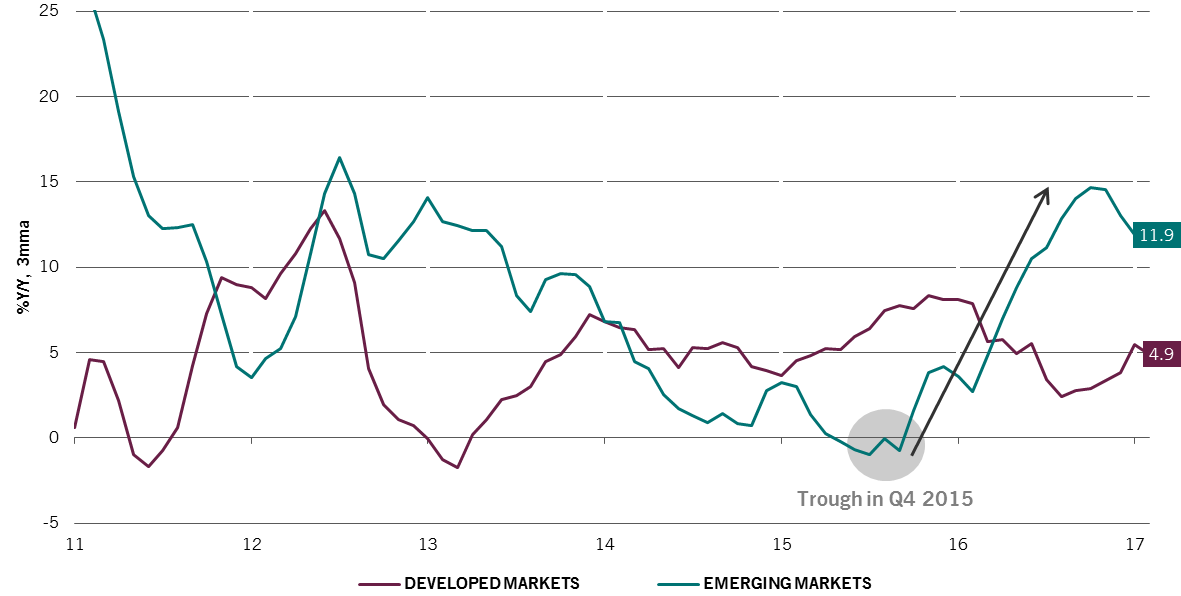

The rebound in EM car sales growth since Q4 2015 appears to bode well for future GDP prospects in emerging markets. We believe that car sales are one of the most reliable indicators of wider consumer spending and confidence.

Growth in EM car sales is also some way ahead of developed markets, despite a recent roll-over (which we expect to be short-lived).

Em vs. DM car sales growth

Volume, % y/y, 3-month moving average

Source: Pictet Asset Management, CEIC, Datastream, data as at 01.01.2017.

