EM Monitor - the fiscal response by emerging markets to Covid 19

June 2020

Marketing Material

EMs walk the line - analysing the fiscal response

In our last edition we covered the monetary response to Covid 19 in emerging markets. This time we look at the fiscal side: which markets are making the biggest adjustments and which seem at greater risk? The troubled trio of Brazil, Turkey, South Africa look particularly vulnerable.

Written by

Patrick Zweifel

Chief Economist

Share this article

Suffering CADs

As in prior episodes of high risk-aversion, it is the currencies of emerging markets that are most reliant on external investors for financing that have suffered the most. The currencies of these current-account-deficit (CAD) markets are down -13% year to date. Let’s study these markets in more detail: India, Indonesia, Malaysia, Brazil, Mexico, Colombia, Turkey & South Africa.

Not as big as you think...

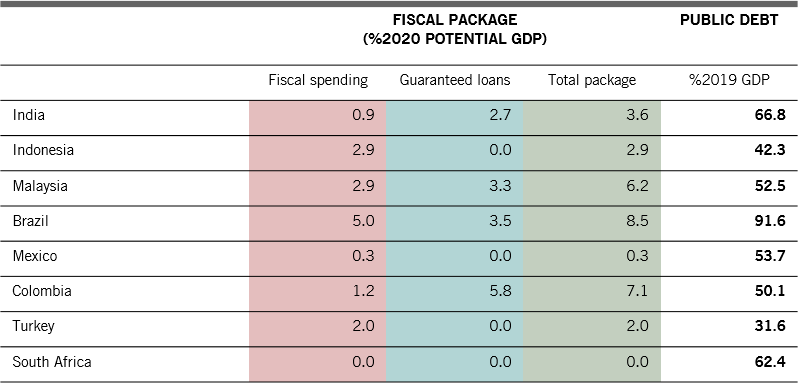

At first glance, total fiscal packages for the eight countries under consideration appear large (e.g. 8.5% of GDP for Brazil or 7.1% for Colombia). Yet a big chunk are guaranteed loans - bridge loans to companies to allow them to survive the crisis - which will not necessarily add to public debt as they should be repaid. ‘Should’ is the key word here, as it assumes that these firms will not default or that governments will not forgive their loans.

Release the pressure

Fig. 1 - Fiscal packages for 8 principal CAD emerging markets

Source: Pictet Asset Management, CEIC, Refinitiv, May 2020

Brazil at most risk

Focusing only on fiscal spending that will impact the debt level, these EMs appear to have generally struck a good balance between necessity and affordability - all apart from Brazil.

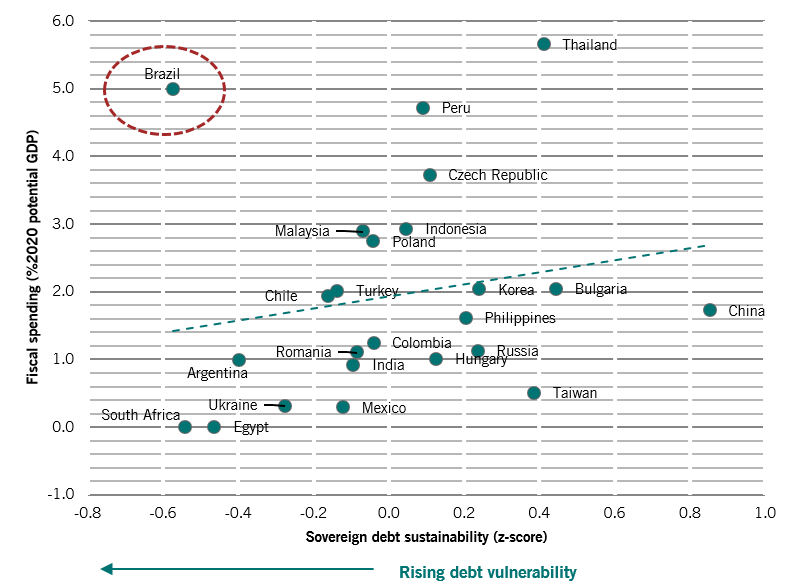

But public debt is just one indicator we think should be considered. Using six inputs to compile our proprietary sovereign debt sustainability score, we then track this in fig.2 below against the fiscal stimulus in the different markets.

This shows that the larger fiscal stimulus packages have come from those countries on a more sustainable debt footing. Or conversely: the higher the sovereign risk, the weaker the fiscal stimulus. Examples of high debt and low stimulus include South Africa and India. Again the notable exception is Brazil, which has just passed the second largest budget in EM after Thailand, worth BRL380bn.

