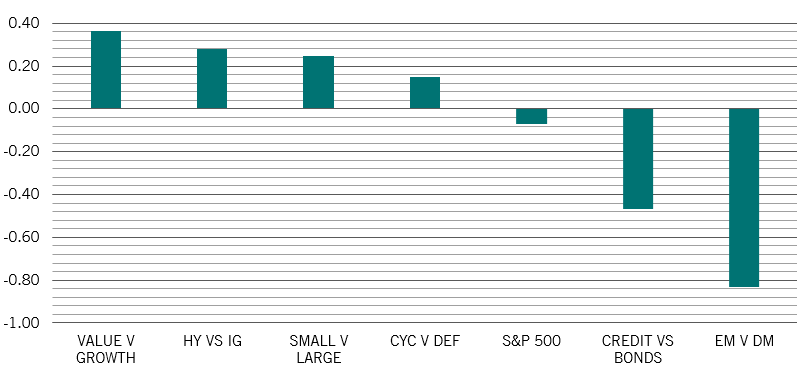

Asset allocation: recovery underpins cyclical tilt

The global economy is enjoying a strong bounce.

Ample monetary and fiscal stimulus and hopes that the Covid vaccine rollout will accelerate worldwide are encouraging investors to allocate more of their assets into stocks at the expense of bonds.

We don’t expect this pattern to change in the near term, and therefore retain our overweight stance on equities.

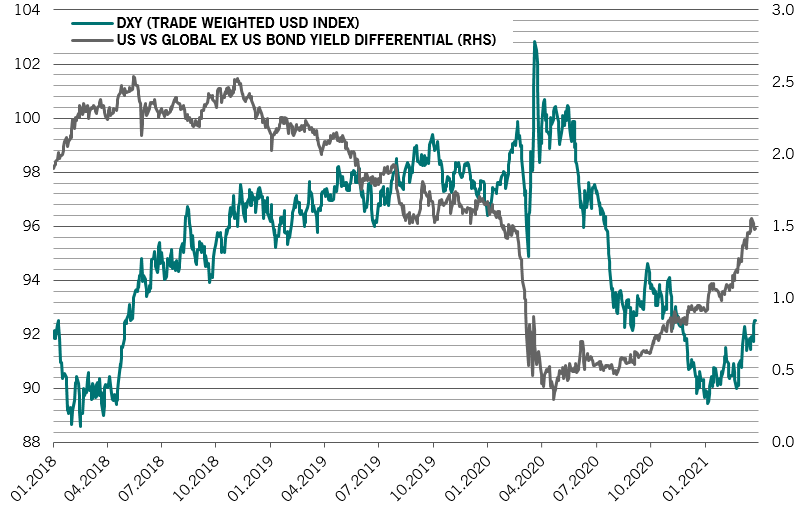

However, we recognise that, as the economic recovery is picking up pace in developed economies, an accompanying rise in both long-term interest rates and the US dollar are a threat to countries that have come to depend on cheap dollar funding.

For these reasons, we downgrade emerging equities to neutral. We also remain neutral bonds and underweight cash.

April

Source: Pictet Asset Management

Our business cycle indicators show the global economic recovery is accelerating, thanks to broad-based strength in the US.

American consumers, whose bank accounts are about to be boosted by federal payments of USD1,400, are starting to spend.

Government transfers to households have grown to USD3 trillion since January 2020, equal to a fifth of US personal consumption and three times the amount delivered during the global financial crisis in 2009.

US households’ net financial worth rose 10 per cent to a record USD130 trillion in the year to December 2020, before they received new stimulus checks from President Joe Biden’s USD1.9 trillion package.

A 10 per cent increase in net worth typically leads to a 1 per cent rise in personal consumption, which contributes nearly 70 per cent to economic output. Taking this into account, we expect the world’s biggest economy to grow by as much as 7 per cent in real terms this year, double the pace in 2020.

Strong economic conditions will put upward pressure on inflation, but price rises should be gradual.

We think price pressures for goods – the result of temporary factors such as higher commodities and supply bottlenecks - should ease in the coming months, helping offset higher service sector inflation later this year.

We don’t think a sustained pick-up in US inflation beyond the US Federal Reserve's 2.0 per cent target next year is likely unless tight labour market conditions trigger sharp wage increases.

Elsewhere, China’s economic recovery remains strong and self-sustaining. Non-manufacturing activity expanded for 11 months in a row in March, while export growth is 32 per cent above trend. The property market shows no signs of slowing down, underpinning demand for commodities.

We upgrade our 2021 real GDP growth forecast by 1 percentage point to 10.5 per cent.

The euro zone is lagging behind as a renewed wave of Covid infections forces countries to introduce restrictions on social and economic activity.

We expect the economy to recover in the second quarter, helped by improvements in the region’s vaccination programme. The region’s EUR2 trillion fiscal stimulus package, due to become available in the same period, will also offer some support.

Our liquidity conditions indicators show that central bank stimulus remains sufficient, but a few countries are beginning to tighten the monetary reins.

In China, which is responsible for at least a fifth of global liquidity supply, conditions are becoming restrictive, which could weigh on equity valuations later this year. The country’s excess liquidity -- the difference between the rate of increase in money supply and nominal GDP growth – has contracted on a year-on-year basis, while the credit impulse – or the flow of new credit from the private sector -- has fallen back to its two decade average after hitting its highest since 2009 in October.

In other emerging countries, a sharp rise in global bond yields and the dollar have exposed limits to easy monetary policy. Turkey, Brazil and Russia were already forced to withdraw policy support at a time when their economies are weak in order to defend their currencies and combat inflation.

In contrast, US liquidity conditions remain supportive of risky assets for now. Our calculations show effective US interest rates – adjusted for inflation and quantitative easing measures – stand at a record low of -4.7 per cent.

The Fed is keeping monetary conditions ultra loose despite a booming economy, which raises risks that the central bank will announce a move to scale back its monetary stimulus in the near future.

Our valuation signals are negative for risky assets, with global stocks hitting the most expensive level since 2008 on our models. Our technical readings are mildly positive for risky assets with equities drawing inflows of almost USD350 billion this year.

In contrast, emerging assets are suffering. According to the Institute of International Finance, a sharp rise in US long-term rates has triggered outflows of nearly USD500 million on a six-week moving average basis, levels last seen at the height of the 2013 “taper tantrum”.