Investing in China's stocks: the long and the short of it

In this interview with Citywire, Pictet Asset Management senior investment manager Lan Wang Simond runs the rule over the Chinese equity market.

Written by

Lan Wang Simond

Senior Investment Manager

Last year was not a good one for investors in Chinese equities. With the economy slowing and global tensions rising, the market was rocked by severe bouts of volatility. Poor sentiment weighed more heavily on the market than long-held convictions about China’s structural growth. The most common onshore A-share and offshore H-share indices ended 2018 down 23.6 per cent and 11.7 per cent respectively.

2019 could see more of the same concerns, with investors fretting about geo-political and local issues at the same time. Volatility is likely to continue throughout the year, thinks Lan Wang Simond, head of and senior investment manager of the Greater China long-short team.

"Our view continues to be cautious. The markets will be tough for directional investors in long-only shares in China, Hong Kong, Taiwan and across the Asian region," she says. Apart from the US-China trade war and China’s slowing economic growth, topping her watch list includes the results season in March, which serves as a barometer of corporate health and valuations.

“With volatility looking here to stay, we prefer to look past the market noise and express our convictions through relative value positions based on our bottom up research," she explains.

She is keen to stress that there are still many good companies with strong prospects in Greater China. In calmer conditions, their stock prices should pull ahead and generate solid returns for long-only investors. Bottom-up stock pickers would not struggle to fill their portfolios if conviction were enough to secure positive gains in 2019, but selectivity will be key. A case in point: The team has taken a long position in a pharmaceutical company that was shunned by investors for its low pricing power over one drug but underestimated the potential of its product pipeline. This contrarian move has been profitable thus far.

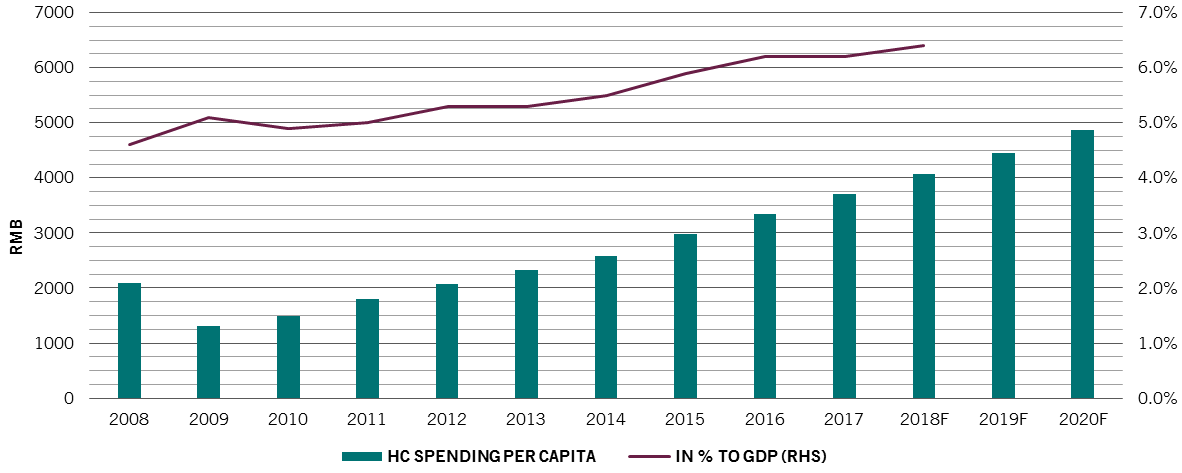

"On the growth side, the transformation of China and the economy continues. Healthcare and higher value-add production will be structural winners in the future," she says (see chart), adding that the team is not particularly positive on the wider consumer sector. The tech sector will remain uneventful and lacklustre as it transitions towards the implementation of 5G.

China healthcare spending per capital and ratio, % of gdp

(2008-2020F)

Market sentiment will continue to be fragile, and the immediate direction of travel for many stocks will be less clear. Even the long-term winners may not escape negative sentiment and the macro economic conditions that weigh on the whole market.

"From a bottom-up perspective, we look for earnings visibility that will be rewarded by the market, as all investors do. But with the headwinds, we are cautious on consumer balance sheets and the deleveraging of China’s debt. Sales of large ticket item may be weak," she says.

No investor wants to put all their eggs in one basket, especially when market conditions are quite so challenging. A typical strategy is to diversify the choice of assets, mixing the promise of growth from stocks with the more defensive attributes of bonds. When turbulence hits, investors reduce their equity exposure and seek capital protection from bonds where they can.

Since the global financial crisis, that inverse correlation has been eroded. Long-only mixed asset strategies have lost much of their diversification benefits as equities and bonds have risen and corrected in unison. When that happens, capital protection is sharply reduced when both asset classes fall.

"The combination of equity and bonds no longer diversifies; the relationship simply does not work. Quantitative tightening is unlikely to help as rate rises spread from the US to Europe and on to Asia and China," she says.

A long-short strategy such as Pictet Mandarin Total Return may offer investors a solution that benefits from long-term structural gains but protects when market conditions are weak. The strategy invests in long equity positions in A- and H-shares, with some exposure to international stocks with a strong Chinese element to their business success. It can also play on general market or individual stock weaknesses through short positions and derivatives that deliver performance when assets fall in absolute or relative terms.

"From a long-term perspective, we want to stay in the market for the growth. But we also need to protect our investors from the volatility. When markets are conducive to risk, we raise our net long exposure. We can also bet against falls, smoothing out the troughs and adding to overall performance,’ says Wang Simond.

