The Chinese investible universe continues to grow and evolve offering an exciting dynamic for fundamental investors in the region.

Written by

James Kenney

Senior Investment Manager

Share this article

Only 5 years ago, Chinese corporate unicorns were as rare as… magical horses with single horns. But by the second quarter this year, there were over 160 of these Chinese Unicorns – as private companies worth more than USD1 billion have come to be known – with total value at over USD700 billion. By number of companies, that’s more than there are in the US. So we recently took a trip to China to have a closer look at this exotic corner of the market. We will delve deeper into the details in a later post, but here are a couple of things that really stood out.

CHinese unicorns - on par with the US

By number of companies, Chinese unicorns have outgrown US counterparts

Morgan Stanley, Pictet Asset Management, August 2018

Chinese companies becoming more global

I’ve been on many investment trips to China, but this was the first where I haven’t needed a translator for a single meeting – and I met with the management teams of 14 unlisted companies, whose cumulative valuation was close to USD400 billion. Increasingly, senior managers have been educated at business schools in the US and Europe. If nothing else, this should help foreign investors’ perceptions of investing in Chinese companies.

Most of the companies we met consider the

entire world as their ultimate market.

It is also giving corporate China an ever more global perspective. Most of the senior executives we met talked not only of expansion within China, but also considered the entire world as their ultimate market.

Unicorns are rapidly expanding the investible universe

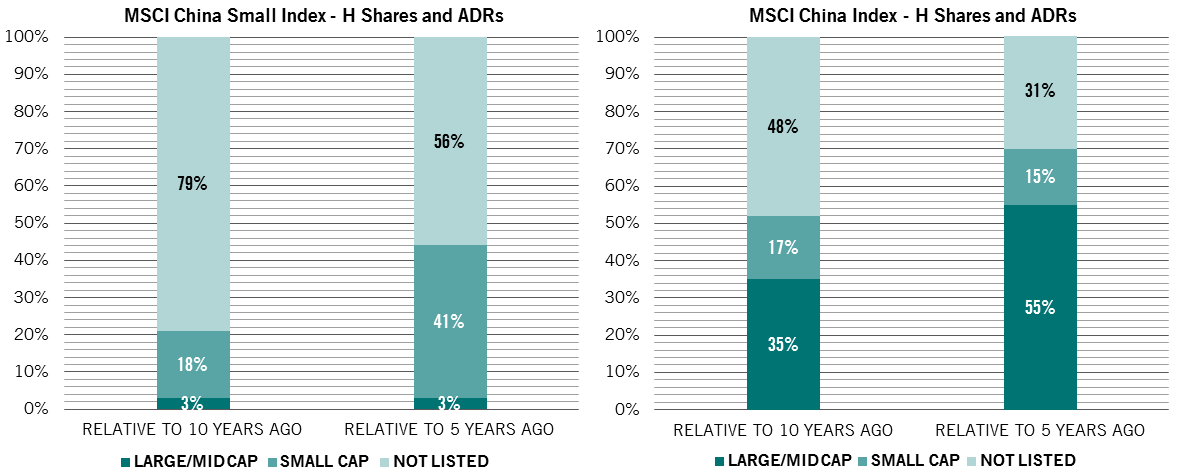

Not only is the profusion of Chinese Unicorns eye catching, but so too is the pace at which they’re listing – a key point for us as investors. If we consider the current universe of H-shares and ADRs within the MSCI China index, only 52 percent were listed 10 years ago. For the MSCI China Small Cap index, this figure is considerably smaller, with only 21 percent being listed 10 years ago. These trends can be seen below; the charts categorize the current constituents of the mentioned indices by their respective market caps 5 and 10 years ago.

The Chinese investment landscape continues to expand

MSCI China constituents ranked by their historic market caps.

Source: Morgan Stanley, Pictet Asset Management, August 2018

With China relaxing the rules for listing companies both in Hong Kong and in the domestic A-share market, we expect ever more of these Unicorns to come to market. Indeed, in 2018 alone, Xiaomi (hardware and online services, USD50 billion market cap), CATL (battery producer, USD25 billion market cap), iQiyi (online video, USD20 billion market cap), Huya (game live broadcasting, USD6 billion market cap), and PingDuoDuo (e-commerce, USD 25 billion market cap) have all listed.

Meanwhile, Tencent Music and Meituan both recently filed for IPO. We anticipate Ant Financial will list in 2019 which, based on current market valuations, would be the largest Unicorn in the world valued well in excess of USD 100 billion.

Chinese unicorns are different

One common denominator in a lot of the internet-related Unicorns is that they are typically owned by one of the BAT (Baidu, Alibaba, Tencent). This provides a structural advantage few American based IPOs can count on – an advantage central to why we believe the returns and the cash generation of these Chinese companies can be superior to their developed-market counterparts.