Odd one out

Fig. 2 - EM fiscal spending & sovereign debt sustainability score

Source: Pictet Asset Management, CEIC, Refinitiv, May 2020

Brazil aside, fiscal deterioration should be much smaller in emerging markets than in advanced economies. The median direct fiscal stimulus in EM being 1.6% of GDP which compares to 4.2% for advanced economies. Moreover, EMs have generally been much more cautious in providing guaranteed loans to the private sector than in developed markets.

The path through the woods

But can you be too cautious? A clear risk is that smaller fiscal packages are ineffective and ultimately lead to a higher costs for the overall economy. This is because fiscal deterioration comes anyway as a collapse in activity leads to a loss in fiscal revenues via lower tax receipts. For example, we forecast in South Africa a nominal fall in GDP of -3.7% in 2020 should result in a contraction of 5% in fiscal revenues.

A clear risk is that smaller fiscal packages are ineffective.

This is the delicate path certain current-account-deficit emerging markets will need to tread in coming months: over-stimulate fiscally and you risk raising your debt burden to unsustainable levels and crashing your currency and economy, but under-stimulate and an economic slump will shrink fiscal revenues and crash the currency.

The importance of a stable base

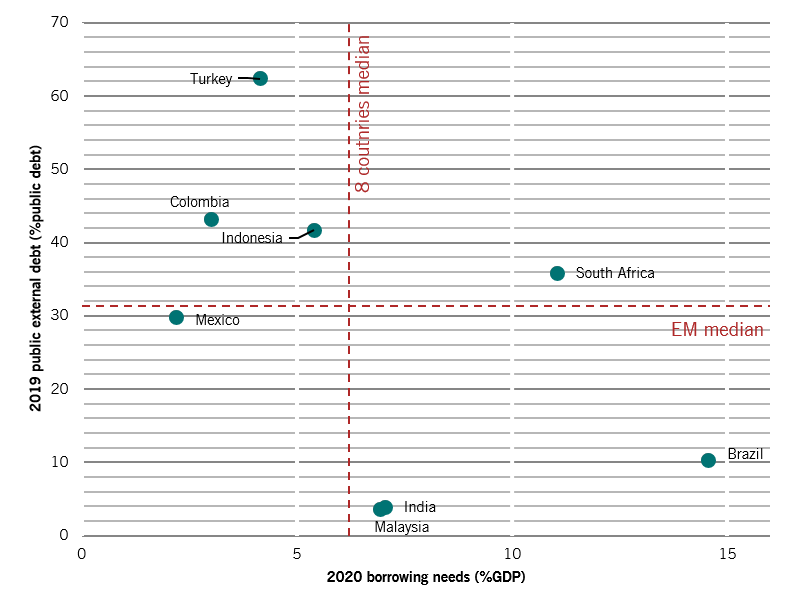

A key factor to consider is the share of domestic investors versus overseas. As fig.3 below shows, markets that score well with more than 85% of their public debt held domestically are Brazil, India & Malaysia. Others such as, Colombia, Indonesia, South Africa and, in particular, Turkey have overseas investor bases above the EM median.

Bringing it all together

Fig. 3 - EM borrowing needs & external public debt (%total public debt)

Source: Pictet Asset Management, CEIC, Refinitiv

The troubled trio

Overall, Brazil has the most sizeable borrowing needs, while Turkey is the most exposed to foreign investors. South Africa however looks the most vulnerable as it has both a significant deficit to finance and a high share of its debt held externally.

About

Patrick Zweifel

Patrick Zweifel joined Pictet in 1997. He is Chief Economist at Pictet Asset Management, having assumed the position in 2009. Before that, he was head of the “Macro Research Team” at Pictet Private Wealth Management, where he was responsible for emerging markets and Japan, and for the development of quantitative models on major asset classes. Before joining Pictet he was a research assistant in econometrics and monetary theory and worked on international research projects for the World Bank and the European Union. He holds a PhD in Econometrics from the University of Lausanne.

About

Sabrina Khanniche

Sabrina Khanniche joined Pictet Asset Management in 2011. She is a Senior Economist, Lead on Eurozone and MEA.

Before joining Pictet, she was with Groupama Asset Management during four years as a Financial Engineer in charge of the analysis and modelling of hedge fund risks. In this regard, she published and presented her work in international academic conferences.

Sabrina holds a Master and a PhD in Economics from the University of Paris West Nanterre La Défense.

About

Nikolay Markov

Nikolay Markov joined Pictet Asset Management in 2013. He is a Senior Economist, Lead on CEE and Other advanced economies.

