Innovative and flexible, sustainability linked bonds could catapult responsible fixed income into the mainstream.

Written by

Philipp Buff

Senior Investment Manager

Stéphane Rüegg

Head of Product Management and Development

Share this article

Responsible investment is making its presence felt in bond markets. Not before time.

Equity investors first embraced environmental, social and governance (ESG) principles with

dedicated strategies and investor engagement several years ago. But, after a few false starts, fixed income is

fast catching up. The amount of outstanding ESG-labelled bonds now tops USD 1 trillion. That figure is sure to rise. One reason is the arrival of an innovate new instrument, the sustainability linked bond. These securities offer investors a new way of engaging with

companies on the issues that matter the most to them and have the potential to

become the default form of ESG fixed income investment. In time they may even take

over from traditional instruments as the standard form of credit.

Sustainability linked bonds

should not be confused with green bonds, which are issued with a pledge to use the

proceeds for specific environmentally-friendly projects. By contrast, companies

issuing sustainability linked bonds pledge to meet specific, firm-wide

objectives in a pre-defined timeframe. That gives investors the opportunity to

pick issuers whose overall sustainability priorities align with their own.

It also affords issuers great flexibility to find a target that suits them –

regardless of their size, credit rating, sector or region.

The specificity of the

objectives is important. Many investors are skeptical of green bonds because it

has been difficult to gauge whether the money raised is genuinely channeled to

environmental projects. Sustainability linked bonds overcome this problem as

they embed a strong incentive for issuing companies to embrace more sustainable practices. That

incentive comes in the form of a “penalty” feature – such as coupon step-ups or an additional payment to investors at maturity – that kicks in whenever performance targets are not met.

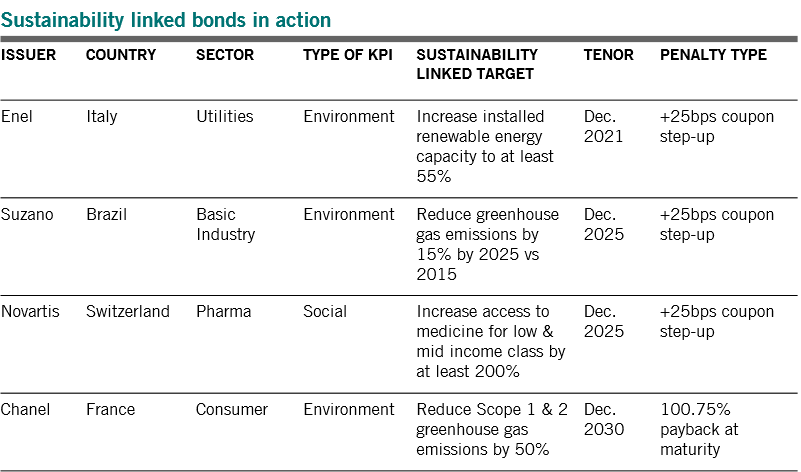

Across industries and ratings

Enel, an Italian

utility company, was the first to issue a sustainability linked bond in 2019. A

few others have followed suit, including Brazilian pulp and paper company

Suzano, Swiss pharmaceutical major Novartis and French luxury house Chanel.

Fig. 1 - Taking the lead

Examples of sustainability linked issues to-date (a selection)

Source: Pictet Asset Management

As there is no pre-requisite for a big, expensive environmental project, there is scope for smaller companies, including ones in the high yield sector, to join in, further

broadening investment options. Given the large number of fallen angels this year – companies that have recently lost their investment-grade ratings – we can expect sustainability-linked bonds to be concentrated within the BB

rating segment, which currently represents close to 75 per cent of the European high

yield market.

We also expect

financial institutions to embrace these instruments, linking ESG targets to the composition of their loan books.

There are grounds to

believe that the wide range of potential sustainability-linked goals will

help this instrument to gain popularity across all industries – in contrast to

green bonds, which have so far largely been the domain of utilities. Retail is

among the sectors that could be a rich source of sustainability linked bonds in the next few years.

Crucially,

it’s not just about the environment. While the first sustainability linked bonds have been tied to

environmental targets, such as reductions in greenhouse gas emissions, pharmaceutical company Novartis

has opted to focus on access to medicine in the middle and low income segments.

This reflects their specific industry and strategy, and demonstrates the potential for such bonds to include tailored targets across full spectrum of ESG issues. Over time, we would

expect to see more social and governance-focused targets alongside

environmental ones – which would further differentiate sustainability linked bonds from their green counterparts.

Diligence pays off

There is a trade-off to investing in these new securities however. They require greater scrutiny and due diligence.

Are the targets sensible, achievable and measurable? Are they truly aligned with ESG principles? Do the yields on offer accurately reflect the risks of the issuer? Are the penalties sufficiently high to act as an incentive for change, while still being fair?

At present, a 25bps step-up in the coupon seems to be the most popular penalty. But this is low compared to a bond's initial coupon. Ideally, the penalty would be similar to the step-ups that kick in when issuers' credit ratings are downgraded – 125bps or so. In other words, a sustainability performance target should be as important as a credit rating target. A first step of breaking the 25bps trend has been taken by Chanel.

Demand for sustainability linked bonds has been strong. Most new issues in 2020 have come to market at more expensive levels than similar bonds trading in the secondary market, demonstrating strong appetite among investors for this type of debt. Many of these bonds now trade at a “negative premium” versus standard bonds.

While investors need to be careful not to overpay, the pricing so far is indicative of the future role that sustainability linked bonds can play. We would expect their popularity to grow further thanks to the European Central Bank’s recent decision to include such paper in its asset purchase programmes and as collateral from January 2021. This is a significant move, particularly as ECB has previously excluded coupon step-up structures (ones triggered by ratings downgrade for instance). As eligibility is phased in, it should encourage further issuance in the coming months.

