Asset allocation: from Corona to conflict

Just as the Covid crisis has begun to fade, a conflict in Ukraine is erupting. The question investors now face is the degree to which Russia’s invasion will undermine the global economic recovery. The next few weeks will offer some clarity.

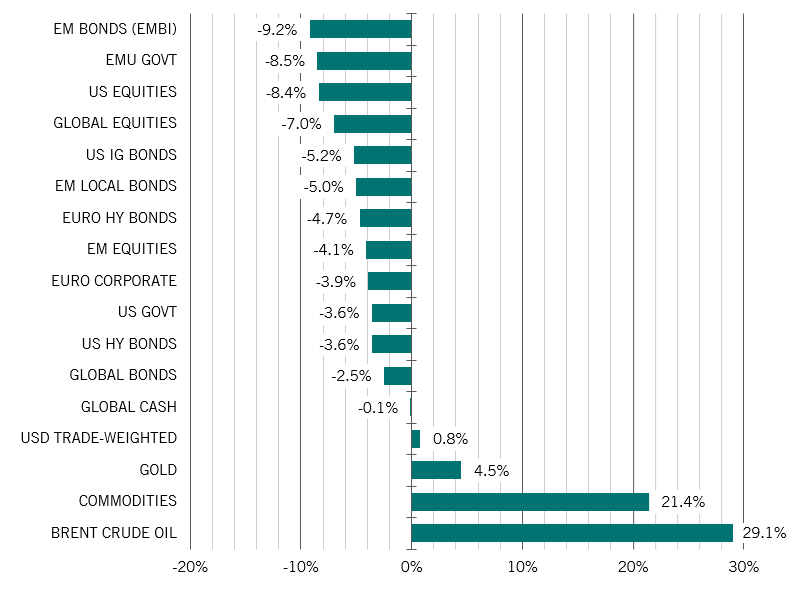

Even so, as long as Russia’s invasion doesn’t result in a drawn-out conflict, any consequences to global markets are likely to be manageable. Neither the Ukraine crisis nor the spike in oil prices is enough to derail what continues to be robust global growth.

Both countries make up only a small proportion of world GDP and, apart from Russian energy exports to Europe alongside some other commodities, have fairly modest roles to play in global trade. Some global industries will be potentially affected – apart from commodities: car manufacturers, food producers, steelmaking and chipmaking – but it is the second-round effects on European inflation and consumer confidence that need to be monitored.

The conflict might prove concerning enough to stay some of the more hawkish elements at the world's major central banks, not least the US Federal Reserve. So while the trend clearly remains towards monetary tightening, it could be at a slower pace than the markets have been pricing recently.

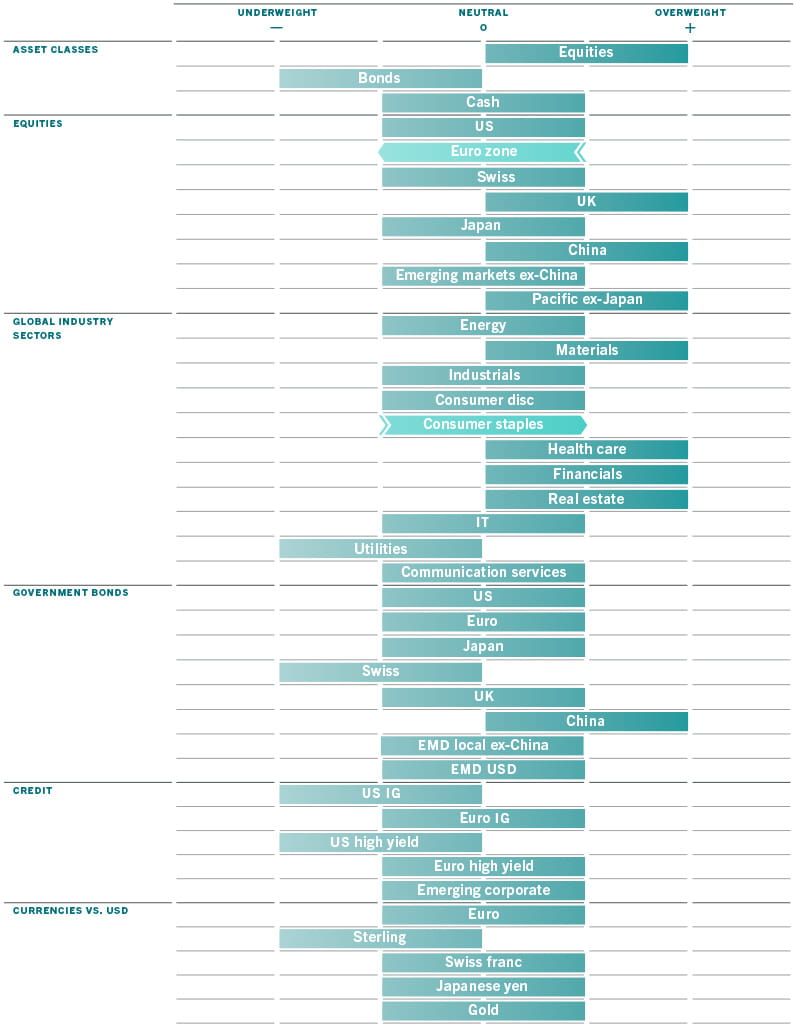

With all that in mind, in the very short term, it makes sense for investors to show some caution. Which is why we have taken a few risk mitigation measures within our equity positioning. But overall, our main asset allocations – overweight equities, underweight bonds - remain unchanged.

