Post-pandemic cities

Coronavirus will change the shape of our cities, but the tide of urbanisation is unstoppable.

Written by

Zsolt Kohalmi

Deputy CEO & Global Head of Real Estate

Past pandemics and diseases have played a key role in influencing the cities of today. The minimalist white walls and floor-to-ceiling windows beloved in modern buildings were originally inspired by the tuberculosis sanatoria of the early 20th century. The iconic boulevards of Paris and New York’s sprawling Central Park, meanwhile, were designed to help control the spread of cholera and other illnesses in the 19th century.

Yet, crucially, the concept of the city itself has continued to survive and flourish. Today, cities account for around 80 per cent of the world’s gross domestic product (GDP), and that share is likely to continue to grow. But the Covid-19 outbreak will transform how we build them, as well as how we work and live in them. In the spirit of never letting a recession go to waste, we must look to seize this opportunity to fix the problems that have long plagued the urban environment.

With interest rates and bond yields around the world very low or negative, real estate will continue to attract strong inflows from investors looking for a positive real return. But to achieve that, it is important to tune into the changes that will sweep across our cities.

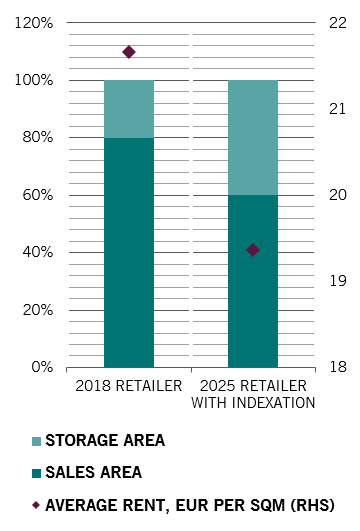

Take retailing. After the pandemic, there will be fewer traditional shops. Bricks and mortar retail was already struggling, with around one in 10 shops standing empty. Now, due to lockdowns, footfall in UK shops dropped 85 per cent year-on-year in April, while online sales spiked by 58 per cent to reach a record high of 70 per cent of all non-food sales. While some of that is temporary, the broad trend has greatly been accelerated by the pandemic. The retailers that survive the digital shakeout will be the ones that are in popular locations and offer experiences and leisure activities. As more space is used for storage and logistics for online sales, rental values will be under pressure (see chart).

Changing shops

Theoretical impact of rising e-commerce on monthly rents in retail sector

City offices threaten to be another casualty of Covid-19. With millions of people across the world having experienced home working, there are fears that office life might be consigned to history. However, the situation is more complex. Undoubtedly, working practices will become more flexible, but we believe that offices have a future, even if not all of us go there every working day. Humans are social animals: we need shared space to co-create, innovate and collaborate. This is particularly true today, when many manual and routine jobs have been automated, changing the nature of what we do in offices – some 80 per cent of work today is defined as “collaborative”.

Of course, some businesses will fold and others – particularly small ones – may decide they can do without having an office. Older buildings in out-of-town locations are likely to struggle to attract tenants, and many may be converted into apartments. But, to balance that, there are businesses that are considering expanding office space to enable social distancing. The average space per employee has halved over the past two decades, and we may now see that trend reverse as spacious modern offices become a talent recruitment tool. (According to Knight Frank’s estimates, socially distanced offices would require 135 sqft per desk-based worker, compared to current averages of 126 sqft in the City of London and 104 sqft in the Docklands business district). There will be other changes too: doors that open without being touched, app-operated canteens, better lift systems, improved air circulation and innovative approaches to hot desking without compromising hygiene.

Real estate sectors dependent on travel will take a long time to recover. Hotels will likely embrace technology to reduce both costs and contact. Business locations may suffer more than leisure ones, and there could be an increased focus on meeting the preferences of domestic tourists. Student accommodation – very recently seen as a sure-fire route to steady income – may be in the doldrums for years as international students stay away and universities embrace online learning.

The residential sector will not be spared upheaval, either. As people become used to working from home, they will require a more professional work area. That implies a different design, including more space and light. In future apartment listings the number of workstations may become as important as the number of bedrooms. Co-living will probably remain popular, for financial reasons if nothing else, but with a greater focus on space and technology.

