Pre-Covid some emerging markets were facing growth and fiscal issues. Which countries' debt levels put them most at risk today?

Written by

Sabrina Khanniche

Senior Economist

Mary-Therese Barton

Chief Investment Officer Fixed Income

Share this article

By Sabrina Khanniche, Senior Economist

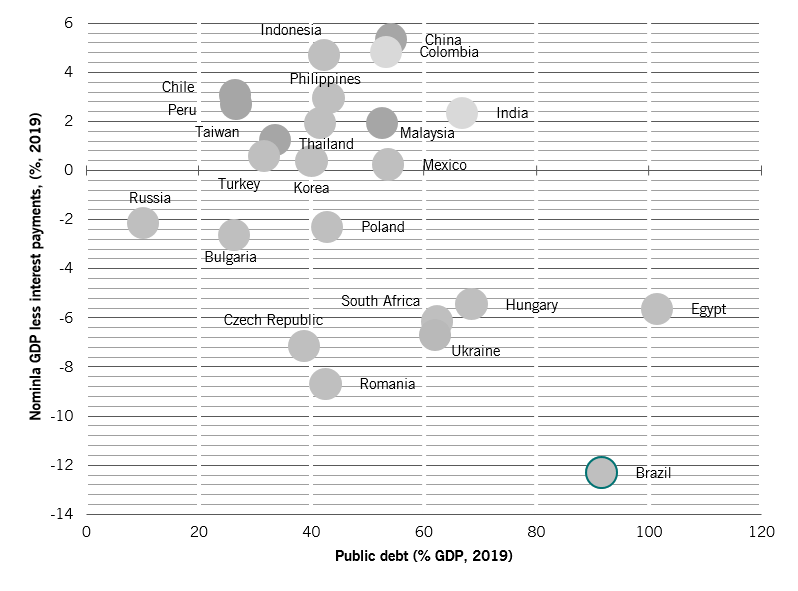

Pre-pandemic, vulnerabilities in some EM economies had mounted amid slowing economic growth. As Fig. 1 shows, countries in the bottom right (Brazil, Egypt, Ukraine, South Africa) had limited fiscal space going into the health crisis as they already had high public-debt-to-GDP ratios.

Fiscal space pre-Covid

Fig. 1: Nominal GDP less interest payments (%, 2019) versus public debt (% GDP 2019)

Since the onset of the current crisis we have seen a surge in debt ratios as recession hit. For the moment there is a tolerance in markets towards higher fiscal deficits and public debt (that we closely monitor), but actions to restore fiscal sustainability will be required once the recovery gets underway.

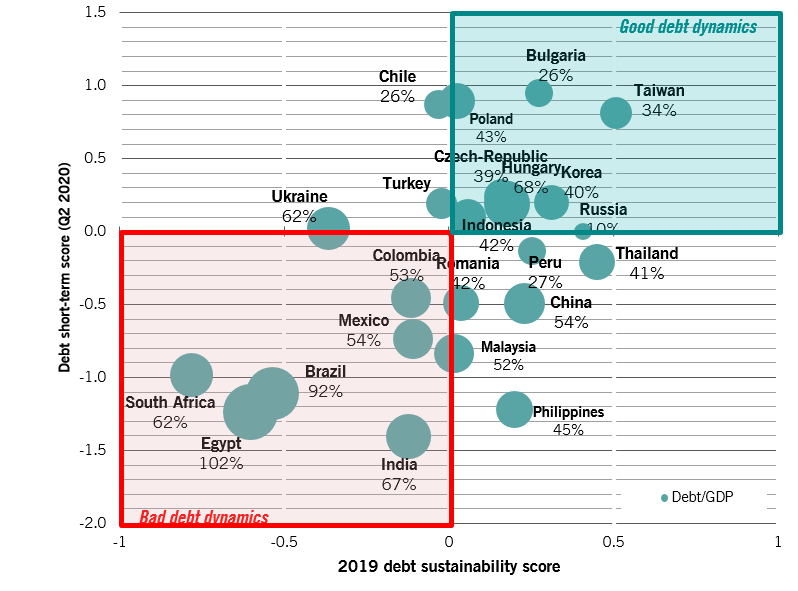

Tracking debt sustainability

Our proprietary ‘Debt Sustainability Score’ looks for a potential negative drift in government indebtedness before it becomes irreversible, using a range of tested inputs. Our ‘Shorter-Term Debt Score’ model detects shorter-term momentum shifts based on quarterly inputs. In fig. 2 below we combine the latest readings of both models.

This chart shows us two things. First it identifies countries with good debt dynamics in the green quadrant: Taiwan particularly and Eastern Europe, especially Bulgaria. Conversely the red quadrant shows us less favourable markets: foremost Brazil (of which more from our EM debt team below), South Africa and Egypt.

