Select your investor profile:

This content is only for the selected type of investor.

Individual investors?

Rewarding stress: investing in distressed securities

Special situations investing offers potentially attractive returns at all points of the investment cycle.

Written by

Galia Velimukhametova

Senior Investment Manager

Gareth Payne

Head of Credit & Alternative Fixed Income Client Portfolio Management

Britain’s high street might be an unfolding catastrophe – celebrity chef Jamie Oliver’s eponymous chain is just the latest in a litany of failing mid-market eateries and retailers – but it also represents an opportunity.

Indeed, this isn’t just true of the UK. DIA in Spain, Steinhoff, listed in Germany and South Africa, and French group Rallye have all come under financial stress recently, allowing adept investors to generate attractive returns.

The ability to either buy or short sell a company’s debt, according to circumstance, is at the heart of this sort of special situations investing. For instance, if the market has yet to fully price in how much a company is struggling financially, it’s possible to make a return by selling its debt short. This involves close analysis of stressed corporate credit, which is to say when it trades below its face value and its yield rises to 10 percentage points above benchmark government bonds with the same maturities.

Then, when the issuing company defaults or enters bankruptcy – in other words the debt becomes distressed – skilled investors can earn returns by buying back the debt if they anticipate the company will be successfully restructured or if its remaining assets are undervalued.

An approach for all seasons

Historically, this style of investing has generated strong returns. Over the past 20 years, investing in distressed fixed income has achieved annual returns of 7.2 per cent against 6.8 per cent for global high yield bonds1.

One reason for this is the asymmetric nature of credit. Normally trading corporate debt generally doesn’t offer much upside – a sudden improvement in a bond issuer’s credit ratings or falling government bond yields can give some uplift, but by and large most of the return comes in the form of regular interest payments. By contrast, if a bond issuer defaults, the hit to a fixed income portfolio can be heavy and long-lasting. Which is why shorting the fully-priced debt of companies running into problems can be so rewarding.

By the same token, the potential gains from buying and holding distressed debt can also be significant – not least because once companies go into default markets often underappreciate the true value of their debt securities, particularly when they don’t trade very often.

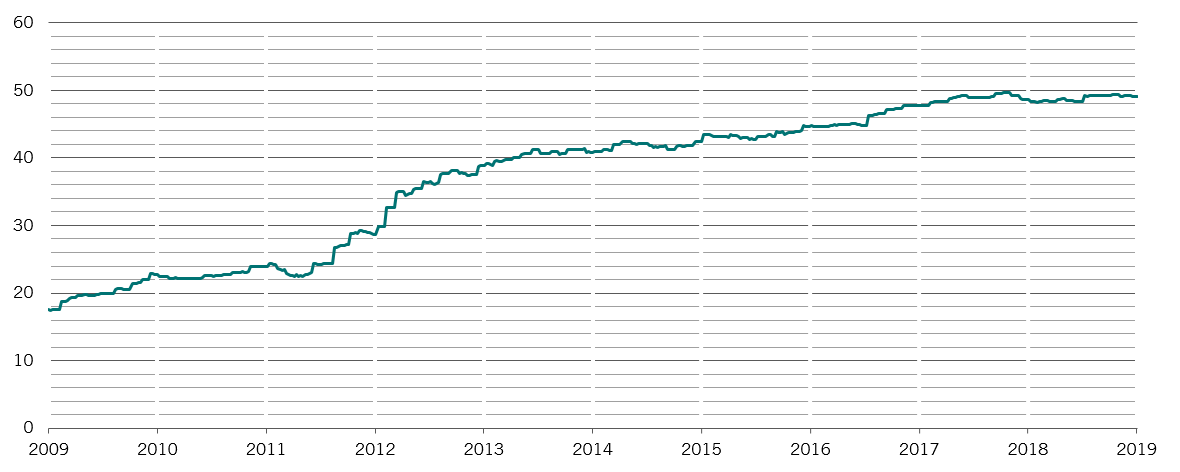

Killer b's

BBB-rated euro-denominated universe, % of total market value

Distressed assets can also add stability to a diversified portfolio. In contrast to equities and higher grade corporate bonds, which tend to perform badly in economic downturns, that’s a time when it becomes particularly rewarding to short struggling corporate credit.

