Asset allocation: steadying economy but virus threat lingers

It’s looking increasingly like a V-shaped economic recovery. True, in some regions the bounce back has been a little less robust. But in others, notably China, economic conditions are largely back to where they were pre-Covid – in July, industrial profits were up 20 per cent year on year. Meanwhile, after reviewing its approach to monetary policy, the US Federal Reserve has formally become a much more dovish institution at the margin, though it stopped short of a radical overhaul anticipated by some in the market.

Markets have noticed. Yet after a powerful rally across all assets during the past few months – sending leading US stock market indices to record highs – we feel that prospects for further broad-based gains are limited, with greater divergence among regional markets.

So while governments may yet offer more fiscal stimulus, not least in the US, liquidity provision is slowing worldwide. There are also political risks associated with US elections in November. And all the while there’s Covid-19. Not only is there the possibility of a significant second wave of the virus, but there is also little clarity on how soon a vaccine might be developed. At the same time, Shinzo Abe’s decision to step down after being Japan’s longest-serving prime minister introduces some uncertainty around geopolitics and the possibility that the world’s third largest economy will change its policy approach.

As a result, we remain neutral on all the major asset classes, though within equities we favour more cyclical sectors.

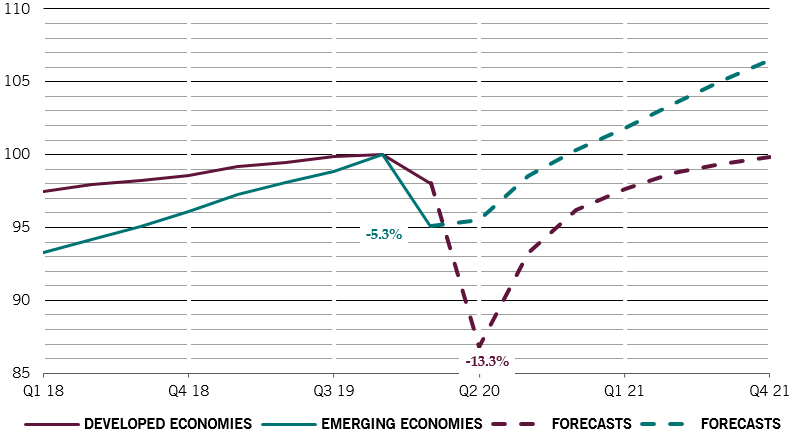

Our business cycle indicators show that the economic recovery is proving to be strong enough to warrant an upgrade to our 2020 economic forecasts. Our economists now expect full year global GDP to come in at -4 per cent from -4.2 per cent previously, but next year’s forecast has been cut to 6.1 per cent from 6.4 per cent.

In the US, retail sales have registered the strongest and fastest ever rebound after the deepest and quickest downturn in history to where they’re now – running at above pre-recession peak. Most past cycles have taken at least three years to play themselves out. This time, it’s been only a little more than three months. Retail sales are also back to trend in the euro zone.

However, it’s notable that only China’s real-time indicators are back to pre-Covid levels. Elsewhere, they’ve flattened out at between 10 per cent and 20 per cent below.

And while inflation could yet prove to be a risk if demand remains firm and supply fails to catch up, that’s not likely to be an issue until the back half of 2021.

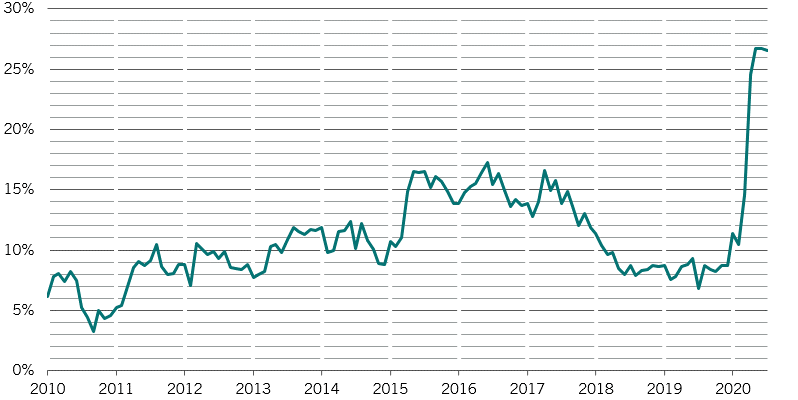

Global liquidity conditions remain very supportive, with new liquidity creation running at 25 per cent of GDP, but there is clear evidence that monetary stimulus growth has peaked [see Fig. 2]. At the same time, banks are tightening credit standards. And the Chinese central bank is now at neutral, while the country’s credit surge has tapered back down.

One upside liquidity risk, though, is that US Treasury cash balances held by the central bank could be drawn down.

Our sentiment indicators paint a mixed picture. The balance of equity calls to puts suggests a degree of market complacency, and our indicators show hedge funds have crowded into a handful of concentrated positions, particularly in the largest of the large cap stocks. On the other hand, retail investors seem cautious about shares and sentiment surveys remain depressed, while fund manager positioning in the asset class is below historic trend. A “wall of cash” remains, with some recently flowing into bonds and credit – both appear overbought.

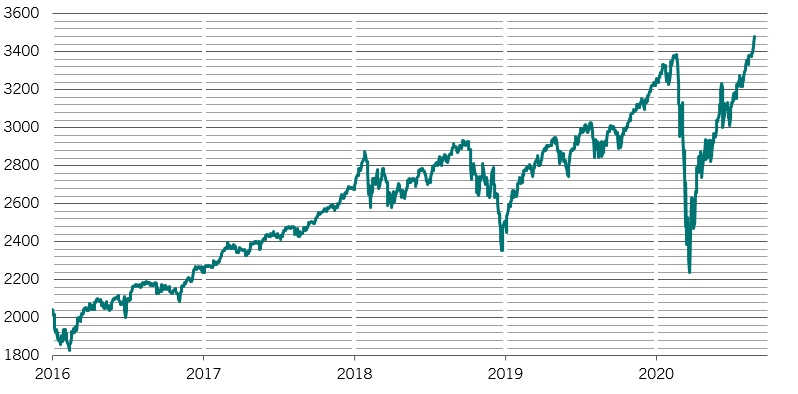

Finally, our valuation indicators suggest equity prices look stretched after a 50 per cent rally in the S&P 500 – on our models, they are at their most expensive in 12 years, trading two standard deviations above their 6-month moving average. Even relative to bonds, equity valuations no longer look particularly cheap. The gap between the global earnings yield and global bond yield is at its lowest in a decade at 4.5 percentage points. But we’re not yet into bubble territory. If current low bond yields, which have fallen 100 basis points this year, are sustained, this valuation impact on US equities exactly offsets the 20 per cent decline in earnings. Our valuation score on equities has moved from negative in January, to strongly positive in March and is back down to negative now.