantage, Republicans also held on to their majorities in both the House of Representatives and the Senate.

As the US political map turned red so too did the world’s equity markets, which had largely dismissed the firebrand Republican’s chances.

Longer term, there are reasons for investors to be both discouraged and encouraged by a Trump presidency.

Trump no friend of trade

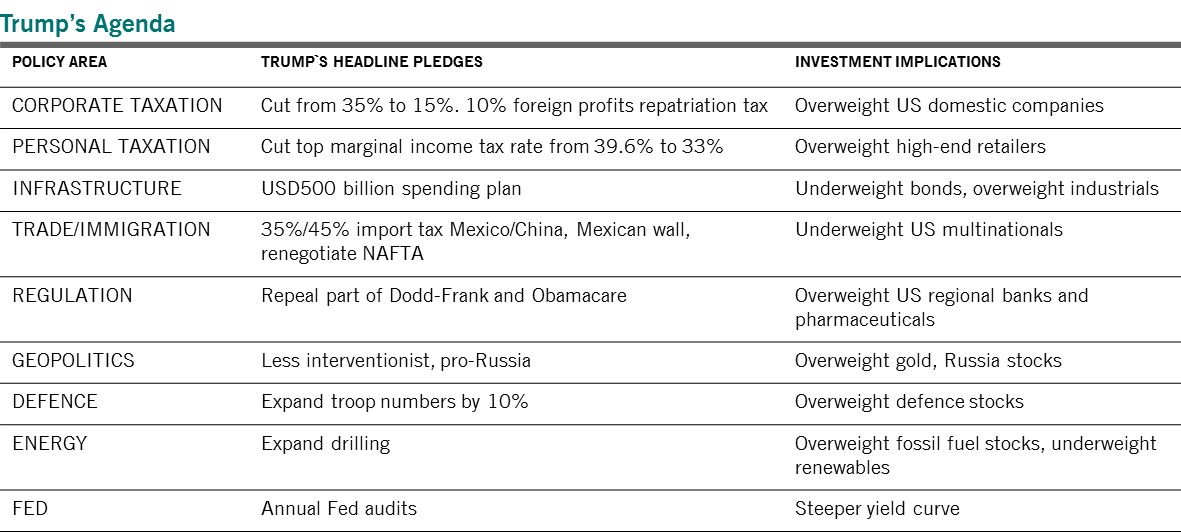

Perhaps the biggest threat to both world growth and financial markets is Trump’s protectionist streak. His proposals to raise trade tariffs – pledging, among other things, to levy a 45 per cent tax on Chinese imports – are a worry. His denouncement of China as a currency manipulator could also invite retaliation from the world’s second biggest economy.

At a time when global trade appears to be experiencing a structural decline, Trump’s stance casts a shadow over the world’s economic prospects.

Silver linings: tax, infrastructure

More positively, though, the Republican party’s clean sweep of the White House, House of Representatives and the Senate could mean an end to the policy gridlock that has plagued the US in recent years.

Trump’s plans to slash corporate tax rates from 35 per cent to 15 per cent and raise infrastructure spending by at least USD500 billion – both of which we see as positive for the US economy – are more likely to be enacted with his party now in full control of the legislature. Equally encouraging are his plans to incentivise US multi-nationals to repatriate the cash they have amassed overseas and proposals to simplify the tax code and cut the top rate of income tax.

Wider deficit, higher inflation, higher rates

The combination of tax cuts and public spending increases will however widen the US public sector deficit in the years to come, which is sure to have a major bearing on inflation and bond yields.

Based on the projections of the non-partisan Council for a Responsible Federal Budget, we estimate that the budget deficit will average around 6.1 per cent of GDP per year over the next 10 years, up from 3.1 per cent now. Higher deficits will undoubtedly result in greater inflationary pressures. Inflation should also show up in the labour market, where Trump’s proposals to limit immigration will probably lead to an acceleration in wage growth.

forecasted Winners and losers in the trump era

Source: Pictet Asset Management, November 2016

The upshot to all this is that US monetary policy will tighten at a faster pace than the Fed currently envisages. True, the central bank could delay its next interest rate hike until 2017 following the shock election result, as markets now suggest. But, longer term, it will probably be keener to tighten the monetary reins. This will result in higher bond yields and a steeper yield curve.

Rising inflation and a wider deficit could also spell an end to dollar strength. According to our models, the greenback is already some 20 per cent overvalued on a trade-weighted basis. Yet a complicating factor in determining the outlook for the dollar and US interest rates is Trump’s strained relationship with the Fed. A harsh critic of its ultra- loose monetary policies, Trump has led demands for the central bank to be audited, which could undermine the institution’s independence. He has also called for the resignation of Fed chair Janet Yellen, whose term expires in 2018.

US industrial, healthcare stocks could shine

Trump’s victory, and the uncertainty

that this represents, create a more

challenging environment for equities

and bonds, both of which remain expensive

by historic standards.

