Infrastructure assets for institutional investors

Upgrading infrastructure can boost an economy’s productivity.

Investing in it is equally worthwhile.

As investments, real assets such as power grids and hydroelectric plants tend to provide stable, inflation-protected cashflows. They can also deliver returns that are uncorrelated with those of equities and bonds.

This is why institutional investors with long-term liabilities - pension funds and life insurance companies - have been allocating capital to infrastructure for decades. Over the years, they have accumulated more than USD1 trillion in infrastructure investments, according to the OECD.

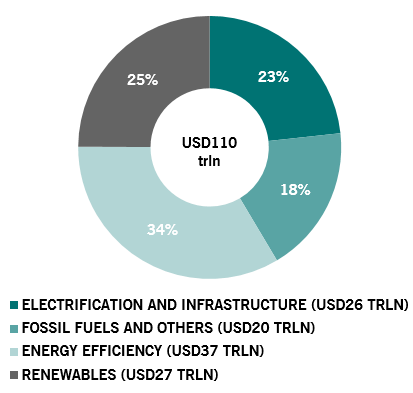

Infrastructure's appeal among this group of investors is likely to grow even stronger in the coming decade. Especially in clean energy.

With the US, Europe and China about to spend trillions of dollars to deliver a green recovery, a wide range of renewable and sustainable assets are poised for rapid growth, including wind and solar power plants, renewable electricity networks, electric vehicle infrastructure and environmentally friendly building. In time, they will make up the lion's share of new infrastructure assets.

Investors are alert to such trends. In a recent survey, more than 80 per cent of institutional investors said they expected the clean energy sector to be the primary source of infrastructure investments over the next 10 years.1

What investors might not realise, however, is that those opportunities won't be confined to the private markets. They are just as likely to come via listed stocks.

Infrastructure's investment appeal

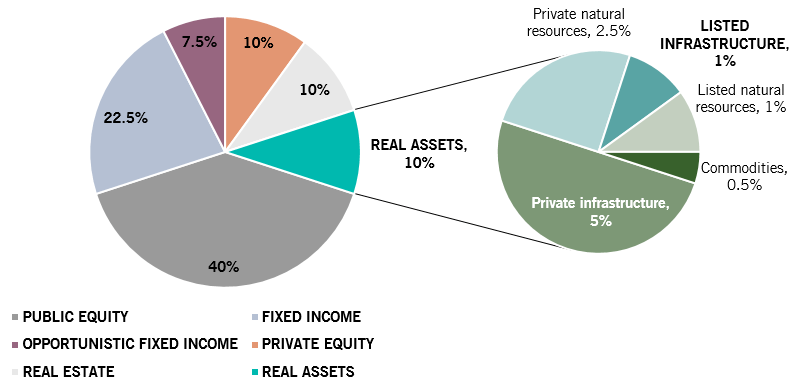

Broadly speaking, institutional investors allocate approximately 6 per cent of their portfolio investments to infrastructure.

Within that, private assets make up the bulk of such investments (see Fig. 1).

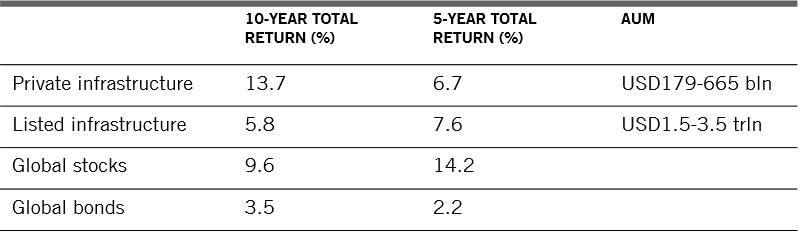

It has proved to be a wise move: unlisted infrastructure has delivered total returns of almost 14 per cent annualised over the past decade.2

While infrastructure investment has generally come in the direct form of private capital, there are good reasons to believe this might not be the default choice in future. In certain sectors, listed infrastructure – public companies that construct, manage and own real assets – are fast-emerging as a credible alternative to direct investment.

There are several reasons why.

To begin with, there’s a glaring imbalance in the supply of and demand for privately managed assets. In recent years, private infrastructure has become a crowded, and therefore, expensive asset class.

The availability of private and high-quality infrastructure investments has been limited – partly because of the time it takes to design, approve and procure big-scale projects.

Illustrating this, US total public spending on infrastructure was just 2.3 per cent of GDP in 2017, below the average since 1980s of around 2.5 per cent.3

This, in turn, has led to a surge in real assets’ valuations.

Since 2000, valuations for private infrastructure have risen eightfold. That rise eclipses that of listed equities, whose valuations have doubled over the same period.4 All of which dampens real assets’ prospective returns.

This presents institutional investors with a dilemma.

While their appetite for infrastructure is undiminished – some 54 per cent of investors polled by consultancy Preqin plan to commit more to infrastructure in the next 12 months than they did last year – reasonably priced options are limited.

Into the breach comes listed infrastructure, where investment returns have in any case been catching up with those of private investments in the past five years (see Fig.2).

Private and listed infrastructure comparison

Listed infrastructure offers several other advantages over more direct forms of investment.

Diversified, liquid, flexible. Compared with direct forms of investment, listed infrastructure companies operate across a range industries, which contain dozens of equity subsectors.5 This gives investors the opportunity to build a more diversified infrastructure portfolio. The public route also affords greater flexibility. Because stocks are liquid investments, investors can easily re-deploy capital in response to economic, regulatory and financial developments that cause changes in asset valuations. This is in contrast to direct investment, where capital tends be locked up for a number of years.

Frequent performance monitoring. Publicly-traded companies are required to post quarterly updates on their sales, earnings and product offerings. Investors can monitor performance of their investments in public markets frequently, in contrast to unlisted firms where certain performance reporting data may not suit institutional asset allocators.6

Better environmental, social and governance (ESG) profile. Listed companies tend to fare better on ESG metrics. Compared with private companies, listed firms are under greater public pressure to improve their performance on ESG. Their response can sometimes be very swift.

Take utility companies’ use of fossil fuels for instance. Since 2005, listed utilities have retired nearly 40 per cent of their coal fleets because of their environmentally damaging profile. This compares with only 20 per cent for private coal power plant owners.

Moreover, the private sector continues to allocate significant capital to coal projects. Nearly 90 per cent of new coal capacity planned in Europe is owned by private firms, while only about 10 per cent of the projects are owned by listed utilities.

While both listed and private utilities continue to operate coal power plants, listed utilities have earmarked around 60 per cent of their remaining fleet for retirement or a switch to emission-reducing fuel. The comparable proportion for private operators is at least 20 percentage points lower.7