The asset class has typically delivered positive returns when traditional asset classes, and particularly equities, tend to be doing badly. Companies tend to take on debt during good times and then suffer when the business cycle turns.

But because it’s always possible to find struggling firms, even when default rates are negligible, special situations investing can generate strong net returns over the whole of the cycle. The most flexible total return strategies involve both selling debt short and taking long positions – with the added bonus that returns from these investments don’t tend to move in lockstep with major asset classes.

European attractions

That’s why special situations investing as a strategy is attractive even in an era characterised by low corporate default rates.

It’ll be even more compelling when those defaults start to increase, as they inevitably will. True, trying to time cycles is far from straightforward; most strategies avoid it. But it’s also important to remember that policymakers have yet to find a way of abolishing the cyclical nature of business. For instance, US companies are as indebted relative to earnings before charges as they were during the 2001 and early 1990s recessions and in worse shape than they were going into the global financial crisis. Even now, when default rates are low, the opportunity set for investors in distressed and stressed assets is significant given how much larger corporate debt markets are now than they were in the past. And investors with the flexibility to invest across the corporate capital structure – equity as well as debt – are even more able to take advantage of these situations.

At the same time, a record proportion of this debt is rated BBB, the lowest investment grade credit rating, which makes for a fragile market. It’s worth noting that the proportion of stressed credits has spiked as worsening trade tensions between the US and China prompted investors to be ruthless with companies that had posted disappointing earnings in recent weeks. In May, for instance, the number of European high yield credits that fell into stressed territory – which is to say, saw their prices fall below 90 – has jumped to 85 from 50 the previous month.

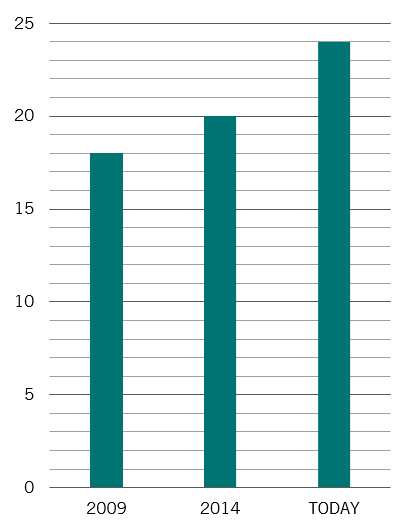

zombies

Russell 2000 companies with interest coverage ratio less than 1, using 1-year interest coverage and 3-year average free cash flow

In this environment, 12 per cent of European companies are zombies, which is to say their earnings fail to cover interest costs, not far below the pre-quantitative easing peak of 14 per cent. This will provide a huge opportunity set to long/short distressed strategies as rates normalise and these companies struggle to service their debt.

In fact, the inversion of the US yield curve points to a US recession next year. Throw in populist politics and the US-China trade war and the outlook looks increasingly gloomy. And where the US economy goes, others tend to follow.

The US, however, is not an especially rich hunting ground for special situations investors. Special situations investing is well established there and defaults are low, leaving many managers chasing relatively few prospects.

Europe, on the other hand, offers good opportunities for special situations investing. There is relatively little competition for stressed and distressed assets which makes for favourable valuations. But this also demands rigorous in-house credit analysis, where specialists with long experience can effectively parse and interpret covenants. Broad, well-established teams are crucial to maximising investor performance.

Furthermore, the fragmented nature of the market, with multiple jurisdictions, various languages and varied investment cultures, makes it a much more complex environment, leaving the field open for investors with local knowledge.

Unlike, say, equity investing where markets tend to be broad, liquid and transparent, distressed debt also often demands good contacts across a wide variety of industries – not to mention local structuring and legal advisors – to find, understand and prosper from the best deals. For instance, right now secular shifts mean that opportunities are popping up in retail, shipping construction and oil services in particular.

The virtues of analysis

But those qualities come with a cost: successful investing in special situations demands a very active approach, based on thorough analytical work. Risks can also be significant. Stressed and distressed debt has often been issued by relatively small companies – so there’s not much of it in the market – or potential market participants have been scared off, or both. In that case it’s important to find the most liquid of these securities, which is to say the ones with large capital structures, in order to minimise volatility and ensure an ability to exit the investment.

Tailoring the investments requires additional skill. It’s important to have an appropriate mix of short and long positions to ensure that the strategy is doing more than just capturing market effects. Shorts also help to develop ideas for what might be successful future long positions.