Second it flags markets which are seeing short-term shifts that might point to improvements or deteriorations in their longer-term debt sustainability score.

Improving on the margin are Chile and Turkey.

Meanwhile a range of markets are seeing short-term deteriorations with possible long-term consequences: foremost the Philippines, but also Malaysia, China and Romania.

A VIEW FROM OUR EM DEBT TEAM ON BRAZIL

By Mary-Therese Barton, Head of Emerging Market Debt

Brazil has been one of the worst affected countries during the Covid-19 crisis, with a large number of virus cases, significant restrictions and economic disruption.

The fiscal and monetary policy response has been timely and very powerful – involving large social transfers and a significant widening in fiscal balances as well as monetary policy easing and liquidity provision.

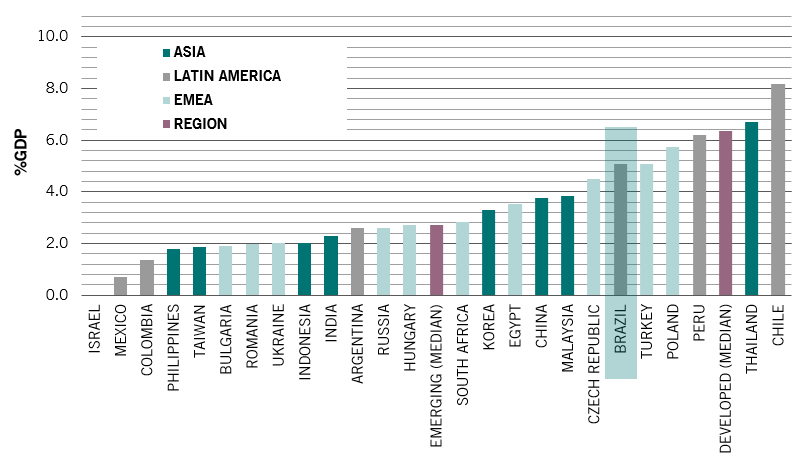

The large fiscal impulse in Brazil presented below, during a time of mounting debt to GDP, has unsettled market participants. Very low interest rates have also weighed on the currency, further exacerbated by a difficult environment for EM FX globally.

Fiscal stimulus in Brazil has been sizeable compared to EM average.

Fig 3. Emerging markets fiscal impulse by country (% of 2020 GDP)

Source: Pictet Asset Management, CEIC, Refinitiv

More recently however, it is becoming clear that the Brazilian real (BRL) has become an increasingly domestic/idiosyncratic story, heavily centered around the outlook for fiscal policy. While we expect the external environment to improve, through a gradual although somewhat uneven global recovery and the prospect of a vaccine in 2021, we believe that BRL will continue to be dominated by domestic fiscal news flow and policy coordination.

The way forward...

In particular, we believe that Brazil needs to set out clear policies for maintaining the fiscal spending ceiling by allowing a gradual expiry of temporary fiscal measures, identifying spending cuts and pushing ahead with a more ambitious reform agenda. Should such a scenario materialize, likely over the next few months, we believe the risk premium specific to Brazil can be priced out from the currency, allowing the BRL to strengthen.

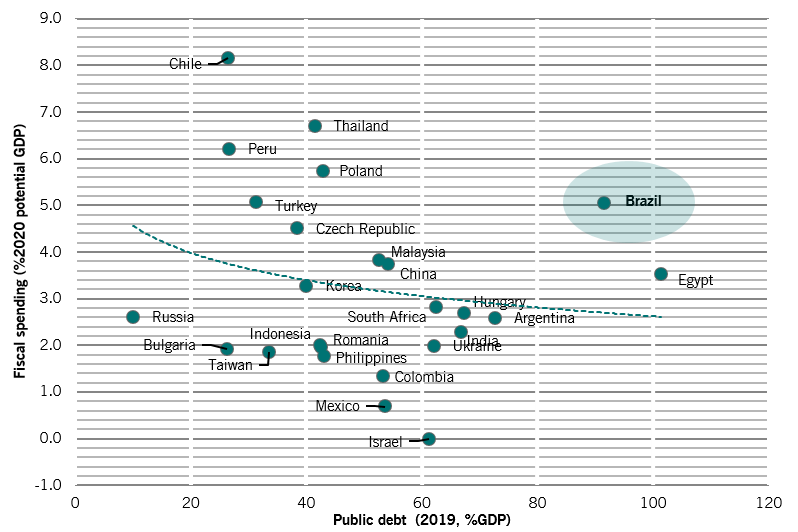

Hey big spender...

Fig. 4: Emerging market fiscal spending vs public debt

Source: Pictet Asset Management, CEIC, Refinitiv

Restoring fiscal credibility in Brazil together with an improving growth/virus picture, strong commodities backdrop and a positive external balance picture should translate into a reversal of this year's significant underperformance. Of course, if there is evidence that the spending cap is not being respected it could mean further currency weakness, as the debt sustainability issue becomes the dominant driver of Brazilian assets.