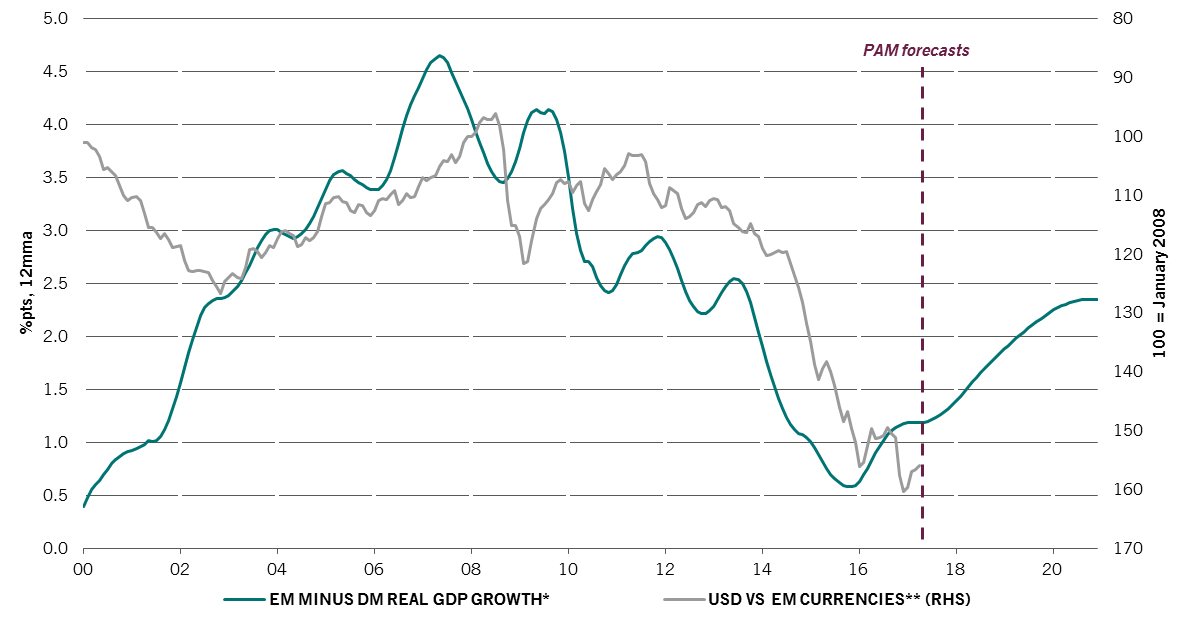

Plenty in the EM 'tank' implies strong prospects for EM growth and currencies

EM growth set to outperform DM

The positive picture in car sales and in our broader leading indicator of activity (see EM leading indicator & GDP chart in next section) are mirrored in our current forecasts for EM growth relative to DM (green line in the below chart).

EM currencies likely to appreciate

If our optimism on EM growth proves correct, EM currencies (grey line in the below chart) look set to appreciate versus the US dollar as this tends to follow with a lag.

EM vs. DM GDP growth & USD vs. EM currencies

Source: Pictet Asset Management, CEIC, Datastream, USD vs. EM currencies data as at 01.04.2017.

* Unweighted 31 EM GDP growth / **Unweighted 31 EM exchange rates.

02

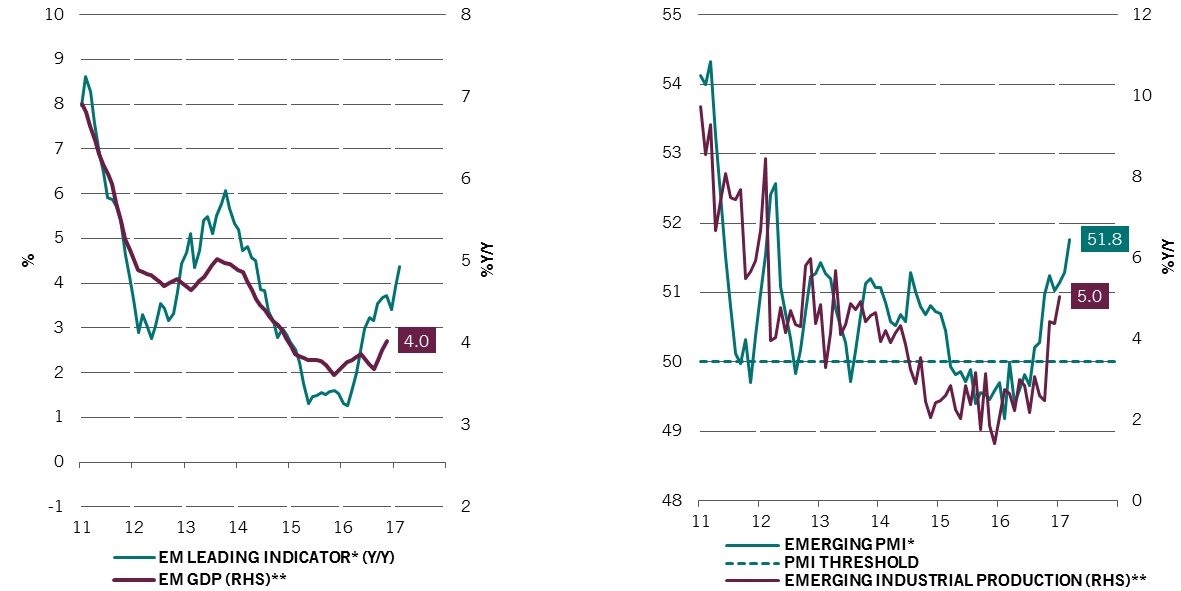

EM health check

Both the demand and the supply sides appear in good health

Our proprietary Pictet Emerging Markets leading indicator* is showing strong momentum.

