Overview

The years since the bursting of the US credit bubble have forced investors to reassess many of the approaches and assumptions they previously held dear.

Developed market sovereign bonds, for example, can no longer be considered reliable or stable sources of income now that some USD9 trillion of these securities offer negative yields. At the same time, equities have experienced fits of volatility with alarming regularity, causing steep peak-to-trough investment losses that have been difficult to recover.

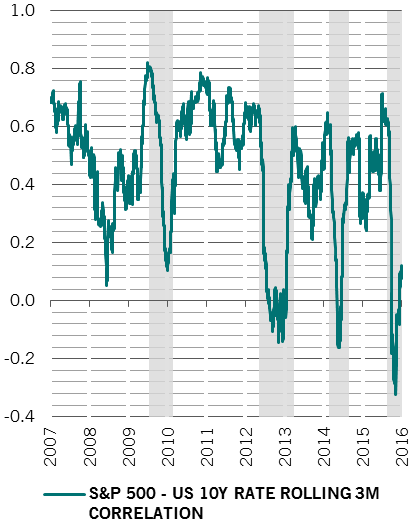

And all the while, the correlation between stocks and government bonds – asset classes that rarely moved in lockstep prior to the Great Recession – has tended to spike whenever central banks step up or scale back their monetary stimulus efforts.

The upshot of all this is that it has become more difficult to diversify the sources of a portfolio’s risk and return simply by combining fixed income and equity assets. Investors have consequently begun to look elsewhere for capital protection and diversification. They are also increasingly keen to access sources of return that lie beyond the reach of long-only equity and bond strategies.

In turn, hedge funds, which do not track a benchmark and are designed to provide a more favourable trade-off between return and volatility, have become a bigger feature of the financial landscape. Indeed, such strategies have seen their assets under management more than double in the past 10 years to some USD3 trillion.1 The eVestment database for institutional investors and consultants now tracks more than a dozen different hedge fund strategies, including macro, long/short equity, equity market neutral, event-driven and relative value.

Yet having more options can be a mixed blessing.

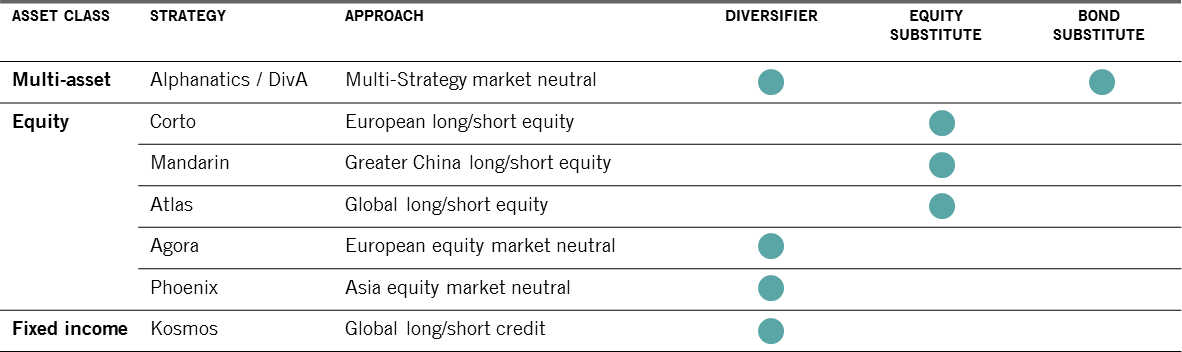

Although most hedge funds invest in established asset classes such as equity, bonds, loans, commodities and cash, they differ considerably in the extent to which they combine long and short positions, deploy leverage and use derivatives to generate alpha.

They also vary according to the type of market anomaly they seek to exploit. For example, some strategies aim to take advantage of the mis-pricing of securities within companies' capital structures or between instruments, regional markets, and industry sectors through various arbitrage strategies; others focus on predicting company-specific developments such as mergers and acquisitions that have the potential to trigger large moves in individual stock or bond prices.

Because investment approaches can differ greatly from fund to fund, it is perfectly reasonable to expect the return of, say, a long/short equity strategy to contrast with that of a macro strategy or an equity market neutral strategy under the same market conditions.

Faced with such complexity, prospective hedge fund investors naturally struggle to make an informed choice. But there are ways to chart a course through this challenging terrain. One way to do so is to look at the functions these alternative investments can perform within a portfolio.

This commentary aims to shed light on the functional properties of hedge funds.