Before joining Pictet, he was working in the Monetary Policy Analysis Unit of the Swiss National Bank where he performed research on monetary policy rules for Switzerland. Prior to working at the Swiss National Bank he was a teaching and research assistant at the University of Geneva and participated in international academic conferences.

Nikolay holds a PhD in Economics from the University of Geneva and obtained a PhD program certificate from the Swiss National Bank doctoral institute in Gerzensee.

About

Anjeza Kadilli

Anjeza Kadilli joined Pictet in 2015. She is an Senior Economist in Pictet Asset Management’s Economic Analysis team where she conducts macroeconomic analysis of emerging markets. Anjeza holds a PhD in Econometrics from the University of Geneva - where she also obtained an MSc and BSc in Economics. During her PhD, Anjeza spent time at the University of Southern California, Riksbank and HEC Montreal as a visiting scholar.

About

Lola Saugy

Lola Saugy joined Pictet Asset Management in 2018 as part of the firm’s Graduate Programme. She is now a Quantitative Economic Analyst within the Economic Analysis team in Geneva. Lola holds a Master of Science in Applied Mathematics from the Ecole Polytechnique Fédérale de Lausanne. She did her master thesis at Harvard University in the field of biostatistics, as a visiting scientist.

This marketing material is issued by Pictet Asset Management (Europe) S.A.. It is neither directed to, nor intended for distribution or use by, any person or entity who is a citizen or resident of, or domiciled or located in, any locality, state, country or jurisdiction where such distribution, publication, availability or use would be contrary to law or regulation. The latest version of the fund‘s prospectus, Pre-Contractual Template (PCT) when applicable, Key Investor Information Document (KIID), annual and semi-annual reports must be read before investing. They are available free of charge in English on www.assetmanagement.pictet or in paper copy at Pictet Asset Management (Europe) S.A., 15 avenue J.F. Kennedy, L-1855 Luxembourg, or at the office of the fund local agent, distributor or centralizing agent if any. The KIID is also available in the local language of each country where the compartment is registered. The prospectus, the PCT when applicable, and the annual and semi-annual reports may also be available in other languages, please refer to the website for other available languages.Only the latest version of these documents may be relied upon as the basis for investment decisions.

The summary of investor rights (in English and in the different languages of our website) is available here and at www.assetmanagement.pictet under the heading "Resources", at the bottom of the page.

The list of countries where the fund is registered can be obtained at all times from Pictet Asset Management (Europe) S.A., which may decide to terminate the arrangements made for the marketing of the fund or compartments of the fund in any given country.

The information and data presented in this document are not to be considered as an offer or solicitation to buy, sell or subscribe to any securities or financial instruments or services.

Information, opinions and estimates contained in this document reflect a judgment at the original date of publication and are subject to change without notice. Pictet Asset Management (Europe) S.A. has not taken any steps to ensure that the securities referred to in this document are suitable for any particular investor and this document is not to be relied upon in substitution for the exercise of independent judgment. Tax treatment depends on the individual circumstances of each investor and may be subject to change in the future. Before making any investment decision, investors are recommended to ascertain if this investment is suitable for them in light of their financial knowledge and experience, investment goals and financial situation, or to obtain specific advice from an industry professional.

The value and income of any of the securities or financial instruments mentioned in this document may fall as well as rise and, as a consequence, investors may receive back less than originally invested.

The investment guidelines are internal guidelines which are subject to change at any time and without any notice within the limits of the fund's prospectus.

The mentioned financial instruments are provided for illustrative purposes only and shall not be considered as a direct offering, investment recommendation or investment advice. Reference to a specific security is not a recommendation to buy or sell that security. Effective allocations are subject to change and may have changed since the date of the marketing material.

Past performance is not a guarantee or a reliable indicator of future performance. Performance data does not include the commissions and fees charged at the time of subscribing for or redeeming shares.

Any index data referenced herein remains the property of the Data Vendor. Data Vendor Disclaimers are available on assetmanagement.pictet in the “Resources” section of the footer.

This document is a marketing communication issued by Pictet Asset Management and is not in scope for any MiFID II/MiFIR requirements specifically related to investment research. This material does not contain sufficient information to support an investment decision and it should not be relied upon by you in evaluating the merits of investing in any products or services offered or distributed by Pictet Asset Management.

Pictet AM has not acquired any rights or license to reproduce the trademarks, logos or images set out in this document except that it holds the rights to use any entity of the Pictet group trademarks. For illustrative purposes only.

Cookie Policy

This website uses cookies to enhance user navigation and to collect statistical data. To refuse the use of cookies, change your settings or for more information, please click on the following link: Cookies policy. By continuing to browse this website, you accept the use of cookies for the above purposes.