On the corporate/supply side, both EM PMI and industrial production readings further reinforce the positive signs observed on the demand side.

*The Pictet Emerging Markets leading indicator is assembled using some 240 underlying indicators across 24 emerging markets that focus on rate-sensitive consumption (car sales, housing, etc.)

EM leading indicator & GDP (left) / EM PMI & industrial production (right)

Source: Pictet Asset Management, CEIC, Datastream. Left-hand chart: EM leading indicator data as at 01.02.2017; EM GDP data as at 01.11.2016.

*GDP-weighted average of 24 countries leading indicators. **GDP-weighted average of 30 countries real GDP. Right-hand chart: EM PMI data as at 01.03.2017; industrial production data as at 01.01.2017.

*GDP-weighted average of 16 manufacturing PMI surveys. **GDP-weighted average of 32 countries industrial production.

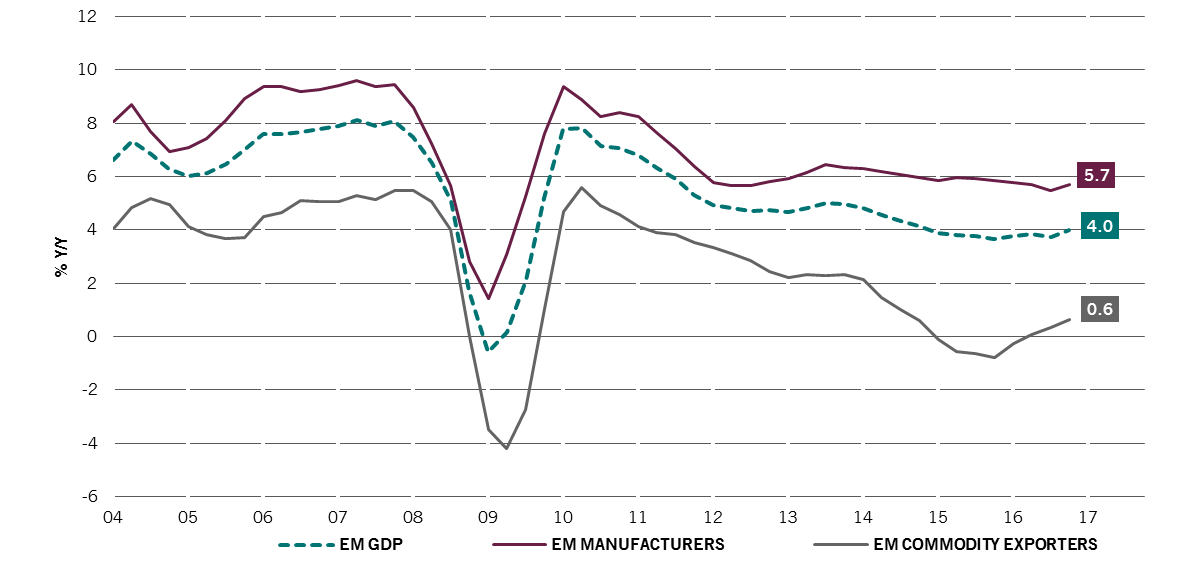

We expect the gap between EM manufacturers and commodity exporters to at least converge to the long-term average

Commodity exporters should see their GDP recover

We think a key lens to differentiate between emerging markets is that of manufacturers vs. commodity exporters.

