Revisiting the case for buying Turkish equities after the 2018 market rout.

Written by

Christopher Bannon

Senior Investment Manager

Share this article

Turkish assets were battered this year, leaving them with exceptionally cheap valuations. Companies with battered valuations are often well placed to rebound sharply. And history shows that badly dented markets returning to the mean is a powerful source of investment returns. But low prices do not necessarily imply high value. During such market conditions, we often align our thinking to one of the axioms of value investing guru Howard Marks: The most important thing – above all else – is the relationship between price and value. This phrase captures what we are concerned with very accurately, and today, when looking at the Turkish market, we ask ourselves: what value is in the price?

Turkey’s woes came from a number of directions – excess debt, an overheating economy, rising inflation, war on its borders and, not least, President Erdogan’s authoritarianism, which left investors questioning the independence of the country’s key institutions: the legal system; the central bank; and the press.

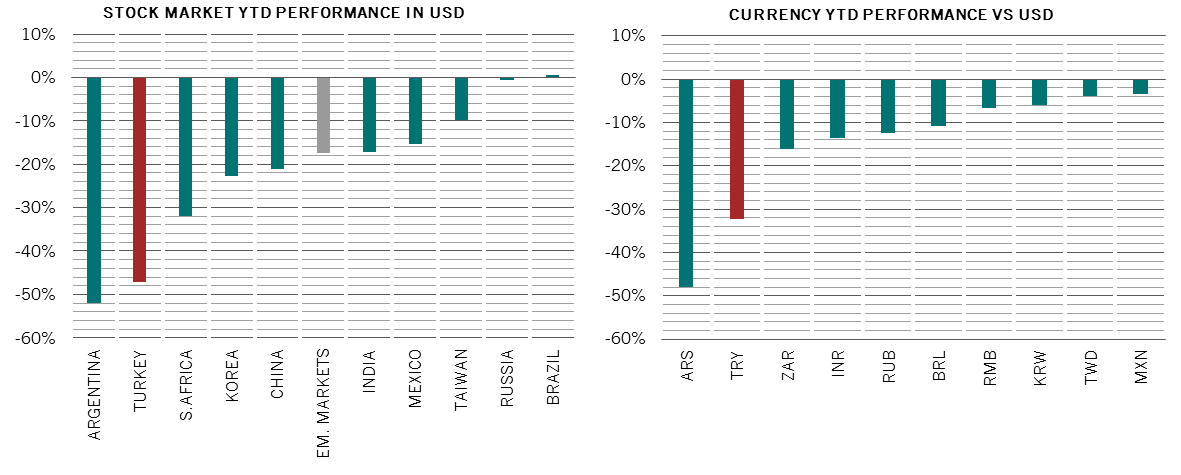

Of emerging market economies, only Argentina’s currency and asset markets have done worse year to date.

Fig.1 - TURKEY - Firmly on the podium of Emerging market underperformers

Year-to-date the Turkish stock market and lira have fallen by 47% and 32% respectively, to 31 October 2018

Pictet Asset Management, Factset, data as at 31st October 2018

So what should we make of this market extreme?

