Overview: all about the growth

It seems that wherever investors look, there are reasons to rein in those animal spirits. For one thing, the political landscape remains treacherous. Brexit, North Korea’s sabre-rattling and US President Donald Trump’s unconventional approach to policymaking all have the potential to send markets into a tailspin next year. Another red flag is stocks’ remarkably long winning streak. Both the MSCI World and S and P 500 indices are now testing historical boundaries, having notched up gains in each of the past 12 months. Higher interest rates are also a concern. With the US Federal Reserve and the Bank of England having hiked borrowing costs and the European Central Bank soon to pare back its bond purchases, financial markets will no longer be able to feed on out-sized servings of monetary stimulus.

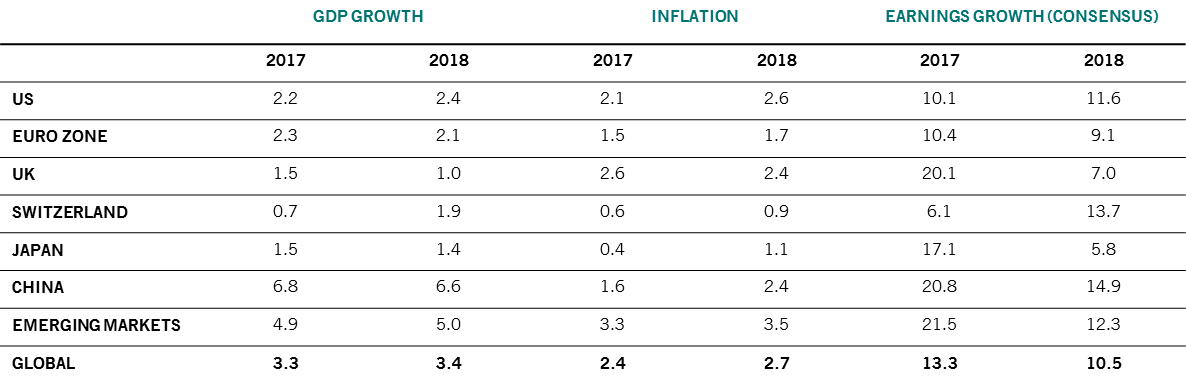

For all this, though, 2018 promises to be another good year for equities. The main reason is growth. We expect the global economy to expand at a healthy clip in 2018 – growing at 3.4 per cent against 3.3 per cent in 2017, surpassing economists’ consensus forecasts.

Encouragingly, the expansion in 2018 should be more broad-based than in recent years, characterised by a solid rise in government and business investment, as well as healthy consumer spending. Emerging economies should fare especially well, benefiting from low inflation and a recovery in commodity prices. Our enthusiasm for stocks isn’t dimmed by the prospect of additional interest rate hikes in the US. Even if the Fed tightens the monetary reins – we expect up to three hikes next year – real interest rates in the US, Europe and Japan will remain negative for quite some time.

But what is good for stocks will not be good for developed market bonds. Rate rises from the Fed are sure to weigh on what we consider to be expensive US government and corporate debt; we expect yields on these securities to ratchet higher over the course of 2018.

Heading in the opposite direction will be the US dollar, which our models indicate remains overvalued, particularly against emerging market currencies. We expect the greenback to continue its depreciation as inflationary pressures build in the US.

So much like any other year, investors will face a wall of worry in 2018. But as far as equities are concerned and emerging asset are concerned, they should be able to climb it.