Secular outlook 2023

Securing single-digit annual returns from a diversified portfolio could prove an unusually complex task in the next five years, largely because of volatile inflation and more muscular state intervention.

Written by

Pictet Asset Management's Strategy Unit (PSU)

1. Overview: return projections for the next five years

Investment strategies will need an overhaul over the next five years. And for several reasons. Economic growth for the rest of this decade will remain stubbornly below average as inflation – while in retreat – is likely to be unusually volatile. Greater state intervention in the economy, meanwhile – in industries such as cleantech, semiconductors and defence – will not only add to the public debt burden but could also increase the risk of policy mistakes and capital misallocation.

The headwinds become more powerful still when the effects of weak productivity, labour shortages and tighter financial conditions begin to manifest themselves with greater intensity. Yet for nimble investors, and those prepared to venture beyond the beaten track of developed equity markets, several potentially rewarding opportunities remain.

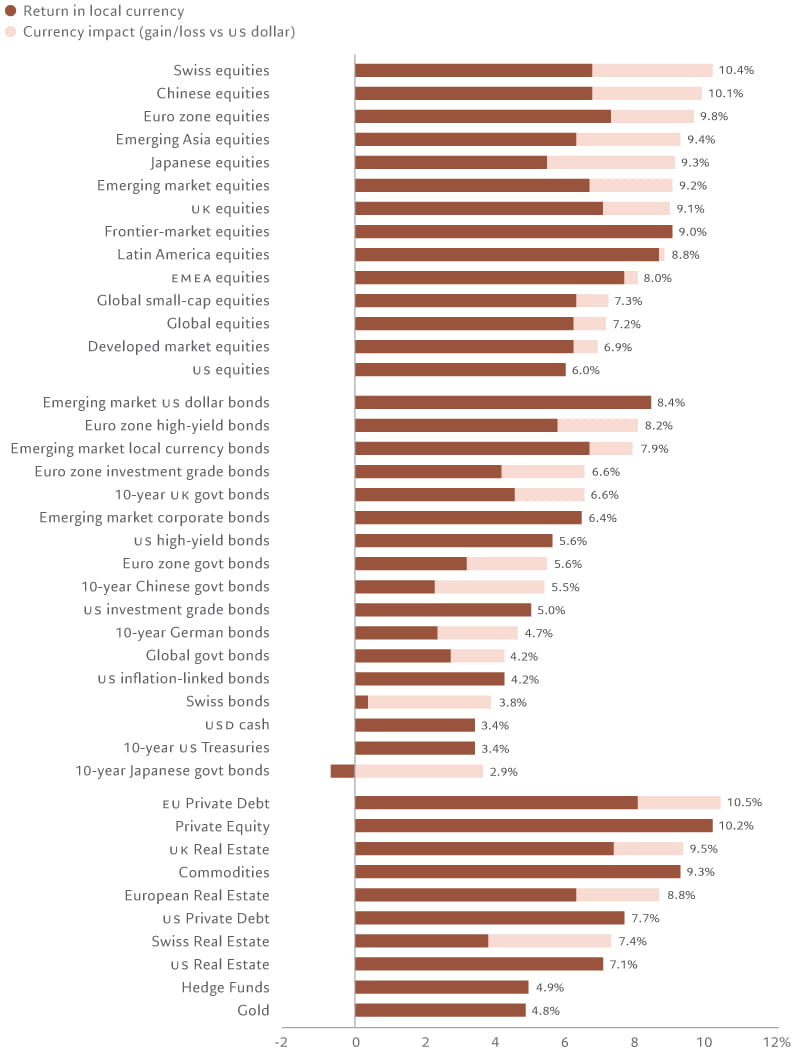

Figure 1 - Asset class returns, 5-year forecast, %, annualised

|

Opportunities

|

Threats

|

2. Secular trends

A more interventionist state

Stung by the experiences of the Covid pandemic and the Ukraine war, governments are prioritising domestic resilience and national defence.

The renewed geopolitical rivalry will reconfigure global commerce. Industries that attract the greatest amount of state subsidies – such as semiconductors, green technology, cybersecurity and defence – may well see an improvement in their fortunes.

Yet the broader picture is one of increased risks for investors. The likelihood of policy mistakes will increase as governments and regulators become involved in the management of their economies.

Since 2018, a balanced portfolio whose assets are split evenly between world stocks and US government bonds has delivered a real return of just

1%

per year annualised.

Source: This is the annualised return, in US dollars of a portfolio whose assets are split evenly between equities (MSCI World index) and bonds (JPMorgan US government bond index), covering period 30.04.18-30.04.2023, adjusted for US CPI.

Inflation will fall but it will also be more volatile

We expect inflation to drift back towards levels consistent with central bank targets over the next five years. But this will come with a cost: the rate of inflation will be considerably more volatile.

Returns on traditional portfolios will be lower. As a consequence, economies will grow at below their own long-term trend while returns from traditional balanced portfolios will also be lower than the historical average.