There are other factors likely to offer support.

By aligning company-specific targets to those in EU green taxonomy and/or the UN’s Sustainable Development Goals (SDGs), the market's growth could be even more rapid.

Bonds embedding SDGs 3, 7, 13 and 3 – which cover clean energy, climate action and good health and wellbeing – could proliferate, in our view.

There is also scope for bonds embedding other SDG targets, including clean water and sanitation, reduced inequality and responsible consumption and production.

Across asset classes, ESG investment is rapidly moving from a niche to “business as usual”. We believe sustainability linked bonds have a key part to play in this revolution. As the market grows, they will win a greater share not only in dedicated sustainable credit portfolios but also in ordinary bond portfolio holdings. For investors, this innovation brings the opportunity to align their own ESG priorities with those of the companies they invest in, to support measurable and concrete progress towards sustainability, as well as to tap into a growing opportunity set with the potential to generate attractive returns.

Philipp Buff is Head of Credit Research, Developed Credit Market since September 2017.

He has been a Credit Analyst since 2014 at Pictet Asset Management. In 2020, he took on the additional responsibility of co-portfolio management for our Global Sustainable Credit fund. Before joining Pictet, he was an analyst responsible for credit risk management and ratings advisory at Goldman Sachs in New York and Brazil. He started his career in 2006 as a risk analyst at Bear Stearns.

Philipp holds a BA in History and Political Science from Duke University in the U.S. and a MBA in Finance from FGV (Fundação Getúlio Vargas) in Brazil. He has also obtained a certificate in Finance from the University of Chicago.

About

Stéphane Rüegg

Stéphane Rüegg is Head of Product Management and Development. He joined Pictet Asset Management in 2013 as a Client Portfolio Manager in the Fixed Income team, covering European credit investment grade and high yield.

Before joining Pictet, he was a client portfolio manager with Amundi in Singapore and Paris. Stéphane started his career in 1999 as fixed income risk manager at Credit Agricole Indosuez. From 2004 to 2008 he was head of risk control of the global fixed income team at Amundi in London.

Stéphane holds a Master’s degree in Business Administration from Ecole supérieure de commerce de Paris and a master in political sciences from Institut d'études politiques de Paris.

Share this article

This marketing material is issued by Pictet Asset Management (Europe) S.A.. It is neither directed to, nor intended for distribution or use by, any person or entity who is a citizen or resident of, or domiciled or located in, any locality, state, country or jurisdiction where such distribution, publication, availability or use would be contrary to law or regulation. The latest version of the fund‘s prospectus, Pre-Contractual Template (PCT) when applicable, Key Investor Information Document (KIID), annual and semi-annual reports must be read before investing. They are available free of charge in English on www.assetmanagement.pictet or in paper copy at Pictet Asset Management (Europe) S.A., 15 avenue J.F. Kennedy, L-1855 Luxembourg, or at the office of the fund local agent, distributor or centralizing agent if any. The KIID is also available in the local language of each country where the compartment is registered. The prospectus, the PCT when applicable, and the annual and semi-annual reports may also be available in other languages, please refer to the website for other available languages.Only the latest version of these documents may be relied upon as the basis for investment decisions.

The summary of investor rights (in English and in the different languages of our website) is available here and at www.assetmanagement.pictet under the heading "Resources", at the bottom of the page.

The list of countries where the fund is registered can be obtained at all times from Pictet Asset Management (Europe) S.A., which may decide to terminate the arrangements made for the marketing of the fund or compartments of the fund in any given country.

The information and data presented in this document are not to be considered as an offer or solicitation to buy, sell or subscribe to any securities or financial instruments or services.

Information, opinions and estimates contained in this document reflect a judgment at the original date of publication and are subject to change without notice. Pictet Asset Management (Europe) S.A. has not taken any steps to ensure that the securities referred to in this document are suitable for any particular investor and this document is not to be relied upon in substitution for the exercise of independent judgment. Tax treatment depends on the individual circumstances of each investor and may be subject to change in the future. Before making any investment decision, investors are recommended to ascertain if this investment is suitable for them in light of their financial knowledge and experience, investment goals and financial situation, or to obtain specific advice from an industry professional.

The value and income of any of the securities or financial instruments mentioned in this document may fall as well as rise and, as a consequence, investors may receive back less than originally invested.

The investment guidelines are internal guidelines which are subject to change at any time and without any notice within the limits of the fund's prospectus.

The mentioned financial instruments are provided for illustrative purposes only and shall not be considered as a direct offering, investment recommendation or investment advice. Reference to a specific security is not a recommendation to buy or sell that security. Effective allocations are subject to change and may have changed since the date of the marketing material.

Past performance is not a guarantee or a reliable indicator of future performance. Performance data does not include the commissions and fees charged at the time of subscribing for or redeeming shares.

Any index data referenced herein remains the property of the Data Vendor. Data Vendor Disclaimers are available on assetmanagement.pictet in the “Resources” section of the footer.

This document is a marketing communication issued by Pictet Asset Management and is not in scope for any MiFID II/MiFIR requirements specifically related to investment research. This material does not contain sufficient information to support an investment decision and it should not be relied upon by you in evaluating the merits of investing in any products or services offered or distributed by Pictet Asset Management.

Pictet AM has not acquired any rights or license to reproduce the trademarks, logos or images set out in this document except that it holds the rights to use any entity of the Pictet group trademarks. For illustrative purposes only.

Cookie Policy

This website uses cookies to enhance user navigation and to collect statistical data. To refuse the use of cookies, change your settings or for more information, please click on the following link: Cookies policy. By continuing to browse this website, you accept the use of cookies for the above purposes.