Is your global equity portfolio over-exposed to highly priced tech names and other growth equities? If so where do you go now?

Written by

Reda Jürg Messikh

Head of Quest Investments

Share this article

Global equities in aggregate appear expensive

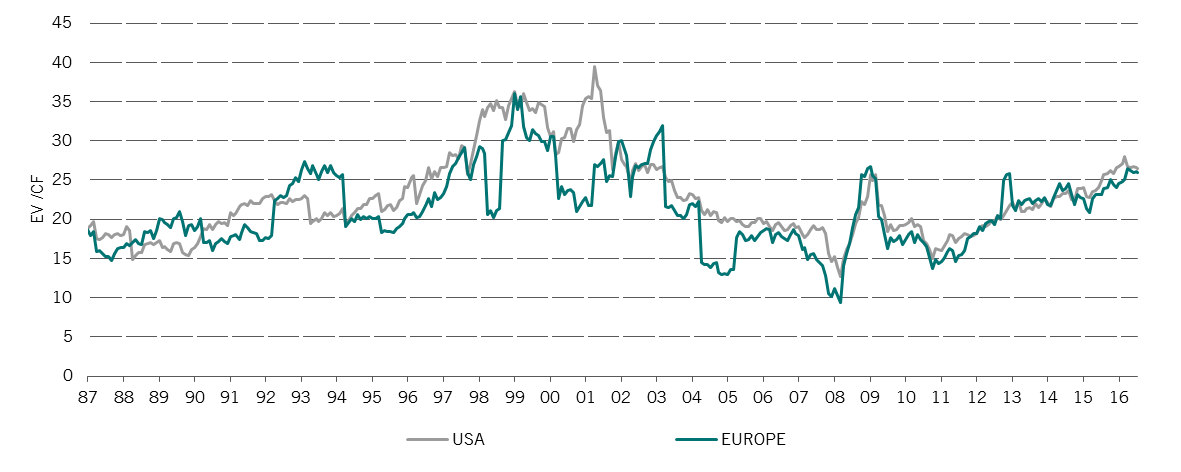

Global equities have continued to rise strongly this year with YTD returns pencilled in at 13.47%*. Using the Enterprise Value/Cashflow (EV/CF) multiple, global equities have not been this highly valued since the dot-com boom in the early 2000s. Furthermore, as Chart 1 shows this is no longer just the case in the US, as European equities are now almost as highly valued.

CHART 1 : Valuation multiple (EV/CF) of US equities vERSUs Europe equities

*Source: MSCI World, Datastream, data as at 31.08.2017 and in USD. Equity indices quoted on the basis of net dividend reinvested.

Why do we use EV/CF as a valuation multiple as opposed to the more universal Price Earnings (PE) ratio? In short, because we think the reliance of PE on the income statement provides only one side of the story, and earnings are one of the easiest figures to massage through creative accounting, buybacks, and capital structure. In our view, using an enterprise-based and cash flow approach provides a fuller picture.

A 'two-speed' equity market

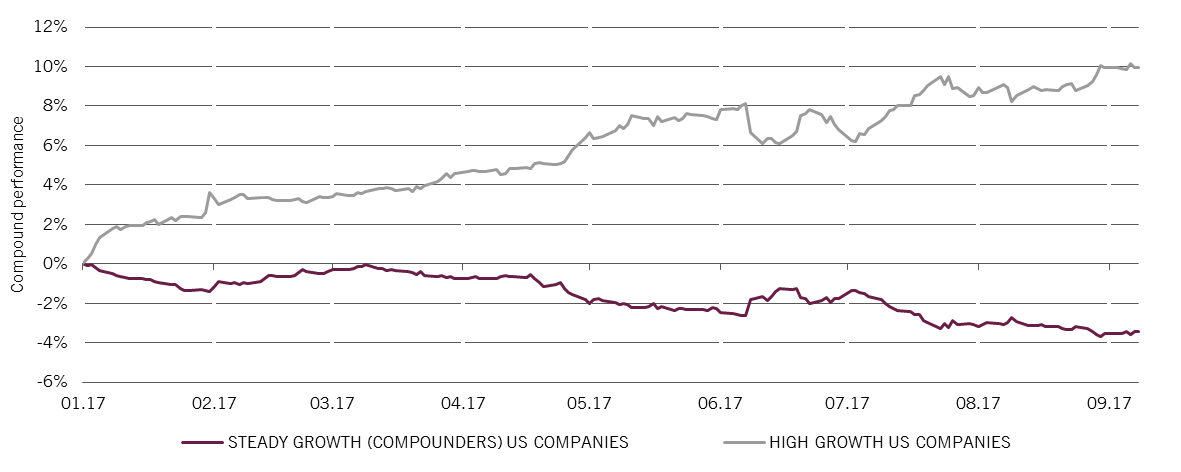

As Chart 2 shows, 'high growth' stocks have driven this year's equity rally, especially those in the technology space. Meanwhile, ‘steady growth (compounders)’ - what we call defensive stocks - have underperformed.