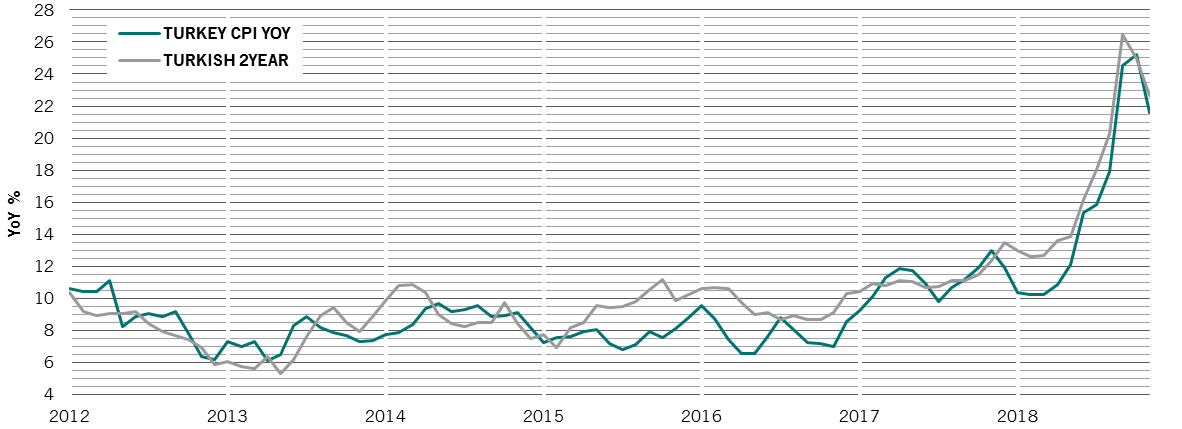

Turkish authorities are trying to undo some of the damage they caused. Fiscal stimulus and an ever widening current account deficit pushed the envelope too much last year with the central bank ultimately found wanting when tested. It took bond yields to blow out to some 30 per cent and the currency to collapse for the central bank to stop the rot.

But when it finally acted, it did so decisively, hiking rates 625bps. Along the way, it recovered some much needed credibility. The currency has since stabilised, while bond yields have retreated somewhat.

Fig.2 - Decisive action from the turkish central bank has had an impact

Turkish CPI (Year on Year changes) and benchmark 2 year government bond yields.

Pictet Asset Management, Factset, data as at 31st October 2018

As a consequence of the policies, we think it’s likely that Turkey will slip into recession over the next twelve months. This should bring the country’s current account back under control – the deficit has already shrunk sharply. Assuming that both the finance ministry and central bank stick to prudent economic management, and that the banking system avoids any contagious large scale deterioration in asset quality, it seems possible that Turkey will avoid having to impose extensive capital controls to stem further capital flight.

The key question is at which point the market starts to recognise value in Turkish assets.

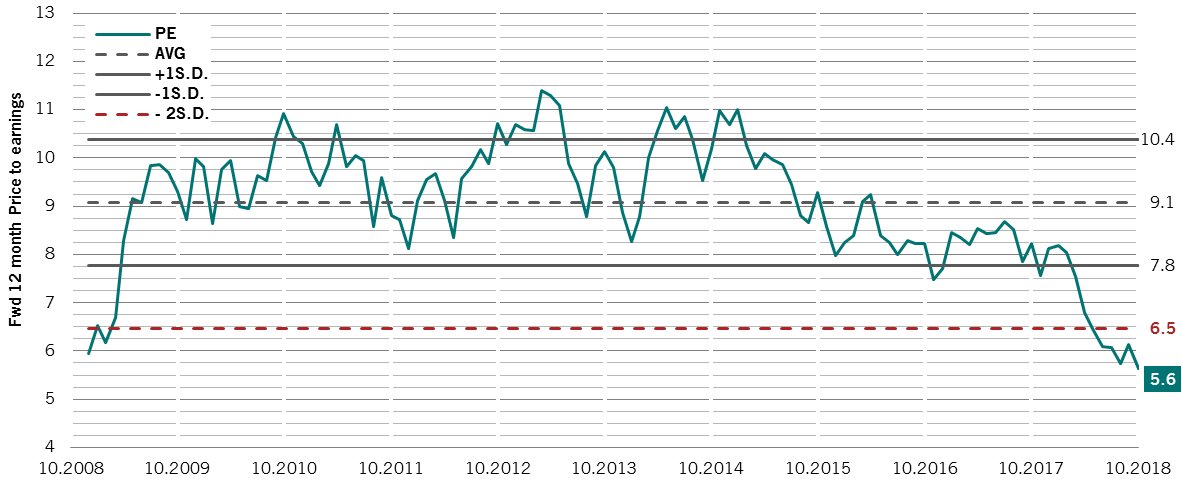

Using history as a guide, we think that’s unlikely until next year – the time to buy following previous Turkish crises has been in the first quarter of negative GDP growth. At present, Turkish equity market valuations are historically cheap at around 5.6 times price to earnings compared with a 10 year historic average of around 9.1 times. We think historic patterns will repeat – that Turkish valuations will return to historic trend, which is why we’ve started to increase our holdings of Turkish equities on a tactical basis.

Fig.3 - Turkish equity markets as cheap as they have been in ten years

Price to earnings ratio, forward twelve months, for the MSCI Turkey Index

Pictet Asset Management, Factset, data as at 31st October 2018Clearly, any investment that has the potential to undergo a severe inflationary debt crisis and 50 per cent devaluation in 3 months merits close scrutiny. But as Howard Marks says, it is the price you pay for assets that determines their risk and ultimate success, not whether they are high quality. On today’s prices, we believe Turkey could represent a fantastic buying opportunity into 2019.