Sabrina Khanniche joined Pictet Asset Management in 2011. She is a Senior Economist, Lead on Eurozone and MEA.

Before joining Pictet, she was with Groupama Asset Management during four years as a Financial Engineer in charge of the analysis and modelling of hedge fund risks. In this regard, she published and presented her work in international academic conferences.

Sabrina holds a Master and a PhD in Economics from the University of Paris West Nanterre La Défense.

About

Mary-Therese Barton

Mary-Therese Barton was appointed Chief Investment Officer - Fixed Income in October 2023. She was previously Head of Emerging Market Fixed Income, overseeing the Emerging Market Sovereign, Corporate and Greater China debt strategies. She joined Pictet Asset Management in 2004.

Prior to joining Pictet she worked at Dun & Bradstreet, where she was an economist responsible for analysing European countries.

Mary-Therese graduated with a BA (Hons) in Philosophy, Politics and Economics from Balliol College, Oxford. She also holds an MSc with distinction in Development Finance from the Centre for Financial Management Studies, SOAS (School of Oriental and African Studies), part of the University of London. Mary-Therese is also a Chartered Financial Analyst (CFA) charterholder.

Share this article

Important legal information

This marketing material is issued by Pictet Asset Management (Europe) S.A.. It is neither directed to, nor intended for distribution or use by, any person or entity who is a citizen or resident of, or domiciled or located in, any locality, state, country or jurisdiction where such distribution, publication, availability or use would be contrary to law or regulation. The latest version of the fund‘s prospectus, Pre-Contractual Template (PCT) when applicable, Key Information Document (KID), annual and semi-annual reports must be read before investing. They are available free of charge in English on www.assetmanagement.pictet or in paper copy at Pictet Asset Management (Europe) S.A., 6B, rue du Fort Niedergruenewald, L-2226 Luxembourg, or at the office of the fund local agent, distributor or centralizing agent if any.

The KID is also available in the local language of each country where the compartment is registered. The prospectus, the PCT when applicable, and the annual and semi-annual reports may also be available in other languages, please refer to the website for other available languages. Only the latest version of these documents may be relied upon as the basis for investment decisions.

The summary of investor rights (in English and in the different languages of our website) is available here and at www.assetmanagement.pictet under the heading "Resources", at the bottom of the page.

The list of countries where the fund is registered can be obtained at all times from Pictet Asset Management (Europe) S.A., which may decide to terminate the arrangements made for the marketing of the fund or compartments of the fund in any given country.

The information and data presented in this document are not to be considered as an offer or solicitation to buy, sell or subscribe to any securities or financial instruments or services.

Information, opinions and estimates contained in this document reflect a judgment at the original date of publication and are subject to change without notice. The management company has not taken any steps to ensure that the securities referred to in this document are suitable for any particular investor and this document is not to be relied upon in substitution for the exercise of independent judgment. Tax treatment depends on the individual circumstances of each investor and may be subject to change in the future. Before making any investment decision, investors are recommended to ascertain if this investment is suitable for them in light of their financial knowledge and experience, investment goals and financial situation, or to obtain specific advice from an industry professional.

The value and income of any of the securities or financial instruments mentioned in this document may fall as well as rise and, as a consequence, investors may receive back less than originally invested.

The investment guidelines are internal guidelines which are subject to change at any time and without any notice within the limits of the fund's prospectus.

The mentioned financial instruments are provided for illustrative purposes only and shall not be considered as a direct offering, investment recommendation or investment advice. Reference to a specific security is not a recommendation to buy or sell that security. Effective allocations are subject to change and may have changed since the date of the marketing material.

Past performance is not a guarantee or a reliable indicator of future performance. Performance data does not include the commissions and fees charged at the time of subscribing for or redeeming shares.

Any index data referenced herein remains the property of the Data Vendor. Data Vendor Disclaimers are available on assetmanagement.pictet in the “Resources” section of the footer.

This document is a marketing communication issued by Pictet Asset Management and is not in scope for any MiFID II/MiFIR requirements specifically related to investment research. This material does not contain sufficient information to support an investment decision and it should not be relied upon by you in evaluating the merits of investing in any products or services offered or distributed by Pictet Asset Management.

Pictet AM has not acquired any rights or license to reproduce the trademarks, logos or images set out in this document except that it holds the rights to use any entity of the Pictet group trademarks. For illustrative purposes only.

Cookie Policy

This website uses cookies to enhance user navigation and to collect statistical data. To refuse the use of cookies, change your settings or for more information, please click on the following link: Cookies policy. By continuing to browse this website, you accept the use of cookies for the above purposes.