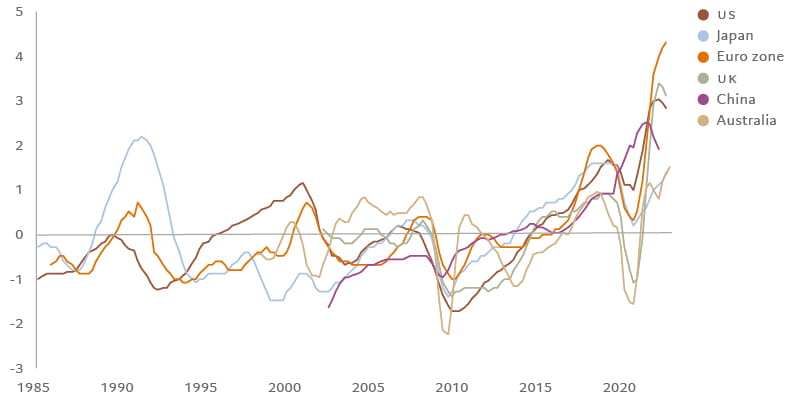

Brace for a labour shortage

An ageing population and the shift to flexible working are exacerbating labour shortages around the world. This is already lowering productivity and curtailing the world economy’s long-term growth potential. China’s shrinking population will make matters even worse.

The adoption of automation could become a more urgent priority.

Figure 2 - In short supply

Labour shortage indicators in selected economies

Avoiding a prolonged economic stagnation will mean making even greater use of automation and machine learning to boost productivity.

But a tech transition will be a long and complicated process.

Related articles

The rise of generative AI

Generative AI has the potential to change the way we live and work and could soon redraw the landscape for investors in technology stocks.

May 2023

Private assets' role in a diversified portfolio

Private assets are an increasingly important source of returns and diversification. Shaniel Ramjee, senior investment manager, Multi Asset, takes us through the opportunities private markets offer, as well as the risks they pose.

April 2023

The sweetspot in European direct lending

When it comes to European direct lending, we believe that small is beautiful. Here is why.

April 2023

Making steel sector more sustainable

A boutique Brazilian company is leading a ‘green steel’ revolution, changing an industry little-known for sustainability.

May 2023

Outlook for clean energy industry

Governments across the world have intensified efforts to secure an ever bigger slice of the environmental tech market.

May 2023

Important legal information

This marketing material is issued by Pictet Asset Management (Europe) S.A.. It is neither directed to, nor intended for distribution or use by, any person or entity who is a citizen or resident of, or domiciled or located in, any locality, state, country or jurisdiction where such distribution, publication, availability or use would be contrary to law or regulation. The latest version of the fund‘s prospectus, Pre-Contractual Template (PCT) when applicable, Key Information Document (KID), annual and semi-annual reports must be read before investing. They are available free of charge in English on www.assetmanagement.pictet or in paper copy at Pictet Asset Management (Europe) S.A., 6B, rue du Fort Niedergruenewald, L-2226 Luxembourg, or at the office of the fund local agent, distributor or centralizing agent if any.

The KID is also available in the local language of each country where the compartment is registered. The prospectus, the PCT when applicable, and the annual and semi-annual reports may also be available in other languages, please refer to the website for other available languages. Only the latest version of these documents may be relied upon as the basis for investment decisions.

The summary of investor rights (in English and in the different languages of our website) is available here and at www.assetmanagement.pictet under the heading "Resources", at the bottom of the page.

The list of countries where the fund is registered can be obtained at all times from Pictet Asset Management (Europe) S.A., which may decide to terminate the arrangements made for the marketing of the fund or compartments of the fund in any given country.

The information and data presented in this document are not to be considered as an offer or solicitation to buy, sell or subscribe to any securities or financial instruments or services.

Information, opinions and estimates contained in this document reflect a judgment at the original date of publication and are subject to change without notice. The management company has not taken any steps to ensure that the securities referred to in this document are suitable for any particular investor and this document is not to be relied upon in substitution for the exercise of independent judgment. Tax treatment depends on the individual circumstances of each investor and may be subject to change in the future. Before making any investment decision, investors are recommended to ascertain if this investment is suitable for them in light of their financial knowledge and experience, investment goals and financial situation, or to obtain specific advice from an industry professional.

The value and income of any of the securities or financial instruments mentioned in this document may fall as well as rise and, as a consequence, investors may receive back less than originally invested.

The investment guidelines are internal guidelines which are subject to change at any time and without any notice within the limits of the fund's prospectus. The mentioned financial instruments are provided for illustrative purposes only and shall not be considered as a direct offering, investment recommendation or investment advice. Reference to a specific security is not a recommendation to buy or sell that security. Effective allocations are subject to change and may have changed since the date of the marketing material.

Past performance is not a guarantee or a reliable indicator of future performance. Performance data does not include the commissions and fees charged at the time of subscribing for or redeeming shares.

Any index data referenced herein remains the property of the Data Vendor. Data Vendor Disclaimers are available on assetmanagement.pictet in the “Resources” section of the footer. This document is a marketing communication issued by Pictet Asset Management and is not in scope for any MiFID II/MiFIR requirements specifically related to investment research. This material does not contain sufficient information to support an investment decision and it should not be relied upon by you in evaluating the merits of investing in any products or services offered or distributed by Pictet Asset Management.

Pictet AM has not acquired any rights or license to reproduce the trademarks, logos or images set out in this document except that it holds the rights to use any entity of the Pictet group trademarks. For illustrative purposes only.