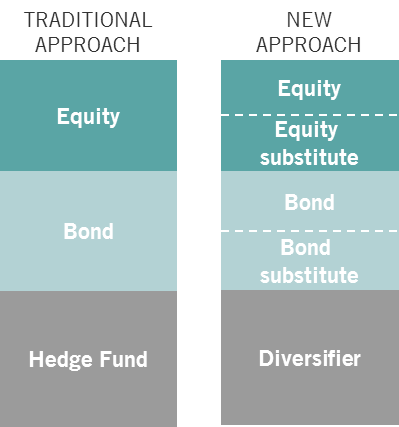

Specifically, our analysis builds on a growing body of evidence that shows such strategies can broadly play one of two roles in a balanced portfolio.

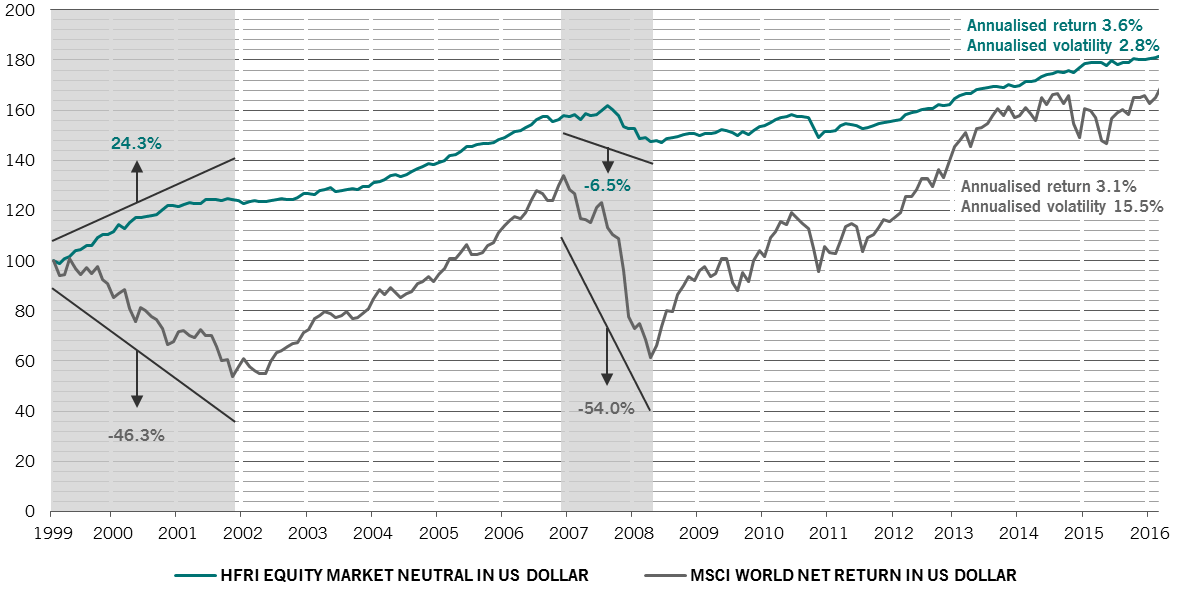

Some serve as diversifiers. These are strategies whose returns exhibit little or no correlation with those of mainstream asset classes and can therefore alter the risk-return characteristics of an entire portfolio.

