Premium brands welcome China's revival

China's luxury goods market is set to benefit from considerable pent-up demand as the country emerges from its Covid lockdowns.

Written by

Pictet Thematic Advisory Board

Beijing’s decision to drop its draconian zero-Covid policy and instead push for growth is a boon for luxury goods producers. Although they’ve weathered China’s recent turmoil reasonably well, the government’s policy shift is bound to release pent-up demand.

The top end of the Chinese luxury market has been resilient throughout, but even where demand has been dented within China, wealthy Chinese have continued to buy such goods abroad, which has helped many brands to sustain global sales. At the same time, Chinese consumers are starting to take an interest in niche sporting and educational products and services – from kayaking to painting lessons – while also increasingly shifting their focus to domestic premium brands, according to Pictet’s Premium Brands Advisory Board. Leading premium brands producers still expect China to be the world’s top luxury market by 2025.1

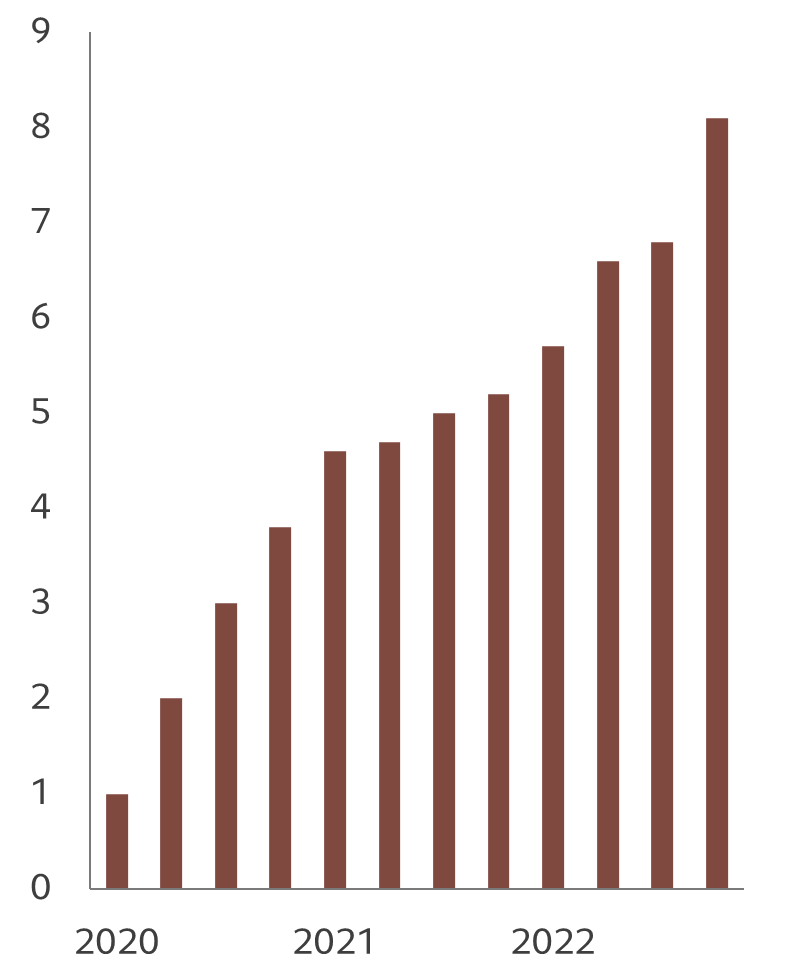

Fig. 1 - Firepower

Chinese excess savings as % of disposable income*

To be sure, the near-term remains a challenge: a combination of inhospitable politics, residual economic headwinds and a shift in consumer tastes are all hurdles for luxury goods producers, warns the advisory board. So while the Chinese personal goods market saw 36 per cent growth in 2021 over the previous year,2 2022 was distinctly less favourable.

The recent Communist Party Congress reinforced President Xi Jinping push to increase state control, which threatens to further undermine China’s dynamic private sector. At the same time, Xi’s zero-Covid policy had a major impact on the economy, with up to half of the country’s regions affected, leaving travel – both internal and foreign – heavily curtailed. Demand was further depressed by the property crisis – real estate represents some 70 per cent of household assets in China. Official crackdowns on some industries, like private education and internet commerce, has also had significant effects, forcing large firms to cut jobs. More generally, youth unemployment has risen to 20 per cent.