The largest cost item for an internet company is the process of acquiring and engaging users. Many of these Chinese Unicorns are born into massive accessible markets. The BAT owns large gateways to the internet, through a huge collective user-base. Baidu is China’s largest search engine with 70 percent market share. Alibaba is the largest online retail company with over 550 million active consumers. Tencent owns the largest social networking mobile application in China, WeChat, with over 900 million monthly active users (MAUs). Access to any of these gateways reduces customer acquisition costs drastically through various mechanisms and increases the addressable market from day one. This is a luxury which few American based IPOs can exploit.

About

James Kenney

James Kenney joined Pictet Asset Management in 2010. He is the Lead Portfolio Manager on the China Equity Strategy and Co-Lead Portfolio Manager on the Asian Equities ex Japan strategy.

Before joining the Emerging Equities team in 2011, James completed a one year rotation within the firm. Previously he was with F&C Asset Management for a year as a performance analyst.

James holds a degree in Chemistry from the University of Oxford as well as the Investment Management Certificate. James is also a Chartered Financial Analyst (CFA) Charterholder.

Read more trip notes from our emerging equity team

This marketing material is issued by Pictet Asset Management (Europe) S.A.. It is neither directed to, nor intended for distribution or use by, any person or entity who is a citizen or resident of, or domiciled or located in, any locality, state, country or jurisdiction where such distribution, publication, availability or use would be contrary to law or regulation. The latest version of the fund‘s prospectus, Pre-Contractual Template (PCT) when applicable, Key Information Document (KID), annual and semi-annual reports must be read before investing. They are available free of charge in English on www.assetmanagement.pictet or in paper copy at Pictet Asset Management (Europe) S.A., 6B, rue du Fort Niedergruenewald, L-2226 Luxembourg, or at the office of the fund local agent, distributor or centralizing agent if any.

The KID is also available in the local language of each country where the compartment is registered. The prospectus, the PCT when applicable, and the annual and semi-annual reports may also be available in other languages, please refer to the website for other available languages. Only the latest version of these documents may be relied upon as the basis for investment decisions.

The summary of investor rights (in English and in the different languages of our website) is available here and at www.assetmanagement.pictet under the heading "Resources", at the bottom of the page.

The list of countries where the fund is registered can be obtained at all times from Pictet Asset Management (Europe) S.A., which may decide to terminate the arrangements made for the marketing of the fund or compartments of the fund in any given country.

The information and data presented in this document are not to be considered as an offer or solicitation to buy, sell or subscribe to any securities or financial instruments or services.

Information, opinions and estimates contained in this document reflect a judgment at the original date of publication and are subject to change without notice. The management company has not taken any steps to ensure that the securities referred to in this document are suitable for any particular investor and this document is not to be relied upon in substitution for the exercise of independent judgment. Tax treatment depends on the individual circumstances of each investor and may be subject to change in the future. Before making any investment decision, investors are recommended to ascertain if this investment is suitable for them in light of their financial knowledge and experience, investment goals and financial situation, or to obtain specific advice from an industry professional.

The value and income of any of the securities or financial instruments mentioned in this document may fall as well as rise and, as a consequence, investors may receive back less than originally invested.

The investment guidelines are internal guidelines which are subject to change at any time and without any notice within the limits of the fund's prospectus.

The mentioned financial instruments are provided for illustrative purposes only and shall not be considered as a direct offering, investment recommendation or investment advice. Reference to a specific security is not a recommendation to buy or sell that security. Effective allocations are subject to change and may have changed since the date of the marketing material.

Past performance is not a guarantee or a reliable indicator of future performance. Performance data does not include the commissions and fees charged at the time of subscribing for or redeeming shares.

Any index data referenced herein remains the property of the Data Vendor. Data Vendor Disclaimers are available on assetmanagement.pictet in the “Resources” section of the footer.

This document is a marketing communication issued by Pictet Asset Management and is not in scope for any MiFID II/MiFIR requirements specifically related to investment research. This material does not contain sufficient information to support an investment decision and it should not be relied upon by you in evaluating the merits of investing in any products or services offered or distributed by Pictet Asset Management.

Pictet AM has not acquired any rights or license to reproduce the trademarks, logos or images set out in this document except that it holds the rights to use any entity of the Pictet group trademarks. For illustrative purposes only.

Cookie Policy

This website uses cookies to enhance user navigation and to collect statistical data. To refuse the use of cookies, change your settings or for more information, please click on the following link: Cookies policy. By continuing to browse this website, you accept the use of cookies for the above purposes.