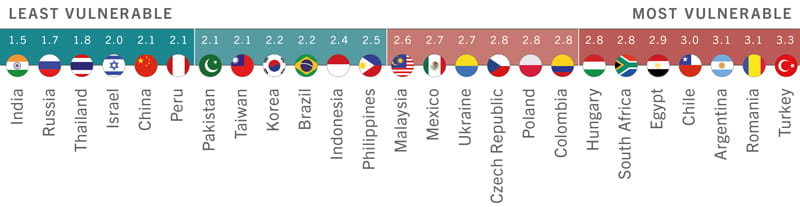

Which countries are most at risk from rising global rates?

Will tighter global rates cool the 'CATS'?

This month we focus on one of the main risks facing emerging markets over the next year: higher interest rates. In particular, we look at which emerging markets are likely to be most vulnerable and why. For this we use our proprietary 12 risk factor model, the output of which is presented below.

Fig. 1: Emerging countries scorecard: vulnerability to higher global rates (based on 12 risk factors)

Encouragingly the largest emerging markets are among the least vulnerable: India, Russia and China. Even Brazil, the final member of the BRIC club, is in the second quartile.

At the bottom of the table however we see a grouping of four reasonably large markets in terms of GDP: Chile, Argentina, Turkey and South Africa: the CATS. Let's look at the prospects for each.

i) Chile: on the rebound?

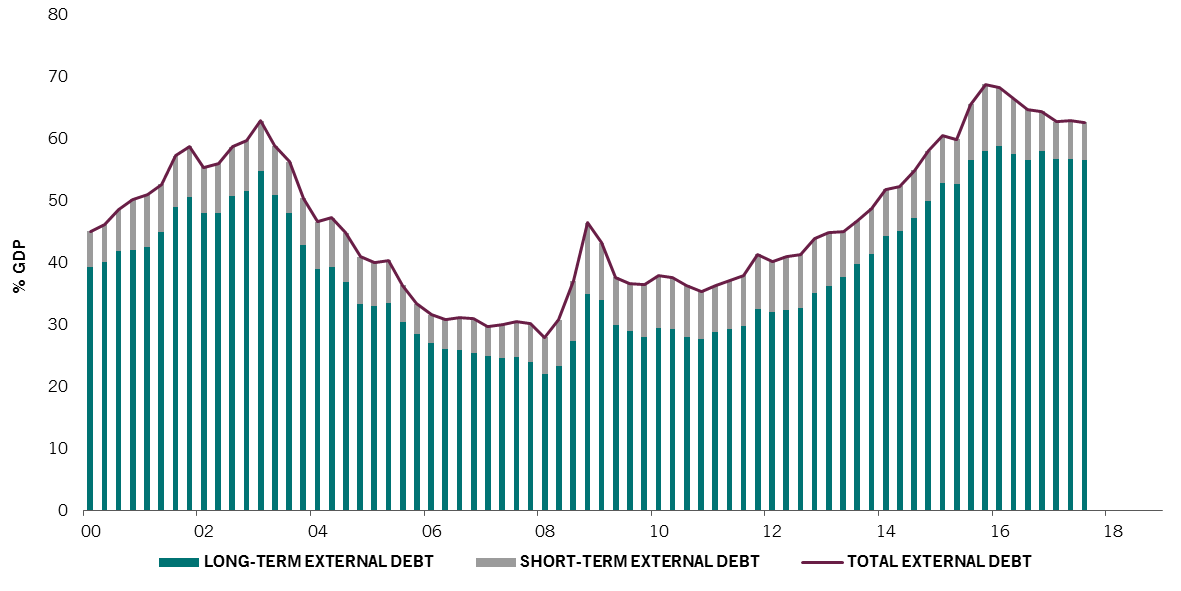

Chile’s poor ranking is surprising given its mature economy, solid political governance and overall good fundamentals. A key weakness appears to be external debt (61.3% of GDP), the highest among Latin American countries that we follow. The good news is only a small part of this external debt is short-term, 6.0% of GDP.

Fig. 2: Chile's external debt, maturity breakdown (% GDP)

We believe however a range of factors alleviate the risks in Chile:

- The local interest rate and inflation are currently low.