Suburban living will experience further growth. Families with young children, for example, may be even more interested in relocating to city outskirts and commuter towns, especially if more flexible working catches on and they no longer have to face the commute every day. At the same time, the shifts towards greener commuting – such as walking and cycling – will reduce the importance of public transport links. Electric bikes in particular can make a wide range of near-central locations more accessible and attractive.

Air quality – both inside and outside – will become a higher priority, both for residents and regulators. This is a big issue, as urban areas are responsible for 70 per cent of the world’s greenhouse gas emissions. In large cities, like London, people will check air quality on their street when looking to buy homes or even choosing potential office locations.

Among the possible winners in the post-Covid world, data centres have emerged as the new darlings for investors, as have medical centres, sports facilities and other wellness establishments in the expectation that that society will emerge from this pandemic with a more health conscious attitude. Small, last mile logistics facilities should also do well as shopping is increasingly done online.

Whichever sector you look at, there will be change. As 70 per cent of all buildings in Europe are over 20 years old, this change will require a lot of work. Investors will have to be particularly nimble in adapting to changing needs and expectations of building users, embracing the opportunity to shape the cities of tomorrow.

Important legal information

This marketing material is issued by Pictet Asset Management (Europe) S.A.. It is neither directed to, nor intended for distribution or use by, any person or entity who is a citizen or resident of, or domiciled or located in, any locality, state, country or jurisdiction where such distribution, publication, availability or use would be contrary to law or regulation. The latest version of the fund‘s prospectus, Pre-Contractual Template (PCT) when applicable, Key Information Document (KID), annual and semi-annual reports must be read before investing. They are available free of charge in English on www.assetmanagement.pictet or in paper copy at Pictet Asset Management (Europe) S.A., 6B, rue du Fort Niedergruenewald, L-2226 Luxembourg, or at the office of the fund local agent, distributor or centralizing agent if any.

The KID is also available in the local language of each country where the compartment is registered. The prospectus, the PCT when applicable, and the annual and semi-annual reports may also be available in other languages, please refer to the website for other available languages. Only the latest version of these documents may be relied upon as the basis for investment decisions.

The summary of investor rights (in English and in the different languages of our website) is available here and at www.assetmanagement.pictet under the heading "Resources", at the bottom of the page.

The list of countries where the fund is registered can be obtained at all times from Pictet Asset Management (Europe) S.A., which may decide to terminate the arrangements made for the marketing of the fund or compartments of the fund in any given country.

The information and data presented in this document are not to be considered as an offer or solicitation to buy, sell or subscribe to any securities or financial instruments or services.

Information, opinions and estimates contained in this document reflect a judgment at the original date of publication and are subject to change without notice. The management company has not taken any steps to ensure that the securities referred to in this document are suitable for any particular investor and this document is not to be relied upon in substitution for the exercise of independent judgment. Tax treatment depends on the individual circumstances of each investor and may be subject to change in the future. Before making any investment decision, investors are recommended to ascertain if this investment is suitable for them in light of their financial knowledge and experience, investment goals and financial situation, or to obtain specific advice from an industry professional.

The value and income of any of the securities or financial instruments mentioned in this document may fall as well as rise and, as a consequence, investors may receive back less than originally invested.

The investment guidelines are internal guidelines which are subject to change at any time and without any notice within the limits of the fund's prospectus. The mentioned financial instruments are provided for illustrative purposes only and shall not be considered as a direct offering, investment recommendation or investment advice. Reference to a specific security is not a recommendation to buy or sell that security. Effective allocations are subject to change and may have changed since the date of the marketing material.

Past performance is not a guarantee or a reliable indicator of future performance. Performance data does not include the commissions and fees charged at the time of subscribing for or redeeming shares.

Any index data referenced herein remains the property of the Data Vendor. Data Vendor Disclaimers are available on assetmanagement.pictet in the “Resources” section of the footer. This document is a marketing communication issued by Pictet Asset Management and is not in scope for any MiFID II/MiFIR requirements specifically related to investment research. This material does not contain sufficient information to support an investment decision and it should not be relied upon by you in evaluating the merits of investing in any products or services offered or distributed by Pictet Asset Management.

Pictet AM has not acquired any rights or license to reproduce the trademarks, logos or images set out in this document except that it holds the rights to use any entity of the Pictet group trademarks. For illustrative purposes only.