Given that the long-term average growth gap between commodity exporters and manufacturers is 400 bps - and assuming manufacturers retain their current stable growth trend - this implies further upside for growth for EM commodity exporters.

Emerging GDP growth: manufacturers vs. commodity exporters

Source: Pictet Asset Management, CEIC, Datastream, data as at 01.10.2016.

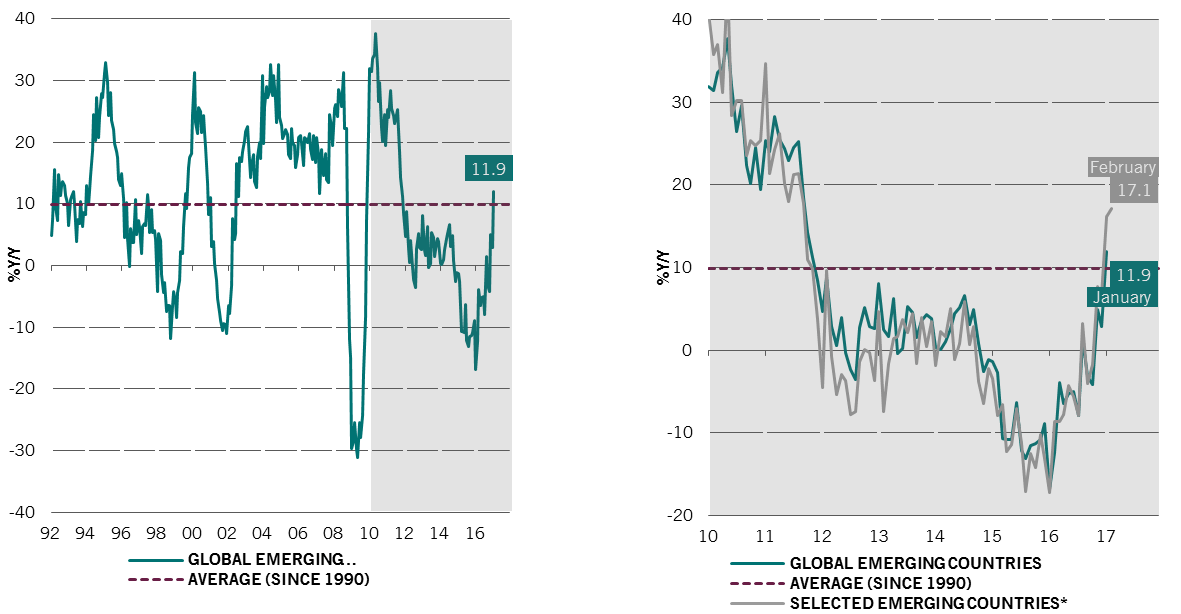

Emerging markets' exports appear to be on the mend

Nominal exports above long-term average for the first time since 2011

Rounding off a range of positive EM indicators this month are nominal global emerging markets’ exports, which ended 2016 above their long-term average for the first time since 2011.

Furthermore, as the right hand chart shows, this rebound could be accelerating in February if early reporting EMs are matched by the wider market.

Emerging nominal exports

Long-term trend (left) and since 2010 with early February 2017 data (right) - In USD

Source: Pictet Asset Management, CEIC, Datastream. Left-hand chart: data as at 01.01.2017. Right-hand chart: global EM countries data as at 01.01.2017; selected emerging countries data as at 01.02.2017.

* EM countries with most recent data: Korea, Taiwan, Brazil, Chile.