One key consideration for investors is liquidity. Although buying illiquid distressed assets like loans or credit of companies with small capital structures can ultimately be rewarding, this often means locking up money for long periods. This can suit private equity investors, but hedged or absolute return strategies will look for investments that are easier to get in and out of. Focus on more liquid investments means shorter holding periods – for an absolute return approach that can mean 12 months rather than the 5 to 7 years for an average private equity fund.

Europe offers good opportunities for special situations investing.

This style of investing has the further advantages of being less management intensive than private equity funds, and of using less leverage. It makes sense to avoid pools of non-performing loans, for example, as they have less transparency on underlying assets, which makes it harder to value them in an informed way. On the other hand, having the flexibility to trade sovereign debt can help an investor’s liquidity profile.

But even investing in more liquid assets requires patience – it can take time for good trades to come up or for distressed positions to bear fruit. At the same time, investors need to be able to take substantial positions when good opportunities roll around.

In all, it’s a market where substantial experience is important, not just to develop the contacts and understand the sort of analysis needed but also to know which opportunities present themselves at different points of the business cycle.

This marketing material is issued by Pictet Asset Management (Europe) S.A.. It is neither directed to, nor intended for distribution or use by, any person or entity who is a citizen or resident of, or domiciled or located in, any locality, state, country or jurisdiction where such distribution, publication, availability or use would be contrary to law or regulation. The latest version of the fund‘s prospectus, Pre-Contractual Template (PCT) when applicable, Key Investor Information Document (KIID), annual and semi-annual reports must be read before investing. They are available free of charge in English on www.assetmanagement.pictet or in paper copy at Pictet Asset Management (Europe) S.A., 15 avenue J.F. Kennedy, L-1855 Luxembourg, or at the office of the fund local agent, distributor or centralizing agent if any. The KIID is also available in the local language of each country where the compartment is registered. The prospectus, the PCT when applicable, and the annual and semi-annual reports may also be available in other languages, please refer to the website for other available languages. Only the latest version of these documents may be relied upon as the basis for investment decisions.

The summary of investor rights (in English and in the different languages of our website) is available here and at www.assetmanagement.pictet under the heading "Resources", at the bottom of the page.

The list of countries where the fund is registered can be obtained at all times from Pictet Asset Management (Europe) S.A., which may decide to terminate the arrangements made for the marketing of the fund or compartments of the fund in any given country.

The information and data presented in this document are not to be considered as an offer or solicitation to buy, sell or subscribe to any securities or financial instruments or services.

Information, opinions and estimates contained in this document reflect a judgment at the original date of publication and are subject to change without notice. Pictet Asset Management (Europe) S.A. has not taken any steps to ensure that the securities referred to in this document are suitable for any particular investor and this document is not to be relied upon in substitution for the exercise of independent judgment. Tax treatment depends on the individual circumstances of each investor and may be subject to change in the future. Before making any investment decision, investors are recommended to ascertain if this investment is suitable for them in light of their financial knowledge and experience, investment goals and financial situation, or to obtain specific advice from an industry professional.

The value and income of any of the securities or financial instruments mentioned in this document may fall as well as rise and, as a consequence, investors may receive back less than originally invested.

The investment guidelines are internal guidelines which are subject to change at any time and without any notice within the limits of the fund's prospectus.

The mentioned financial instruments are provided for illustrative purposes only and shall not be considered as a direct offering, investment recommendation or investment advice. Reference to a specific security is not a recommendation to buy or sell that security. Effective allocations are subject to change and may have changed since the date of the marketing material.

Past performance is not a guarantee or a reliable indicator of future performance. Performance data does not include the commissions and fees charged at the time of subscribing for or redeeming shares.

Any index data referenced herein remains the property of the Data Vendor. Data Vendor Disclaimers are available on assetmanagement.pictet in the “Resources” section of the footer.

This document is a marketing communication issued by Pictet Asset Management and is not in scope for any MiFID II/MiFIR requirements specifically related to investment research. This material does not contain sufficient information to support an investment decision and it should not be relied upon by you in evaluating the merits of investing in any products or services offered or distributed by Pictet Asset Management.

Pictet AM has not acquired any rights or license to reproduce the trademarks, logos or images set out in this document except that it holds the rights to use any entity of the Pictet group trademarks. For illustrative purposes only.