Sizing up China

An example of the nation's overcapacity

how big China is and its manufacturing output.

For example, almost one out of four manufactured goods is produced in China.

Today, Chinese policymakers are walking a tight rope to cut debt levels and rebalance the economy.

The big question is: how much growth will they sacrifice in the process?

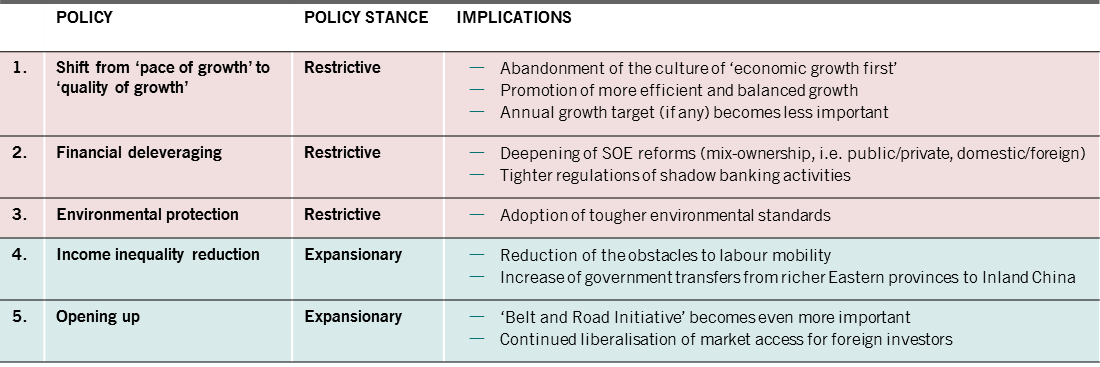

What does China's policy mix mean for growth?

Policies outlined at last month's 19th National Congress, aimed by Xi Jinping at producing a "better life" for China’s economy and people, suggest slower economic growth but, on balance, point to a more sustainable future for China.

Looking at policy areas, the two stimulative initiatives may be ambitious but will not be enough to offset the impact of restrictive ones.

More details will be disclosed in late December at the Central Economic Work Conference.

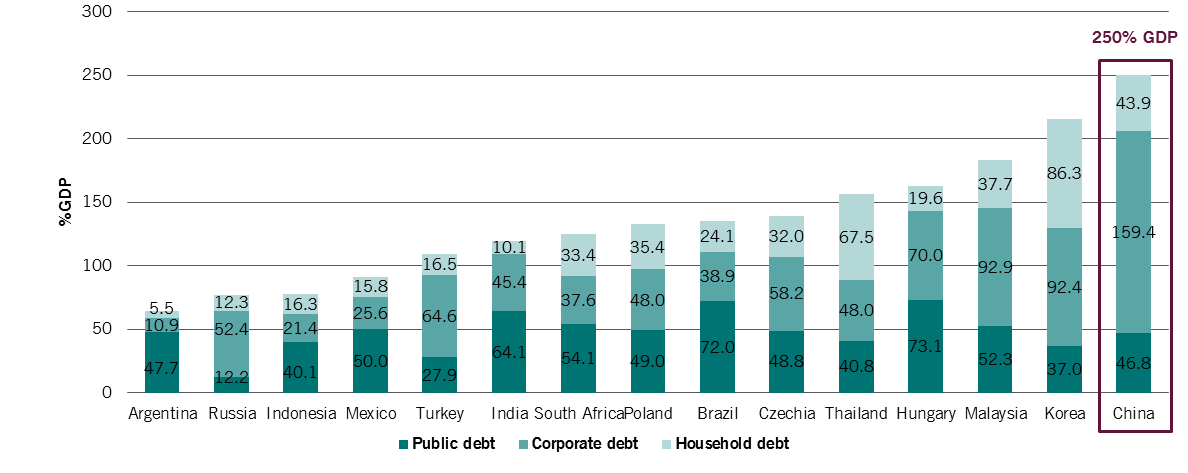

Could debt levels cause a crisis?

Currently at 250 per cent of GDP, China's debt burden may be big but is still under control.

The main risks are the financial liberalisation and the opening up of the capital account, which have been catalysts in previous EM financial crises. There are however mitigating factors, most importantly:

- the government owns the main creditors (large banks) and debtors (2/3 of corporate debt is SOE)

- Chinese debt is still essentially domestically held.

What's China doing to manage its debt levels?