- The currency is stable and the risks of a substantial depreciation are very limited.

- Finally, Chile appears to be at a turning point in the business cycle after suffering from lower commodity prices in the past years.

ii) Don't cry for me Argentina...

The main components of Argentina’s low ranking are its fiscal balance, its current account, and its low score in foreign currency reserves.

Elected in late 2015, the government of Mauricio Macri is tackling all three.

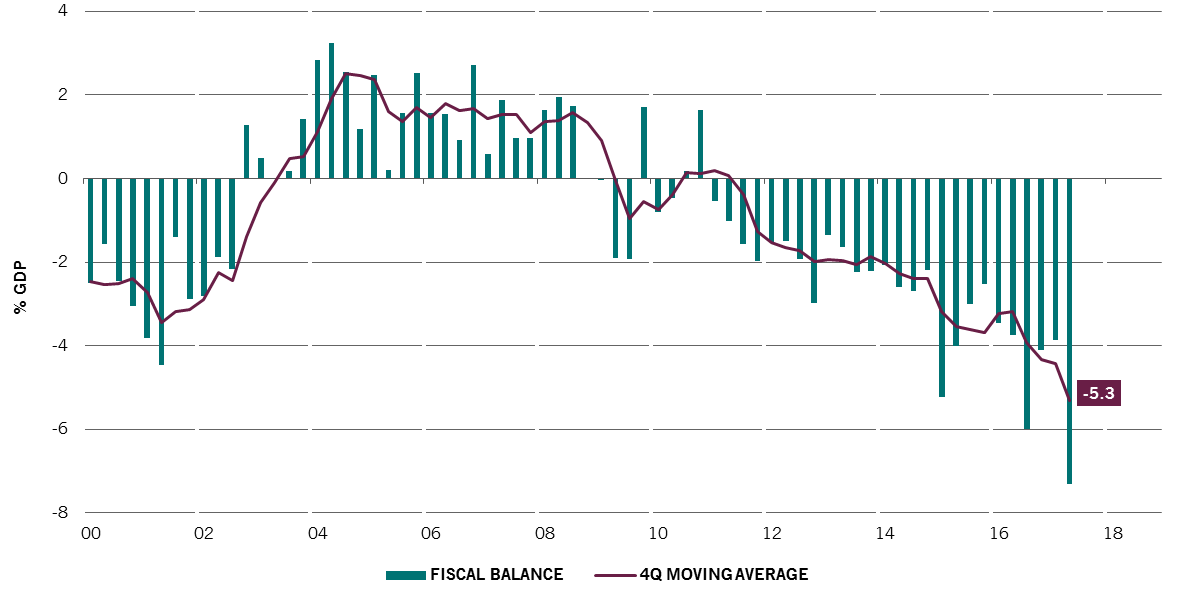

Plans to tackle the fiscal deficit have centred on hiking public transit and utility prices. This plan will take a while but we believe sweeping victories in October's mid-term elections has provided them with more leverage to implement reforms.

Fig. 3: Argentina's fiscal balance (% of GDP)

Meanwhile, the lifting of currency controls has led to doubling of foreign currency reserves between Q4 2015 from USD 24.5bn (equivalent to 4.1 months of imports) to USD 44.6bn by Q3 2017 (equivalent to 7.9 months of imports). While low by EM standards, reserves should continue to improve given the brighter outlook for exports and foreign investment.

