EM Monitor - Impact of Covid-19 on EM labour markets

October 2020

Marketing Material

Colombia and Peru in the grip of the Covid-19 economic crisis

Unemployment in Peru and Colombia has surged in the face of the Covid crisis. We look at how their respective governments are tackling the challenge.

Written by

Anjeza Kadilli

Senior Economist

Lola Saugy

Quantitative Economic Analyst

Share this article

Unemployment double pre-Covid crisis levels

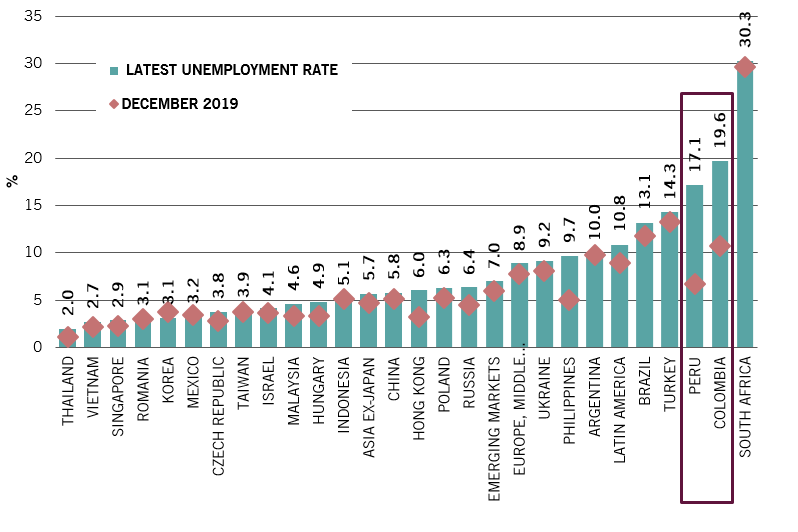

Colombia and Peru stand out in emerging markets by the surge in their unemployment rate (Fig.1). Nearly one in five people are unemployed in Colombia, while in Peru, unemployment has jumped from 6.8 per cent in December 2019 to 17.1 per cent based on the latest available data.

Fig.1 - EM unemployment rate: latest available versus December 2019

We think the employment outlook is likely to deteriorate because:

current figures do not account for underemployment, or only partially;

lower labour participation rates1 have biased unemployment rates to the downside. In other words, had the participation rate been constant, the unemployment rate would have been much higher.

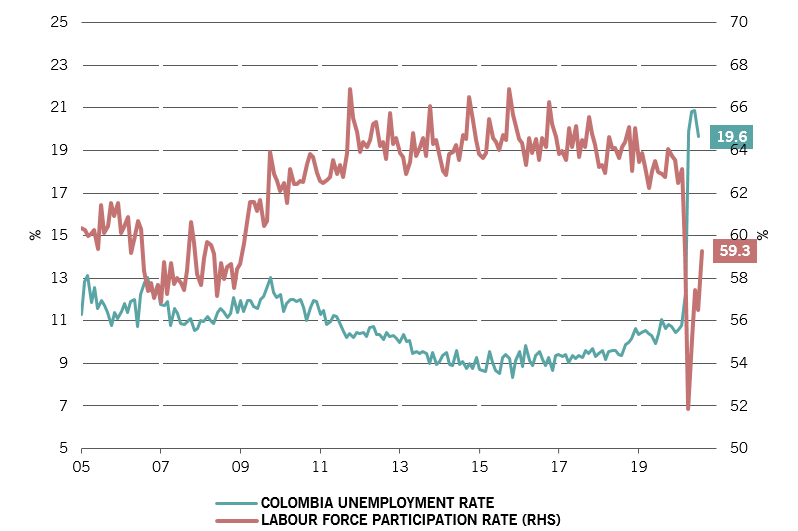

In Colombia, labour force participation fell sharply (Fig. 2), from 63.2 per cent in February to 51.8 per cent in April, excluding many from unemployment figures. As of August, there are an estimated 2.7 million fewer jobs and 1.7 million more inactive workers relative to February at a national level2. Had all workers remained active with these levels of employment, the unemployment rate would be higher than the current 19.6 per cent.

Fig.2 - Colombia: unemployment rate & labour force participation rate

Source: Pictet Asset Management, CEIC, Refinitiv, Bloomberg. Unemployment rate data to July 2020; participation rate to August 2020.

In Peru, 7 million people lost their jobs between February and June, pushing the unemployment rate to 16.7 per cent in June. At the same time, 6.8 million dropped out of the labour force. Unemployment would currently top 43 per cent if those workers were still included as unemployed3.

Smaller firms (up to 10 workers) have been the most affected, with a 65.5 per cent free fall in employment over a year ago (oya). By comparison, employment fell by 36.5 per cent oya in larger firms (more than 50 workers).

Tackling the challenge...

In Colombia, lackluster labour demand has been tied to economic activity, hindered by further lockdowns in cities, making urban employment recovery more volatile.