Long-short strategies also offer additional benefits in Greater China where the range between strong and weak performing stocks tends to be greater than in developed markets like the S&P 500. Betting on the rising stars and against the fallen angels can lead to excess returns. As Wang Simond points out, that wide dispersion is set to continue as global trade tensions occupy investors’ minds and monetary tightening takes hold.

Investing in the A- and H-share universe offers a wide range of sectors, companies and market capitalisations. The bottom-up team analyses each sector, looking for those firms that are likely to benefit from growth and structural change, and for those that look set to fall behind. Positions are then taken on a directional view, identifying winners and losers or relative value through pair trades.

Positions in single names are played through physical equities or derivatives that offer an equity-like returns, particularly for short positions. The team can also manage the sensitivity of the portfolio to the market using indices, typically through options and futures.

"The key to long-short is risk management, especially as we run an emerging market strategy that offers investors daily liquidity."

"Whether long or short, our investments tend to be mainly in liquid large or mega-cap stocks so we can change position quickly if needed," she explains.

Look past market noise to focus on high conviction long/short views.

The team also has plenty of experience to help guide them through tricky markets. Wang Simond has been investing in the region for more than 25 years and survived many market cycles and macro-driven periods of market instability. The team also has recourse to the global Pictet Asset Management team and infrastructure. With operations and trading taken care of, the team can devote 100 per cent of its time to running the strategy and seeking out long-short opportunities at stock and market level.

China’s desire to open its markets to global investors is good news for investors like Wang Simond and the Mandarin Total Return team. Historically, China restricted which shares could be shorted and when. The opening of the Stock Connect programmes that link the markets of Hong Kong, Shanghai and Shenzen has increased the availability of tools at their disposal. China’s inclusion in the MSCI indices means new market- and index-level shorting instruments will become more mainstream over time.

The team may call heavily on its range of skills, resources and investment tools as 2019 unfolds. With markets and stocks having re-valued significantly, there is plenty of opportunity to find solid stocks that are significantly under-priced. Equally, there are also stocks that have seen their prices fall for good reason. The trick is to decide which is which and for what reason, then position appropriately.

‘The opportunities have opened up, but which are real opportunities or a justified downgrade? We aim to build a constructive view but we prepare for the worst and for volatility too,’ says Wang Simond.

‘Our focus is always on stock selection, not the geo-politics. But any negatives on the world stage will always have an effect on sentiment and liquidity in the region as inflows can change direction quickly,’ she adds.

Important legal information

This marketing material is issued by Pictet Asset Management (Europe) S.A.. It is neither directed to, nor intended for distribution or use by, any person or entity who is a citizen or resident of, or domiciled or located in, any locality, state, country or jurisdiction where such distribution, publication, availability or use would be contrary to law or regulation. The latest version of the fund‘s prospectus, Pre-Contractual Template (PCT) when applicable, Key Information Document (KID), annual and semi-annual reports must be read before investing. They are available free of charge in English on www.assetmanagement.pictet or in paper copy at Pictet Asset Management (Europe) S.A., 6B, rue du Fort Niedergruenewald, L-2226 Luxembourg, or at the office of the fund local agent, distributor or centralizing agent if any.

The KID is also available in the local language of each country where the compartment is registered. The prospectus, the PCT when applicable, and the annual and semi-annual reports may also be available in other languages, please refer to the website for other available languages. Only the latest version of these documents may be relied upon as the basis for investment decisions.

The summary of investor rights (in English and in the different languages of our website) is available here and at www.assetmanagement.pictet under the heading "Resources", at the bottom of the page.

The list of countries where the fund is registered can be obtained at all times from Pictet Asset Management (Europe) S.A., which may decide to terminate the arrangements made for the marketing of the fund or compartments of the fund in any given country.

The information and data presented in this document are not to be considered as an offer or solicitation to buy, sell or subscribe to any securities or financial instruments or services.

Information, opinions and estimates contained in this document reflect a judgment at the original date of publication and are subject to change without notice. The management company has not taken any steps to ensure that the securities referred to in this document are suitable for any particular investor and this document is not to be relied upon in substitution for the exercise of independent judgment. Tax treatment depends on the individual circumstances of each investor and may be subject to change in the future. Before making any investment decision, investors are recommended to ascertain if this investment is suitable for them in light of their financial knowledge and experience, investment goals and financial situation, or to obtain specific advice from an industry professional.

The value and income of any of the securities or financial instruments mentioned in this document may fall as well as rise and, as a consequence, investors may receive back less than originally invested.

The investment guidelines are internal guidelines which are subject to change at any time and without any notice within the limits of the fund's prospectus. The mentioned financial instruments are provided for illustrative purposes only and shall not be considered as a direct offering, investment recommendation or investment advice. Reference to a specific security is not a recommendation to buy or sell that security. Effective allocations are subject to change and may have changed since the date of the marketing material.

Past performance is not a guarantee or a reliable indicator of future performance. Performance data does not include the commissions and fees charged at the time of subscribing for or redeeming shares.

Any index data referenced herein remains the property of the Data Vendor. Data Vendor Disclaimers are available on assetmanagement.pictet in the “Resources” section of the footer. This document is a marketing communication issued by Pictet Asset Management and is not in scope for any MiFID II/MiFIR requirements specifically related to investment research. This material does not contain sufficient information to support an investment decision and it should not be relied upon by you in evaluating the merits of investing in any products or services offered or distributed by Pictet Asset Management.

Pictet AM has not acquired any rights or license to reproduce the trademarks, logos or images set out in this document except that it holds the rights to use any entity of the Pictet group trademarks. For illustrative purposes only.