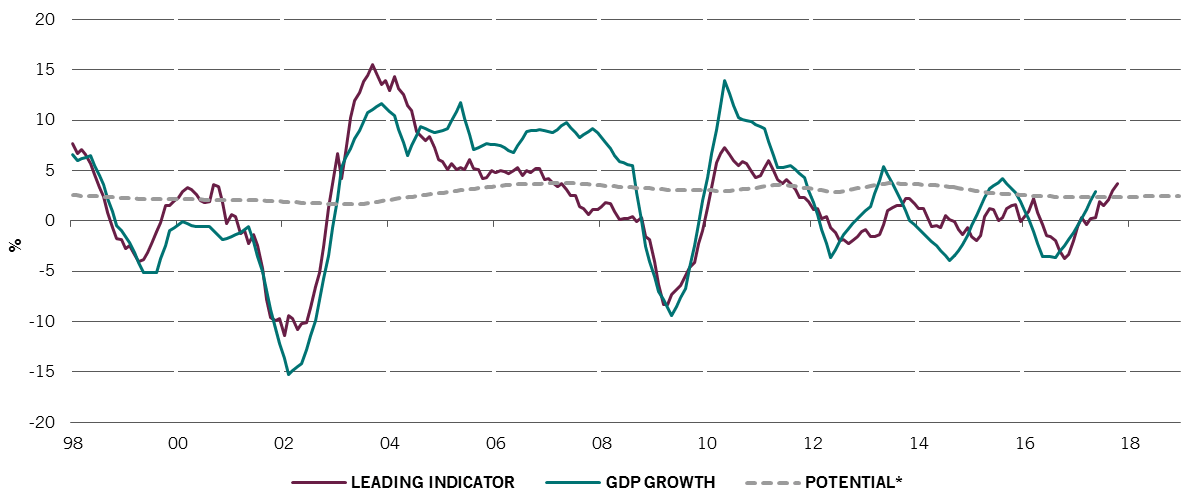

The economy is recovering, but inflation is still too high

One negative remains inflation, which is still high and persistent, harming consumption. Inflation should go down, but we believe the ambitious target of 8% to 12% next year is out of reach.