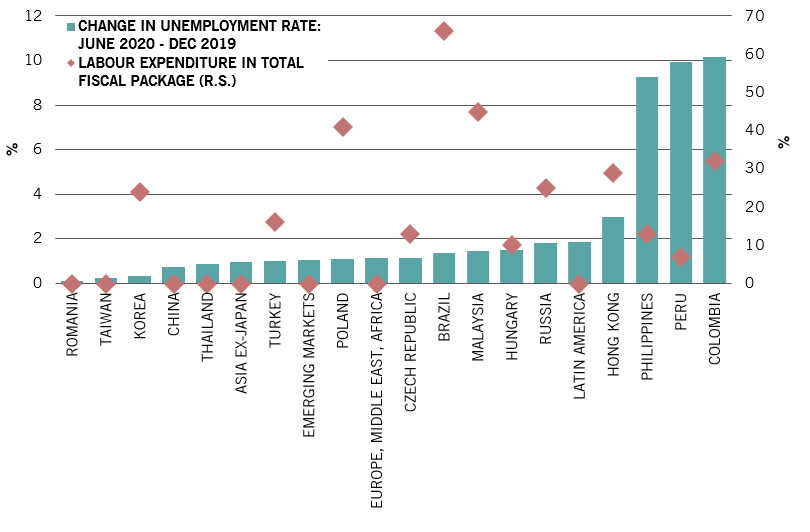

A third of the fiscal stimulus (2.5 per cent of GDP) is directed towards job retention schemes (Fig.3). This takes the form of credit to struggling SMEs and postponement of income tax payment; subsidised payrolls for companies with a 20 per cent income loss for up to three months.

August’s labour national survey data shows gains in the participation rate, which is now up to 59.3 per cent, closer to its pre-pandemic level. The reopening of more sectors clearly had a positive impact on employment.

Fig.3 - Change in unemployment rate (December 2019 to June 2020) & fiscal spending

In Peru, only 5 per cent of the fiscal stimulus (4.6 per cent of GDP) funds job retention schemes. In addition to tax relief arrangements and other measures introduced to support companies and the poorer population, the government has launched the “Arranca Peru” (Peru jumpstarts) programme, for a value of USD1.8 billion. The aim is to create more than 1 million public-sector jobs in areas such as transportation, communication and housing.

Job losses during the health crisis have been significant. Only a share of those lost jobs have been recovered in recent months, and not at the same conditions. It is likely that the normalisation of employment will continue for the remaining of 2020, but the drop in conditions weigh on wages and households’ spending.

THE VIEW FROM OUR EM DEBT TEAM

By Mary-Therese Barton, Head of Emerging Market Debt

Despite challenges in the region, such as the examples presented above, we believe that Latin America can still offer long-term investment opportunities for the following key reasons:

Although LatAM was one of the hardest hit regions by COVID, economic growth has started to recover, albeit lagging behind other EM regions;

The region has delivered extensive fiscal and monetary support which will continue to be supportive for the economic recovery;

LatAm central banks are close to the end of their easing cycle and there is little room for further monetary stimulus, but our expectation is that rates will remain at their lower bound for some time;

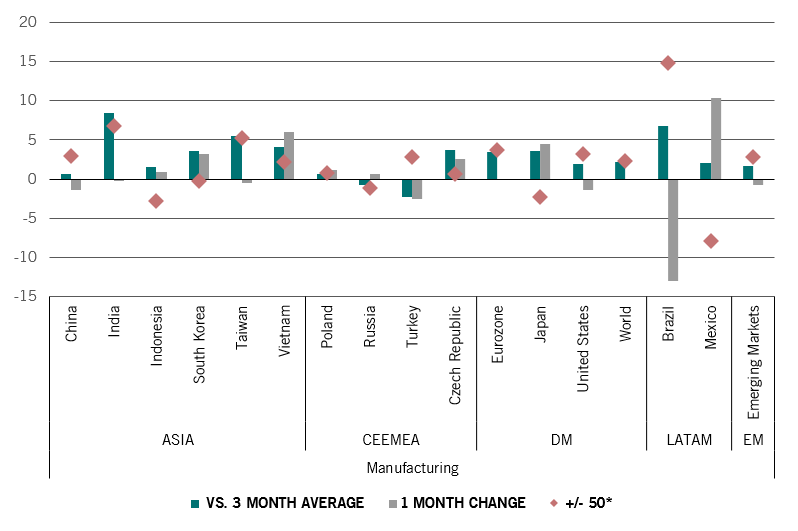

Manufacturing production is recovering fast (see chart below);

A faster than expected US recovery could provide further support.

At a country level, Brazil has shown improving manufacturing activity over the last 3 months, despite a drop in September (1-month change). An increasingly large fiscal deficit however needs to be monitored closely.

The fiscal response in Mexico has been generally well handled with the country running a relatively small fiscal deficit and we are starting to see improved manufacturing data emerge.

Manufacturing PMIs by region

Source: Bloomberg, Pictet Asset Management, 01.10.2020. * +/-50: A reading above 50 indicates an expansion of the manufacturing sectors whereas below 50 indicates a contraction.