Fundamentally, we believe global markets

are caught between an improving

economic backdrop and a draining of

central bank stimulus. So far, the deterioration

in financial liquidity – characterised

by the re-start of the Fed’s reverse

repos and the liquidation of

reserves held by emerging market central

banks – has occurred primarily in

the US dollar market.

The silver lining is that, should market

conditions become more volatile, central

banks could step in once more with

additional stimulus.

Should market conditions become more volatile, central banks could step in once more with additional stimulus.

For all this, there should be some obvious winners from Trump’s proposals. His infrastructure spending plans, for instance, would be positive for industrial and construction stocks. Meanwhile, healthcare companies, which have been the worst performing stocks amid fears that a Clinton-led administration would introduce pricing curbs – could also stage a prolonged relief rally.

Defence and energy equipment stocks would benefit even though oil prices will be held in check by a boost in supply if drilling restrictions are removed.

The financial sector could experience a sustained rally too if, as Trump has suggested, he reverses some of the banking regulations implemented since the 2008 crisis.

Bonds to struggle

A Trump-led administration is however likely to have a negative effect on bond markets. Emerging market (EM) debt looks particularly vulnerable. Higher US bond yields would be a negative, as would any further decline in world trade. But not all EM bond markets would suffer. Debt issued by commodity exporters may gain if raw materials prices rally in response to higher US infrastructure spending.

Political risks hold sway

Looking further into 2017, riskier asset classes will remain under pressure in response to a shifting political climate. Markets will be waiting to see who Trump appoints to key positions in his cabinet – they will also be keen to see if the anti-establishment movement that powered this political outsider to the presidency continues to gather strength in Europe. The Italian constitutional referendum in December might provide evidence of that.

This marketing material is issued by Pictet Asset Management (Europe) S.A.. It is neither directed to, nor intended for distribution or use by, any person or entity who is a citizen or resident of, or domiciled or located in, any locality, state, country or jurisdiction where such distribution, publication, availability or use would be contrary to law or regulation. The latest version of the fund‘s prospectus, Pre-Contractual Template (PCT) when applicable, Key Information Document (KID), annual and semi-annual reports must be read before investing. They are available free of charge in English on www.assetmanagement.pictet or in paper copy at Pictet Asset Management (Europe) S.A., 6B, rue du Fort Niedergruenewald, L-2226 Luxembourg, or at the office of the fund local agent, distributor or centralizing agent if any.

The KID is also available in the local language of each country where the compartment is registered. The prospectus, the PCT when applicable, and the annual and semi-annual reports may also be available in other languages, please refer to the website for other available languages. Only the latest version of these documents may be relied upon as the basis for investment decisions.

The summary of investor rights (in English and in the different languages of our website) is available here and at www.assetmanagement.pictet under the heading "Resources", at the bottom of the page.

The list of countries where the fund is registered can be obtained at all times from Pictet Asset Management (Europe) S.A., which may decide to terminate the arrangements made for the marketing of the fund or compartments of the fund in any given country.

The information and data presented in this document are not to be considered as an offer or solicitation to buy, sell or subscribe to any securities or financial instruments or services.

Information, opinions and estimates contained in this document reflect a judgment at the original date of publication and are subject to change without notice. The management company has not taken any steps to ensure that the securities referred to in this document are suitable for any particular investor and this document is not to be relied upon in substitution for the exercise of independent judgment. Tax treatment depends on the individual circumstances of each investor and may be subject to change in the future. Before making any investment decision, investors are recommended to ascertain if this investment is suitable for them in light of their financial knowledge and experience, investment goals and financial situation, or to obtain specific advice from an industry professional.

The value and income of any of the securities or financial instruments mentioned in this document may fall as well as rise and, as a consequence, investors may receive back less than originally invested.

The investment guidelines are internal guidelines which are subject to change at any time and without any notice within the limits of the fund's prospectus.

The mentioned financial instruments are provided for illustrative purposes only and shall not be considered as a direct offering, investment recommendation or investment advice. Reference to a specific security is not a recommendation to buy or sell that security. Effective allocations are subject to change and may have changed since the date of the marketing material.

Past performance is not a guarantee or a reliable indicator of future performance. Performance data does not include the commissions and fees charged at the time of subscribing for or redeeming shares.

Any index data referenced herein remains the property of the Data Vendor. Data Vendor Disclaimers are available on assetmanagement.pictet in the “Resources” section of the footer.

This document is a marketing communication issued by Pictet Asset Management and is not in scope for any MiFID II/MiFIR requirements specifically related to investment research. This material does not contain sufficient information to support an investment decision and it should not be relied upon by you in evaluating the merits of investing in any products or services offered or distributed by Pictet Asset Management.

Pictet AM has not acquired any rights or license to reproduce the trademarks, logos or images set out in this document except that it holds the rights to use any entity of the Pictet group trademarks. For illustrative purposes only.

Cookie Policy

This website uses cookies to enhance user navigation and to collect statistical data. To refuse the use of cookies, change your settings or for more information, please click on the following link: Cookies policy. By continuing to browse this website, you accept the use of cookies for the above purposes.