Fig. 4: Argentina's real GDP growth and leading indicator growth

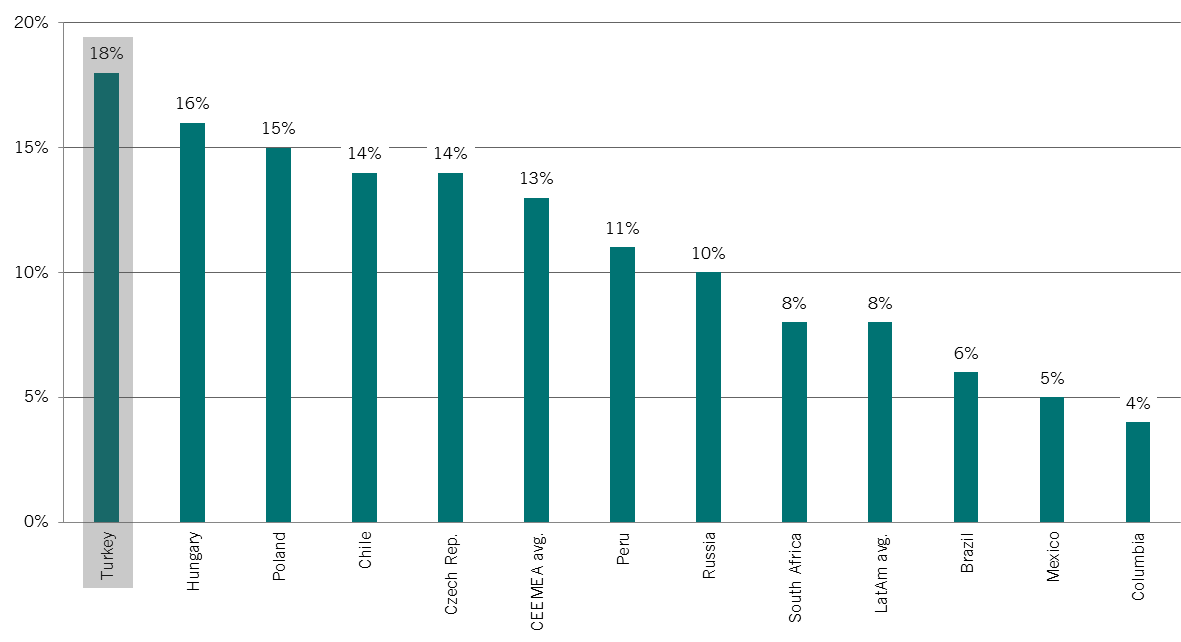

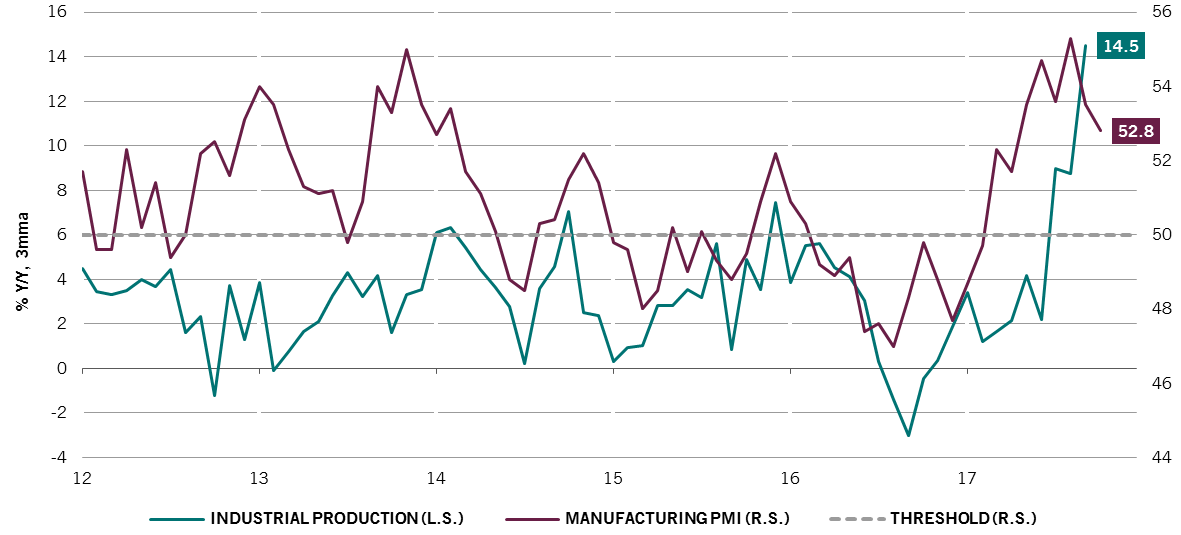

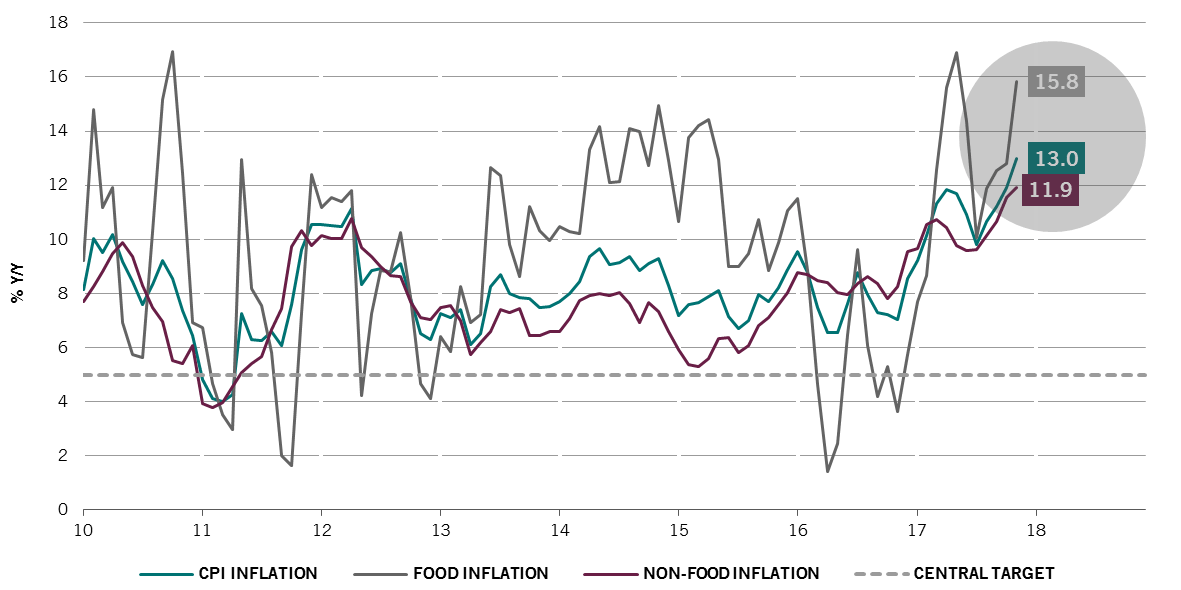

iii) Turkey: handle with care

Inflation - a growing problem

iv) Crunch time for South Africa?