03

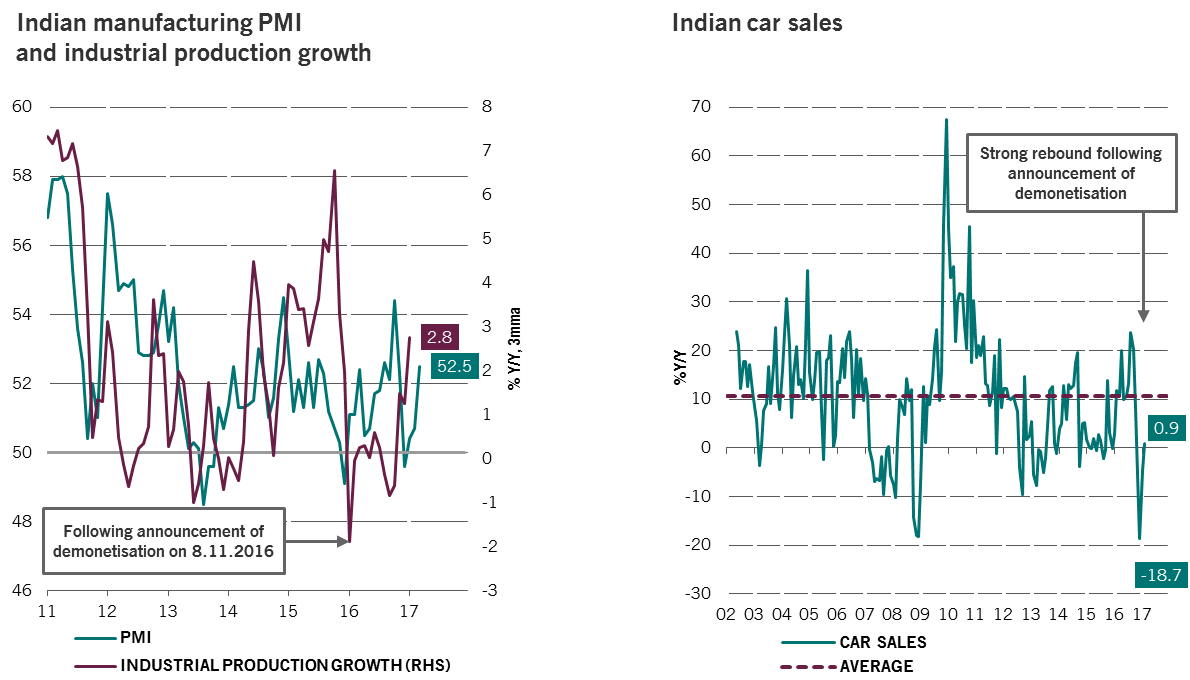

In focus: India

Indian activity seems to be rebounding from the impact of demonetisation

After Prime Minister Modi’s surprise announcement of demonetisation on 8 November 2016, India went through a period of economic disruption. This seems to be over now with PMI and industrial production picking up again.

This is also reflected in the consumer sentiment as illustrated through our favoured indicator of car sales, which have risen back into positive territory towards long-term average levels.

Indian manufacturing PMI and industrial production growth (left) / Indian car sales (right)

Source: Pictet Asset Management, CEIC, Datastream. Left-hand chart: PMI data as at 01.03.2017; industrial production growth data as at 01.01.2017. Right-hand chart: Car sales data as at 01.02.2017