Releasing pent-up demand

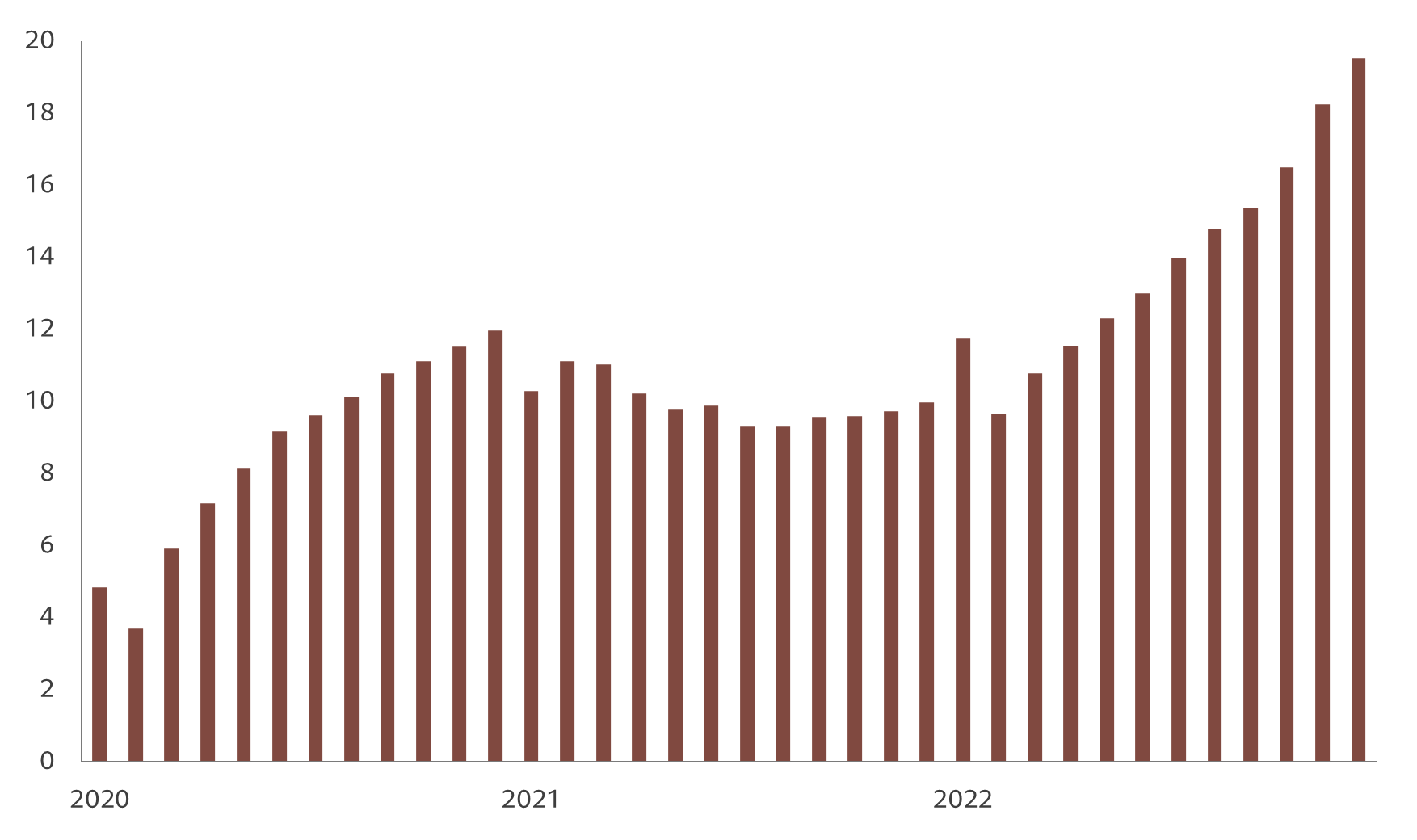

But with the government dropping its zero Covid policy and introducing measures to support the country’s struggling property market, China is poised to boom over the coming year – Pictet Asset Management’s strategists expect China to outperform developed economies during the coming year. Our economists estimate that, by the end of 2022, Chinese cumulative excess savings accounted for some 8.1 per cent of disposable income and household excess savings nearly 20 per cent of GDP (see Figs. 1 and 2).