Finally, South Africa is another market that we are not surprised to see near the bottom of the ranking. Political risk remains a key issue under the discredited leadership of President Jacob Zuma. An inflexion point might be nearing however.

This week’s conference of the ruling ANC party saw the selection of deputy president Cyril Ramaphosa as new leader of the party, narrowly beating Nkosazana Dlamini-Zuma (Zuma’s ex wife). In the immediate aftermath of this announcement the South African rand rallied against the US dollar .

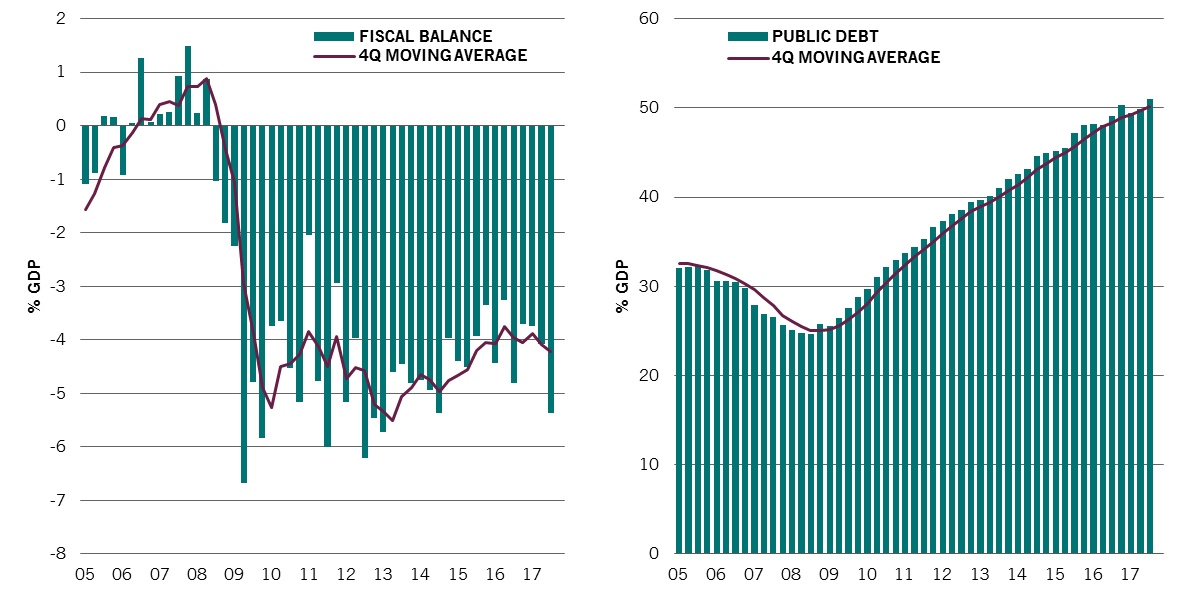

As the charts below demonstrate, the main risk for South Africa is on public finances given the large fiscal deficit and rising public debt.

Looking for silver linings, the rebound in commodity prices is providing some support. The current account is improving led by the rising trade surplus. This should contain the rand depreciation & help secure foreign capital inflows.

In conclusion: look at the business cycle

Finally, the momentum of each market's business cycle - positive or negative - will also have an impact on how well they are able to weather rising global rates. It will also affect how quickly they can improve their underlying risk factor scores.

In the chart below we plot each of the ‘CATS’ in our Pictet Regime Indicator, which tracks where different regions are in the business cycle, and shows the asset classes most in favour in each growth/inflation regime.

To summarise:

- In Chile we expect growth to improve, although not substantially, and inflation should remain low.

- Argentina should see growth improve, and whilst inflation will fall it will remain very high.

- South Africa's low growth prospects might improve marginally depending on the direction of the political transition.

- Turkey's growth looks likely to slow somewhat and inflation remain high.