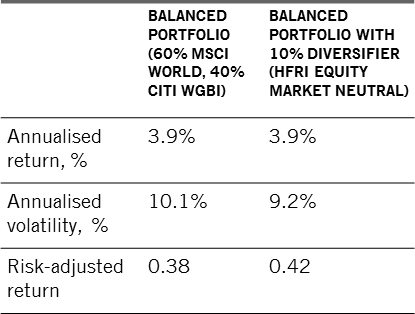

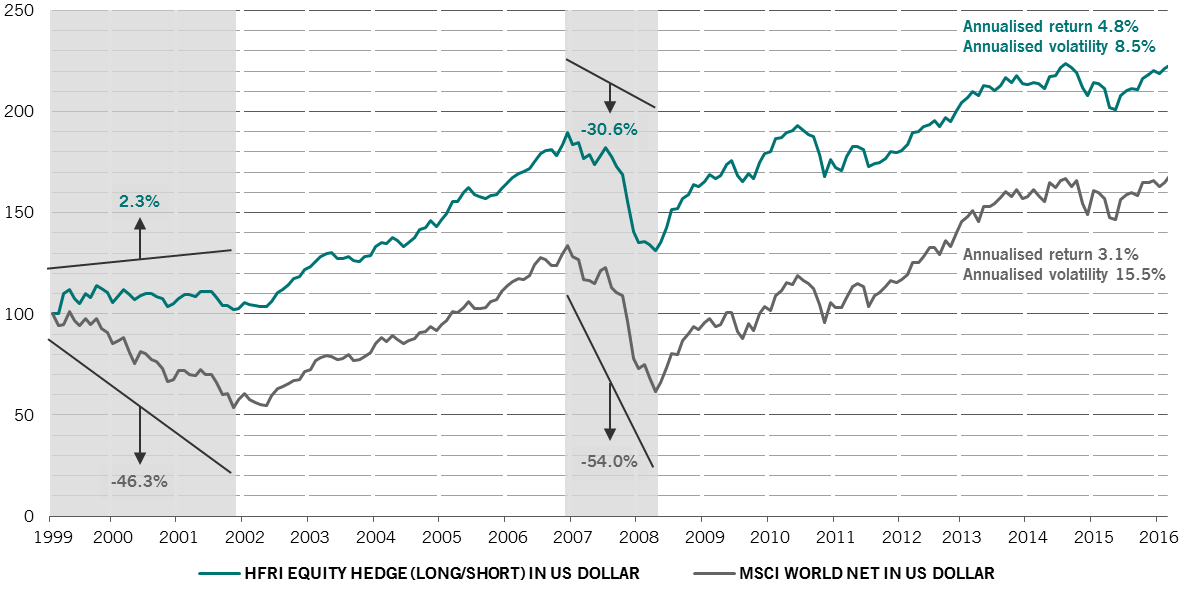

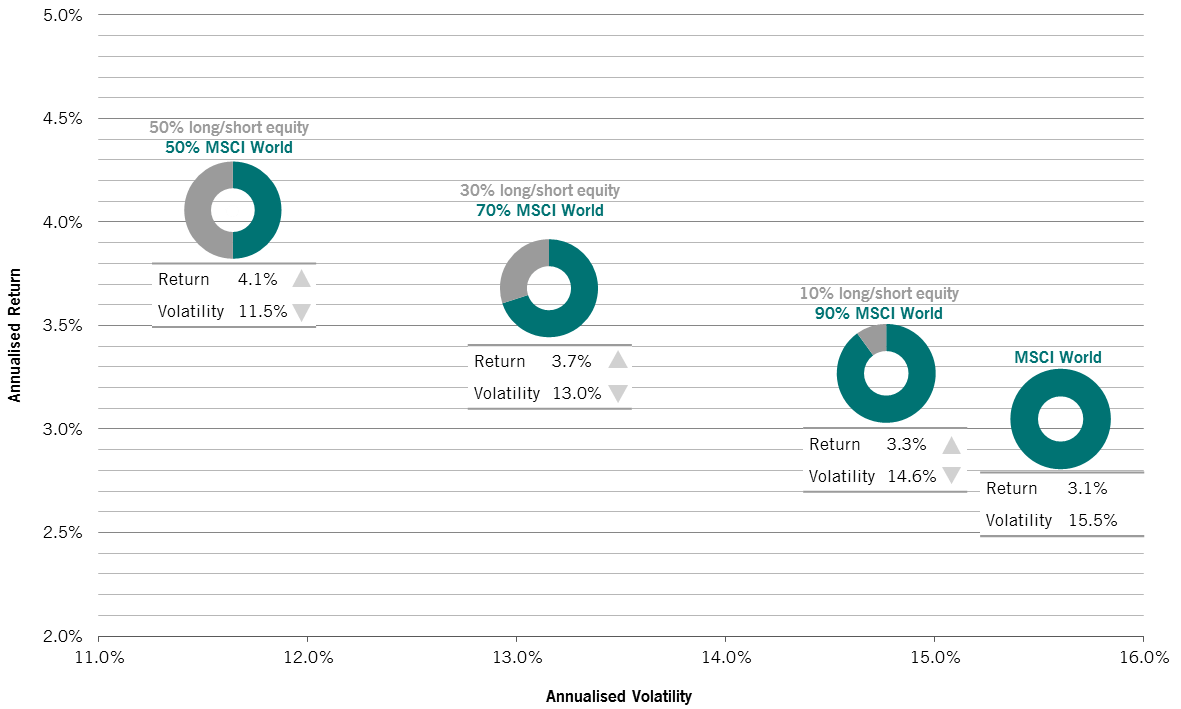

Others serve as substitutes, capable of replacing a portion of equity or fixed income investments to improve the overall return-volatility trade-off.