04

Market watch

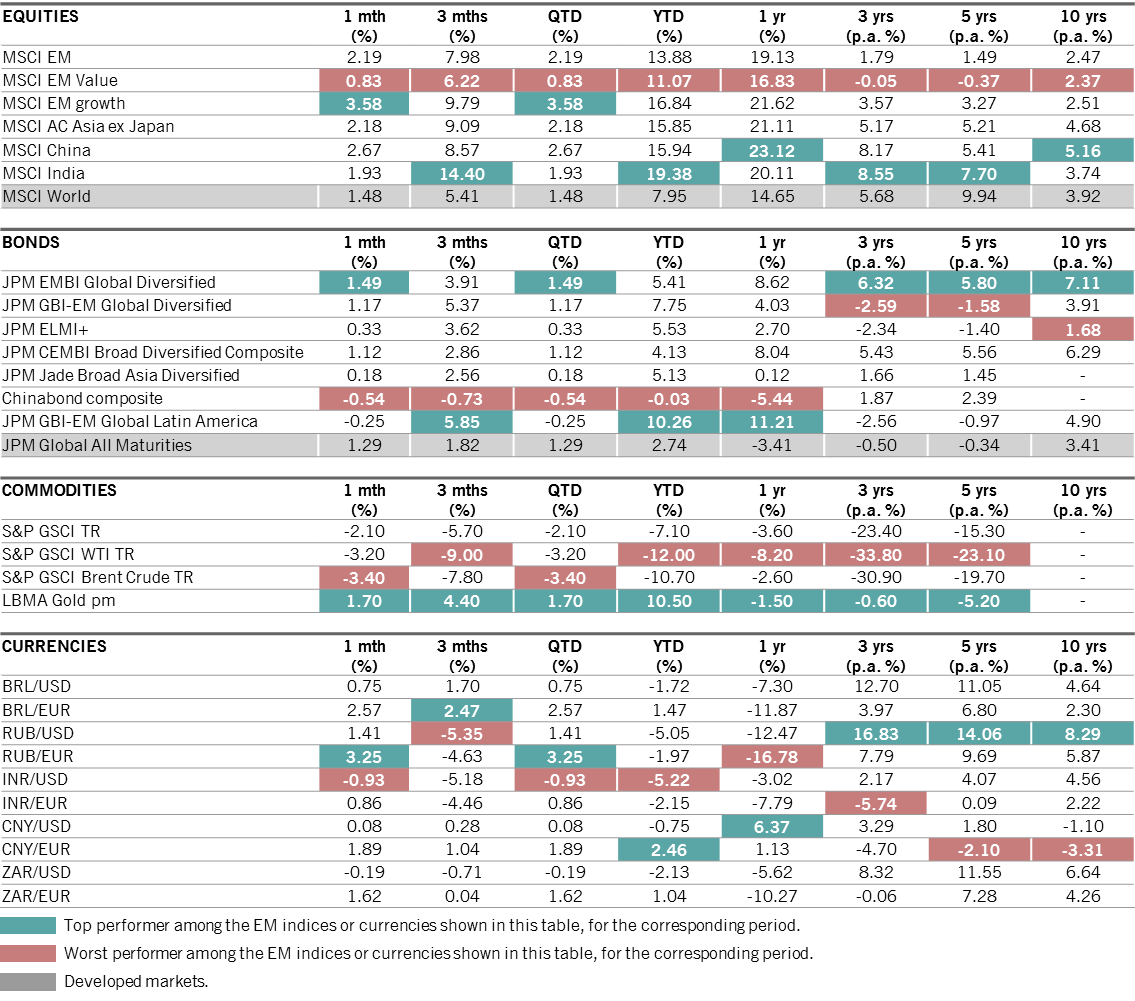

Key market data

As at 30.04.2017

Source: Datastream, Bloomberg, data as at 30.04.2017 and in USD. Equity indices are quoted on a net dividend reinvested basis; bond and commodity indices are quoted on a total return basis. The currency rates evolution is treated as a performance calculation based on FX rates.

About

Patrick Zweifel

Patrick Zweifel joined Pictet in 1997. He is Chief Economist at Pictet Asset Management. Before assuming his current position in 2009, he was head of the “Macro Research Team” at Pictet Private Wealth Management. In particular, he had economic research responsibility for emerging markets and Japan, and for the development of quantitative models on major asset classes, primarily foreign exchange models. Before joining Pictet he was a research assistant in econometrics and monetary theory and worked on international research projects for the World Bank and the European Union. He holds a PhD in econometrics from the University of Lausanne.

About

Alain Nsiona Defise

Alain Nsiona Defise joined Pictet Asset Management in 2012 and is Co-Head of Emerging Markets - Corporate. Previously, Alain worked at JPMorgan in London where he was in charge of managing the Emerging Corporate franchise, worth over USD 2 billion. Prior to JPMorgan, he worked for nine years at Fortis Investments, where he started as a senior credit analyst focusing on the high yield market. He later moved to Emerging Markets Fixed Income as a senior portfolio manager building the emerging corporate business. He holds a Master's in Business Engineering from Solvay Business School, Brussels and a Diploma in Financial Analysis from the European Federation of Financial Analysts Societies (EFFAS).