Chart 2: Relative performance of US steady growth vs. US high growth equities

2017 YTD

Source: MSCI World, Datastream, data as at 31.08.2017 and in USD. Equity indices quoted on the basis of net dividend reinvested.

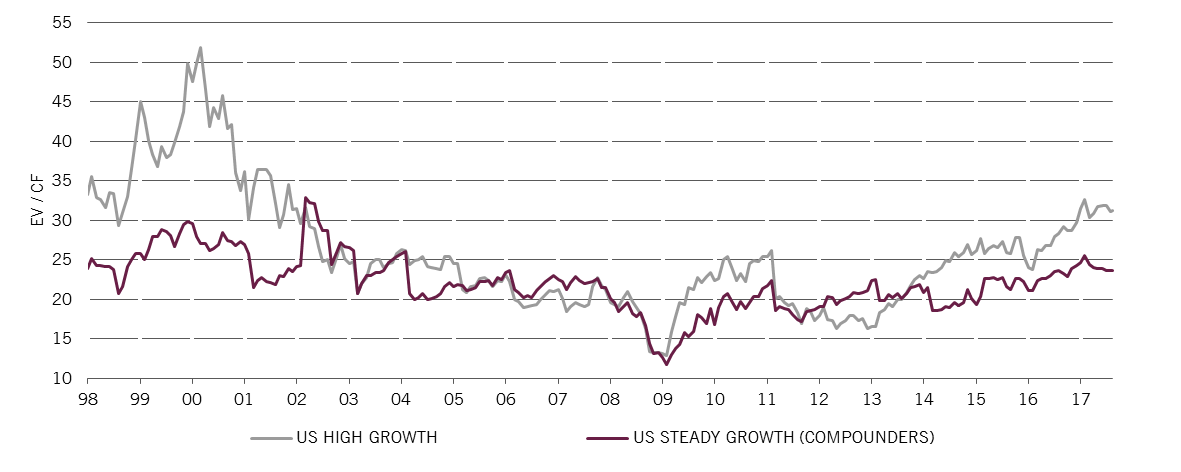

Steady growth stocks are therefore trading at a widening discount to high growth. Indeed, Chart 3 shows that using our favoured EV/CF valuation multiple they are at a discount to high growth stocks in the US market not seen since the build-up to the dot-com boom.

Chart 3: valuation multiples (EV/CF) of high growth stocks versus steady growth stocks in the us

1997 to 2017

Source: MSCI World, Datastream, data as at 31.08.2017 and in USD. Equity indices quoted on the basis of net dividend reinvested.

Note: we define ‘steady growth’ and ‘high growth’ companies as those ranking in the 4th and 1st quartile respectively for ‘investment growth’. We use 5 year investment growth of a company as it is a good proxy for anticipated future revenue growth.

Long-term, steady growth, defensive equities beat high growth

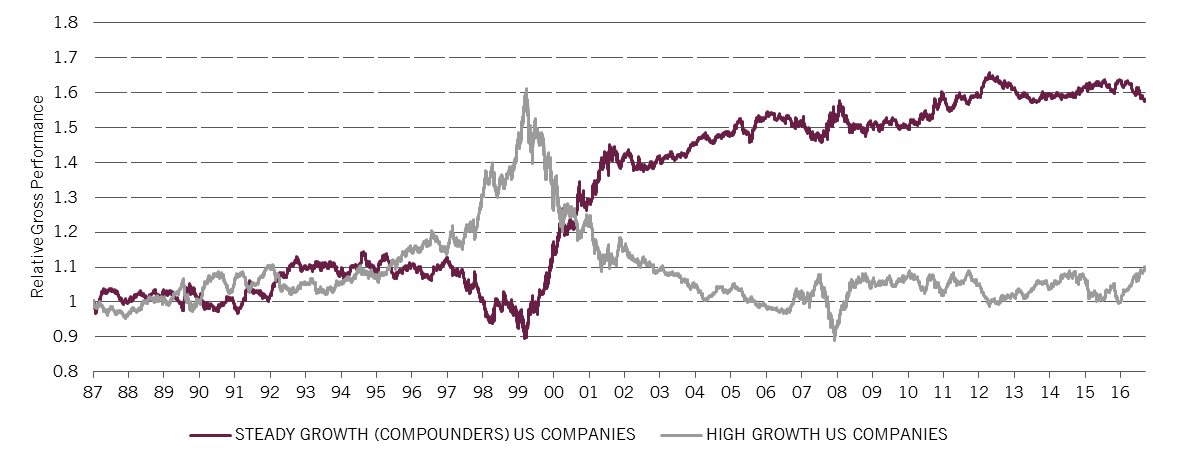

While the current environment is perhaps more favourable for growth strategies, long-term track records show such an environment tends to be rather short-lived. As chart 4 shows, over the longer term it is the less glamourous, lower growth, defensive US stocks that have outperformed. A similar, actually more emphatic, trend is observable within global equities over this same period. This is because, more often than not, growth stories do not translate into sustainable shareholder returns.