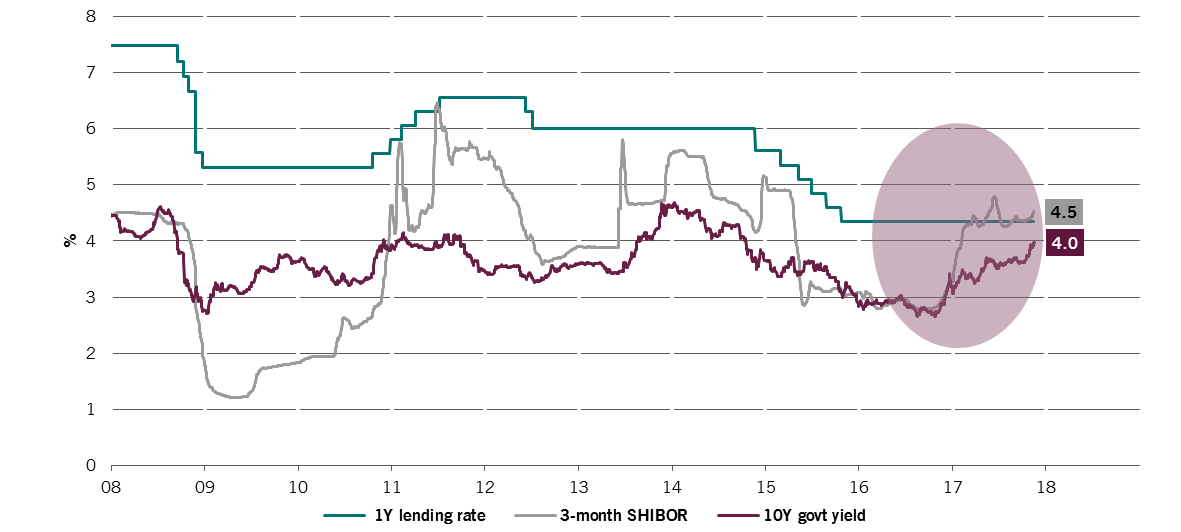

Tighter monetary policy has helped mitigate the risks posed by China's debt burden. Since late last year, monetary authorities have allowed a steady increase in money market rates. As a result, interest rates have bounced from their lows in October 2016 (Fig.4).

This tightening helps anchor RMB expectations ahead of the US rate tightening cycle by containing the interest rate spread between China and the US.

What rates of growth can we expect in the next decade?

China’s economy is maturing: it has become the world's third largest debt market, second largest economy and since 2010, the largest manufacturer. But its corporate sector is massively over-leveraged. And history shows that this tends to lead to lower future growth rates.

What growth rate can we expect in future?

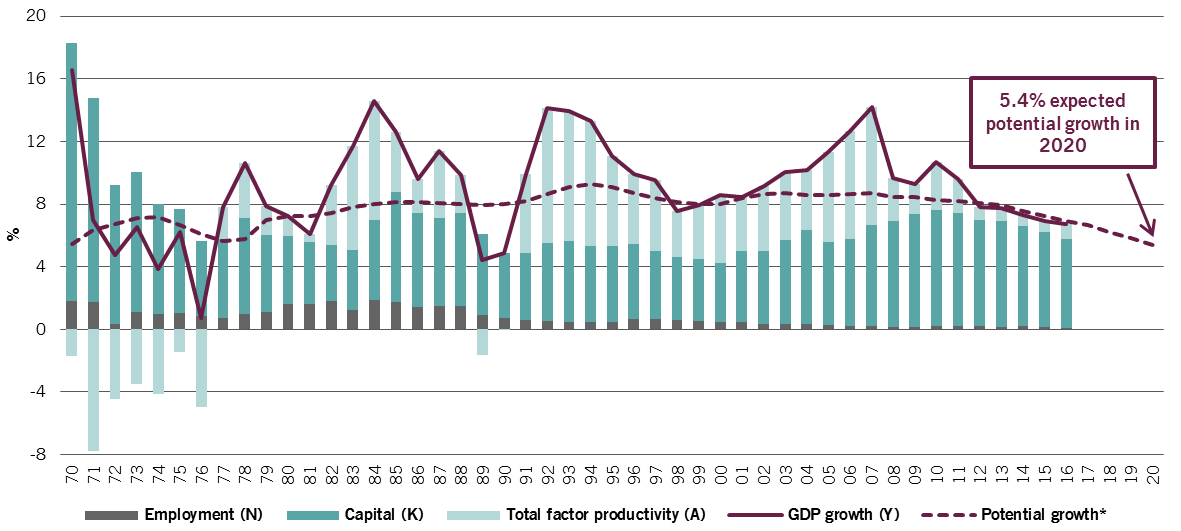

We have estimated the growth trajectory based on three calculation models: leverage levels seven years prior and post their peak, GDP per capita and production factors (Fig.5).

All three approaches point to growth of 4 to 5 per cent over the next 5-7 years.

We therefore expect growth targets to be lowered over the next few years, starting next year, while the rebalancing of the economy should continue from investment towards consumption.

Source: Pictet Asset Management, CEIC, Datastream. Data to January 2016 except for potential growth data which is up to January 2020. *Mixed forecasting: non-accelerating inflation growth of output, HP filtering, working-age population.

The city of Shenzhen in China.