About

John Moorhead

An ardent believer in value investing, John Moorhead has been looking at emerging market stocks through the value lens since joining Pictet Asset Management as a Materials analyst in 2008. His research-focused background is most evident in the influence he has had in shaping the group’s rigorous investment process. In addition to his responsibilities as Head of Emerging Equities, John is also part of the portfolio management teams for the Global Emerging Markets and the Global Emerging Market High Dividend strategies. John graduated with a Bachelor of Mining Engineering (Hons) from the University of Queensland and holds a Graduate Diploma from the Securities Institute of Australia. He is a CFA charterholder.

This marketing material is issued by Pictet Asset Management (Europe) S.A.. It is neither directed to, nor intended for distribution or use by, any person or entity who is a citizen or resident of, or domiciled or located in, any locality, state, country or jurisdiction where such distribution, publication, availability or use would be contrary to law or regulation. The latest version of the fund‘s prospectus, Pre-Contractual Template (PCT) when applicable, Key Information Document (KID), annual and semi-annual reports must be read before investing. They are available free of charge in English on www.assetmanagement.pictet or in paper copy at Pictet Asset Management (Europe) S.A., 6B, rue du Fort Niedergruenewald, L-2226 Luxembourg, or at the office of the fund local agent, distributor or centralizing agent if any.

The KID is also available in the local language of each country where the compartment is registered. The prospectus, the PCT when applicable, and the annual and semi-annual reports may also be available in other languages, please refer to the website for other available languages. Only the latest version of these documents may be relied upon as the basis for investment decisions.

The summary of investor rights (in English and in the different languages of our website) is available here and at www.assetmanagement.pictet under the heading "Resources", at the bottom of the page.

The list of countries where the fund is registered can be obtained at all times from Pictet Asset Management (Europe) S.A., which may decide to terminate the arrangements made for the marketing of the fund or compartments of the fund in any given country.

The information and data presented in this document are not to be considered as an offer or solicitation to buy, sell or subscribe to any securities or financial instruments or services.

Information, opinions and estimates contained in this document reflect a judgment at the original date of publication and are subject to change without notice. The management company has not taken any steps to ensure that the securities referred to in this document are suitable for any particular investor and this document is not to be relied upon in substitution for the exercise of independent judgment. Tax treatment depends on the individual circumstances of each investor and may be subject to change in the future. Before making any investment decision, investors are recommended to ascertain if this investment is suitable for them in light of their financial knowledge and experience, investment goals and financial situation, or to obtain specific advice from an industry professional.

The value and income of any of the securities or financial instruments mentioned in this document may fall as well as rise and, as a consequence, investors may receive back less than originally invested.

The investment guidelines are internal guidelines which are subject to change at any time and without any notice within the limits of the fund's prospectus.

The mentioned financial instruments are provided for illustrative purposes only and shall not be considered as a direct offering, investment recommendation or investment advice. Reference to a specific security is not a recommendation to buy or sell that security. Effective allocations are subject to change and may have changed since the date of the marketing material.

Past performance is not a guarantee or a reliable indicator of future performance. Performance data does not include the commissions and fees charged at the time of subscribing for or redeeming shares.

Any index data referenced herein remains the property of the Data Vendor. Data Vendor Disclaimers are available on assetmanagement.pictet in the “Resources” section of the footer.

This document is a marketing communication issued by Pictet Asset Management and is not in scope for any MiFID II/MiFIR requirements specifically related to investment research. This material does not contain sufficient information to support an investment decision and it should not be relied upon by you in evaluating the merits of investing in any products or services offered or distributed by Pictet Asset Management.

Pictet AM has not acquired any rights or license to reproduce the trademarks, logos or images set out in this document except that it holds the rights to use any entity of the Pictet group trademarks. For illustrative purposes only.

Cookie Policy

This website uses cookies to enhance user navigation and to collect statistical data. To refuse the use of cookies, change your settings or for more information, please click on the following link: Cookies policy. By continuing to browse this website, you accept the use of cookies for the above purposes.