Our business cycle indicators point to a positive outlook for the global economy during the next year, with all major economies expected to grow at between 3 per cent and 5 per cent. World retail sales may have peaked, but they remain above trend. Industrial production and exports are accelerating. And services affected by Covid are poised to boom – not least travel and mass events.

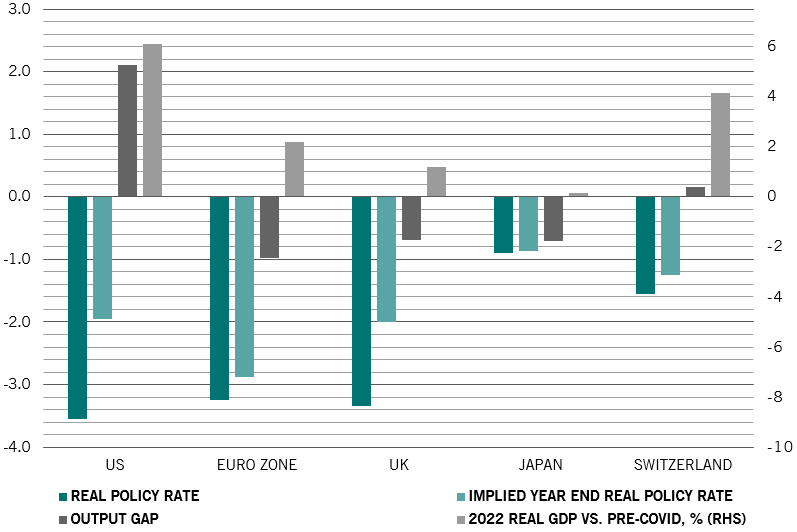

The US economy, which is least likely to be affected by Ukraine, shows strong underlying consumer demand and a resilient housing sector. Europe is vulnerable to its reliance on Russian gas, but the overall trend is towards recovery and monetary policy is likely to remain supportive. And China is starting to recover.

Meanwhile, even with the latest spike in oil prices, inflation should peak towards the end of the first quarter or early in the second across all major regions.

Our liquidity indicators offer mixed signals. Set against a the vast pool of global liquidity that has been built up during the Covid pandemic, central banks are starting not only to turn off the taps, but to drain some of the excess – we expect a net contraction of central bank liquidity this year to reach 3 per cent of global GDP. The Fed is poised to undertake a quadruple tightening – exiting quantitative easing, starting quantitative tightening and hiking rates even as inflation peaks and starts to slow. Offsetting this, however, is growth in the provision of credit from private sector banks. And central banks might find it prudent to talk down some of the markets’ excess hawkishness, particularly in light of global events.

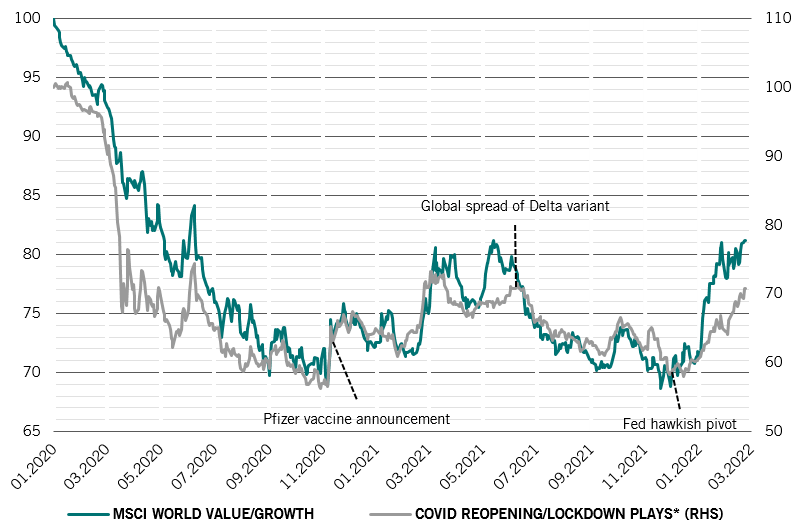

Our short-term valuation indicators show that both equities and bonds are trading at close to fair value, with only commodities looking expensive among the major asset classes. For the first time in a long time equity markets do not exhibit extreme relative valuation readings in either regions or sectors. The US remains the most expensive stock market, but only moderately so. The upward move in real rates was behind the recent outperformance of value stocks over growth – future earnings are worth less today as rates head higher – but that trade might be running its course. And while there may be further downward pressure on price to earnings (P/E) ratios, a 20 per cent decline in 12 month P/Es since September 2020 suggests there’s limited scope for further contraction in stocks' earnings multiples for the rest of this year – so, for instance, our model suggests P/E ratios will stabilise over the coming year (see Fig. 2).

Our technical indicators suggest that equities are oversold – particularly after the Ukraine-inspired drops. But there are no real signs of market panic. US equity sentiment is particularly gloomy, a bearish shift that’s been confirmed by the latest Bank of America fund manager survey. To us, this indicates the scope for a further sharp decline in US stocks is limited.