CHART 4: long-term performance of high growth veRSUS STEADY growth US stocks

1987-2017 YTD

Source: MSCI World, Datastream, data as at 31.08.2017 and in USD. Equity indices quoted on the basis of net dividend reinvested.

We think this calls for great caution when investing in growth stocks, especially when valuations are not supportive.

Although the aggregate market is very expensive, we continue to find interesting opportunities in defensive steady-growth stocks in our portfolios. As stated above, these have the advantage of being less expensive and we believe should outperform over the long term.

To find out more about how we manage the Pictet Global Defensive Equities strategy, read below or get in touch with your Pictet salesperson.

Reda Jürg Messikh joined Pictet Asset Management in 2007 and is Head of Quest Investments.

Reda was previously Senior Investment Manager/Head of Quantitative Research. Prior to that, he was Deputy Head of Risk Control in the Product and Risk Management team until 2011.

Before joining Pictet, he was a researcher at the Swiss Federal Institute of Technology (EPFL) in Lausanne and at EURANDOM in Eindhoven, the Netherlands.

Reda Jürg graduated with an Engineering degree in Physics from EPFL. He also holds a PhD in Mathematics and a MSc in Stochastic Modelling from the University of Paris (Orsay).

Share this article

Important legal information

This marketing material is issued by Pictet Asset Management (Europe) S.A.. It is neither directed to, nor intended for distribution or use by, any person or entity who is a citizen or resident of, or domiciled or located in, any locality, state, country or jurisdiction where such distribution, publication, availability or use would be contrary to law or regulation. The latest version of the fund‘s prospectus, Pre-Contractual Template (PCT) when applicable, Key Information Document (KID), annual and semi-annual reports must be read before investing. They are available free of charge in English on www.assetmanagement.pictet or in paper copy at Pictet Asset Management (Europe) S.A., 6B, rue du Fort Niedergruenewald, L-2226 Luxembourg, or at the office of the fund local agent, distributor or centralizing agent if any.

The KID is also available in the local language of each country where the compartment is registered. The prospectus, the PCT when applicable, and the annual and semi-annual reports may also be available in other languages, please refer to the website for other available languages. Only the latest version of these documents may be relied upon as the basis for investment decisions.

The summary of investor rights (in English and in the different languages of our website) is available here and at www.assetmanagement.pictet under the heading "Resources", at the bottom of the page.

The list of countries where the fund is registered can be obtained at all times from Pictet Asset Management (Europe) S.A., which may decide to terminate the arrangements made for the marketing of the fund or compartments of the fund in any given country.

The information and data presented in this document are not to be considered as an offer or solicitation to buy, sell or subscribe to any securities or financial instruments or services.

Information, opinions and estimates contained in this document reflect a judgment at the original date of publication and are subject to change without notice. The management company has not taken any steps to ensure that the securities referred to in this document are suitable for any particular investor and this document is not to be relied upon in substitution for the exercise of independent judgment. Tax treatment depends on the individual circumstances of each investor and may be subject to change in the future. Before making any investment decision, investors are recommended to ascertain if this investment is suitable for them in light of their financial knowledge and experience, investment goals and financial situation, or to obtain specific advice from an industry professional.

The value and income of any of the securities or financial instruments mentioned in this document may fall as well as rise and, as a consequence, investors may receive back less than originally invested.

The investment guidelines are internal guidelines which are subject to change at any time and without any notice within the limits of the fund's prospectus.

The mentioned financial instruments are provided for illustrative purposes only and shall not be considered as a direct offering, investment recommendation or investment advice. Reference to a specific security is not a recommendation to buy or sell that security. Effective allocations are subject to change and may have changed since the date of the marketing material.

Past performance is not a guarantee or a reliable indicator of future performance. Performance data does not include the commissions and fees charged at the time of subscribing for or redeeming shares.

Any index data referenced herein remains the property of the Data Vendor. Data Vendor Disclaimers are available on assetmanagement.pictet in the “Resources” section of the footer.

This document is a marketing communication issued by Pictet Asset Management and is not in scope for any MiFID II/MiFIR requirements specifically related to investment research. This material does not contain sufficient information to support an investment decision and it should not be relied upon by you in evaluating the merits of investing in any products or services offered or distributed by Pictet Asset Management.

Pictet AM has not acquired any rights or license to reproduce the trademarks, logos or images set out in this document except that it holds the rights to use any entity of the Pictet group trademarks. For illustrative purposes only.

Cookie Policy

This website uses cookies to enhance user navigation and to collect statistical data. To refuse the use of cookies, change your settings or for more information, please click on the following link: Cookies policy. By continuing to browse this website, you accept the use of cookies for the above purposes.