Christopher Bannon joined Pictet Asset Management in 2007 and is a Senior Investment Manager in the Emerging Markets Equities team, specialising in Emerging Europe and Russia.

Christopher joined Pictet in 2007, initially as a risk manager before moving across to the Emerging Equities Research team in 2011 specialising in the energy sector across global emerging markets. Christopher started his career in 2005 with Citigroup, where he spent 18 months on the corporate actions desk.

Christopher graduated from Trinity College Dublin with a BA (Hons) in Mathematics and Philosophy and he holds an MSc in Finance (graduated with Distinction) from Imperial College London. He is also a Chartered Financial Analyst (CFA) charterholder.

Share this article

Important legal information

This marketing material is issued by Pictet Asset Management (Europe) S.A.. It is neither directed to, nor intended for distribution or use by, any person or entity who is a citizen or resident of, or domiciled or located in, any locality, state, country or jurisdiction where such distribution, publication, availability or use would be contrary to law or regulation. The latest version of the fund‘s prospectus, Pre-Contractual Template (PCT) when applicable, Key Information Document (KID), annual and semi-annual reports must be read before investing. They are available free of charge in English on www.assetmanagement.pictet or in paper copy at Pictet Asset Management (Europe) S.A., 6B, rue du Fort Niedergruenewald, L-2226 Luxembourg, or at the office of the fund local agent, distributor or centralizing agent if any.

The KID is also available in the local language of each country where the compartment is registered. The prospectus, the PCT when applicable, and the annual and semi-annual reports may also be available in other languages, please refer to the website for other available languages. Only the latest version of these documents may be relied upon as the basis for investment decisions.

The summary of investor rights (in English and in the different languages of our website) is available here and at www.assetmanagement.pictet under the heading "Resources", at the bottom of the page.

The list of countries where the fund is registered can be obtained at all times from Pictet Asset Management (Europe) S.A., which may decide to terminate the arrangements made for the marketing of the fund or compartments of the fund in any given country.

The information and data presented in this document are not to be considered as an offer or solicitation to buy, sell or subscribe to any securities or financial instruments or services.

Information, opinions and estimates contained in this document reflect a judgment at the original date of publication and are subject to change without notice. The management company has not taken any steps to ensure that the securities referred to in this document are suitable for any particular investor and this document is not to be relied upon in substitution for the exercise of independent judgment. Tax treatment depends on the individual circumstances of each investor and may be subject to change in the future. Before making any investment decision, investors are recommended to ascertain if this investment is suitable for them in light of their financial knowledge and experience, investment goals and financial situation, or to obtain specific advice from an industry professional.

The value and income of any of the securities or financial instruments mentioned in this document may fall as well as rise and, as a consequence, investors may receive back less than originally invested.

The investment guidelines are internal guidelines which are subject to change at any time and without any notice within the limits of the fund's prospectus.

The mentioned financial instruments are provided for illustrative purposes only and shall not be considered as a direct offering, investment recommendation or investment advice. Reference to a specific security is not a recommendation to buy or sell that security. Effective allocations are subject to change and may have changed since the date of the marketing material.

Past performance is not a guarantee or a reliable indicator of future performance. Performance data does not include the commissions and fees charged at the time of subscribing for or redeeming shares.

Any index data referenced herein remains the property of the Data Vendor. Data Vendor Disclaimers are available on assetmanagement.pictet in the “Resources” section of the footer.

This document is a marketing communication issued by Pictet Asset Management and is not in scope for any MiFID II/MiFIR requirements specifically related to investment research. This material does not contain sufficient information to support an investment decision and it should not be relied upon by you in evaluating the merits of investing in any products or services offered or distributed by Pictet Asset Management.

Pictet AM has not acquired any rights or license to reproduce the trademarks, logos or images set out in this document except that it holds the rights to use any entity of the Pictet group trademarks. For illustrative purposes only.

Cookie Policy

This website uses cookies to enhance user navigation and to collect statistical data. To refuse the use of cookies, change your settings or for more information, please click on the following link: Cookies policy. By continuing to browse this website, you accept the use of cookies for the above purposes.