This should help support Chinese retail consumption and, with it, spending on luxury goods. Forecasters still expect China to become the world’s biggest market for luxury goods by 2025. Mere moderation of the zero-Covid policy or signs that the pandemic is no longer a health crisis could release some pent-up demand, potentially boosting global turnover in the sector by 10 per cent. Chinese luxury brands rooted in local culture, such as traditional medicine and craftsmanship will be in particular demand and are likely to be supported by Beijing.3

Fig. 2 - Dry powder

Chinese household excess deposits, % of GDP*

More generally, there seems to be a change in consumption patterns among Chinese consumers. Demand appears to be shifting from conspicuous luxury goods to high quality experiences. Rather than buying yet another luxury handbag or watch, the most affluent consumers are investing in education, healthcare, refined hobbies like painting or playing musical instruments, or in elite sports. And the government has been encouraging its citizens to take up a wider variety of sports, which has already started to benefit specialist brands. Yoga has been particularly popular.

Overall, the glass remains half full for luxury goods companies selling into the Chinese market. A few of the very high-end brands even managed to generate growth in sales during the difficult conditions of the third quarter of 2022. Chinese appetite for luxuries will endure. Even though the across-the-board boom of the past decade seems unlikely to be repeated, the picture remains brighter for top brands and niche suppliers of both goods and services.

related articles

Economic bumps shouldn't derail the recovery in global travel.

The travel and tourism industry has struggled with Covid, but they're reviving as the impact of the pandemic fades.

February 2023

Why China's re-opening could be a blessing for emerging market bonds

The re-opening of the world's second largest economy shouldn't concern those worried about inflation.

February 2023

Important legal information

This marketing material is issued by Pictet Asset Management (Europe) S.A.. It is neither directed to, nor intended for distribution or use by, any person or entity who is a citizen or resident of, or domiciled or located in, any locality, state, country or jurisdiction where such distribution, publication, availability or use would be contrary to law or regulation. The latest version of the fund‘s prospectus, Pre-Contractual Template (PCT) when applicable, Key Information Document (KID), annual and semi-annual reports must be read before investing. They are available free of charge in English on www.assetmanagement.pictet or in paper copy at Pictet Asset Management (Europe) S.A., 6B, rue du Fort Niedergruenewald, L-2226 Luxembourg, or at the office of the fund local agent, distributor or centralizing agent if any.

The KID is also available in the local language of each country where the compartment is registered. The prospectus, the PCT when applicable, and the annual and semi-annual reports may also be available in other languages, please refer to the website for other available languages. Only the latest version of these documents may be relied upon as the basis for investment decisions.

The summary of investor rights (in English and in the different languages of our website) is available here and at www.assetmanagement.pictet under the heading "Resources", at the bottom of the page.

The list of countries where the fund is registered can be obtained at all times from Pictet Asset Management (Europe) S.A., which may decide to terminate the arrangements made for the marketing of the fund or compartments of the fund in any given country.

The information and data presented in this document are not to be considered as an offer or solicitation to buy, sell or subscribe to any securities or financial instruments or services.

Information, opinions and estimates contained in this document reflect a judgment at the original date of publication and are subject to change without notice. The management company has not taken any steps to ensure that the securities referred to in this document are suitable for any particular investor and this document is not to be relied upon in substitution for the exercise of independent judgment. Tax treatment depends on the individual circumstances of each investor and may be subject to change in the future. Before making any investment decision, investors are recommended to ascertain if this investment is suitable for them in light of their financial knowledge and experience, investment goals and financial situation, or to obtain specific advice from an industry professional.

The value and income of any of the securities or financial instruments mentioned in this document may fall as well as rise and, as a consequence, investors may receive back less than originally invested.

The investment guidelines are internal guidelines which are subject to change at any time and without any notice within the limits of the fund's prospectus. The mentioned financial instruments are provided for illustrative purposes only and shall not be considered as a direct offering, investment recommendation or investment advice. Reference to a specific security is not a recommendation to buy or sell that security. Effective allocations are subject to change and may have changed since the date of the marketing material.

Past performance is not a guarantee or a reliable indicator of future performance. Performance data does not include the commissions and fees charged at the time of subscribing for or redeeming shares.

Any index data referenced herein remains the property of the Data Vendor. Data Vendor Disclaimers are available on assetmanagement.pictet in the “Resources” section of the footer. This document is a marketing communication issued by Pictet Asset Management and is not in scope for any MiFID II/MiFIR requirements specifically related to investment research. This material does not contain sufficient information to support an investment decision and it should not be relied upon by you in evaluating the merits of investing in any products or services offered or distributed by Pictet Asset Management.

Pictet AM has not acquired any rights or license to reproduce the trademarks, logos or images set out in this document except that it holds the rights to use any entity of the Pictet group trademarks. For illustrative purposes only.