Mary-Therese Barton was appointed Chief Investment Officer - Fixed Income in October 2023. She was previously Head of Emerging Market Fixed Income, overseeing the Emerging Market Sovereign, Corporate and Greater China debt strategies. She joined Pictet Asset Management in 2004.

Prior to joining Pictet she worked at Dun & Bradstreet, where she was an economist responsible for analysing European countries.

Mary-Therese graduated with a BA (Hons) in Philosophy, Politics and Economics from Balliol College, Oxford. She also holds an MSc with distinction in Development Finance from the Centre for Financial Management Studies, SOAS (School of Oriental and African Studies), part of the University of London. Mary-Therese is also a Chartered Financial Analyst (CFA) charterholder.

About

Anjeza Kadilli

Anjeza Kadilli joined Pictet in 2015. She is an Senior Economist in Pictet Asset Management’s Economic Analysis team where she conducts macroeconomic analysis of emerging markets. Anjeza holds a PhD in Econometrics from the University of Geneva - where she also obtained an MSc and BSc in Economics. During her PhD, Anjeza spent time at the University of Southern California, Riksbank and HEC Montreal as a visiting scholar.

About

Lola Saugy

Lola Saugy joined Pictet Asset Management in 2018 as part of the firm’s Graduate Programme. She is now a Quantitative Economic Analyst within the Economic Analysis team in Geneva. Lola holds a Master of Science in Applied Mathematics from the Ecole Polytechnique Fédérale de Lausanne. She did her master thesis at Harvard University in the field of biostatistics, as a visiting scientist.

Share this article

This marketing material is issued by Pictet Asset Management (Europe) S.A.. It is neither directed to, nor intended for distribution or use by, any person or entity who is a citizen or resident of, or domiciled or located in, any locality, state, country or jurisdiction where such distribution, publication, availability or use would be contrary to law or regulation. The latest version of the fund‘s prospectus, Pre-Contractual Template (PCT) when applicable, Key Investor Information Document (KIID), annual and semi-annual reports must be read before investing. They are available free of charge in English on www.assetmanagement.pictet or in paper copy at Pictet Asset Management (Europe) S.A., 15 avenue J.F. Kennedy, L-1855 Luxembourg, or at the office of the fund local agent, distributor or centralizing agent if any. The KIID is also available in the local language of each country where the compartment is registered. The prospectus, the PCT when applicable, and the annual and semi-annual reports may also be available in other languages, please refer to the website for other available languages.Only the latest version of these documents may be relied upon as the basis for investment decisions.

The summary of investor rights (in English and in the different languages of our website) is available here and at www.assetmanagement.pictet under the heading "Resources", at the bottom of the page.

The list of countries where the fund is registered can be obtained at all times from Pictet Asset Management (Europe) S.A., which may decide to terminate the arrangements made for the marketing of the fund or compartments of the fund in any given country.

The information and data presented in this document are not to be considered as an offer or solicitation to buy, sell or subscribe to any securities or financial instruments or services.

Information, opinions and estimates contained in this document reflect a judgment at the original date of publication and are subject to change without notice. Pictet Asset Management (Europe) S.A. has not taken any steps to ensure that the securities referred to in this document are suitable for any particular investor and this document is not to be relied upon in substitution for the exercise of independent judgment. Tax treatment depends on the individual circumstances of each investor and may be subject to change in the future. Before making any investment decision, investors are recommended to ascertain if this investment is suitable for them in light of their financial knowledge and experience, investment goals and financial situation, or to obtain specific advice from an industry professional.

The value and income of any of the securities or financial instruments mentioned in this document may fall as well as rise and, as a consequence, investors may receive back less than originally invested.

The investment guidelines are internal guidelines which are subject to change at any time and without any notice within the limits of the fund's prospectus.

The mentioned financial instruments are provided for illustrative purposes only and shall not be considered as a direct offering, investment recommendation or investment advice. Reference to a specific security is not a recommendation to buy or sell that security. Effective allocations are subject to change and may have changed since the date of the marketing material.

Past performance is not a guarantee or a reliable indicator of future performance. Performance data does not include the commissions and fees charged at the time of subscribing for or redeeming shares.

Any index data referenced herein remains the property of the Data Vendor. Data Vendor Disclaimers are available on assetmanagement.pictet in the “Resources” section of the footer.

This document is a marketing communication issued by Pictet Asset Management and is not in scope for any MiFID II/MiFIR requirements specifically related to investment research. This material does not contain sufficient information to support an investment decision and it should not be relied upon by you in evaluating the merits of investing in any products or services offered or distributed by Pictet Asset Management.

Pictet AM has not acquired any rights or license to reproduce the trademarks, logos or images set out in this document except that it holds the rights to use any entity of the Pictet group trademarks. For illustrative purposes only.

Cookie Policy

This website uses cookies to enhance user navigation and to collect statistical data. To refuse the use of cookies, change your settings or for more information, please click on the following link: Cookies policy. By continuing to browse this website, you accept the use of cookies for the above purposes.