EM Monitor - growth differential BETWEEN EMERGING and DEVELOPED MARKETS in 2021

January 2021

Marketing Material

Full steam ahead for emerging markets?

Five reasons why we believe the EM GDP growth differential with developed markets should widen in 2021

Written by

Patrick Zweifel

Chief Economist

Share this article

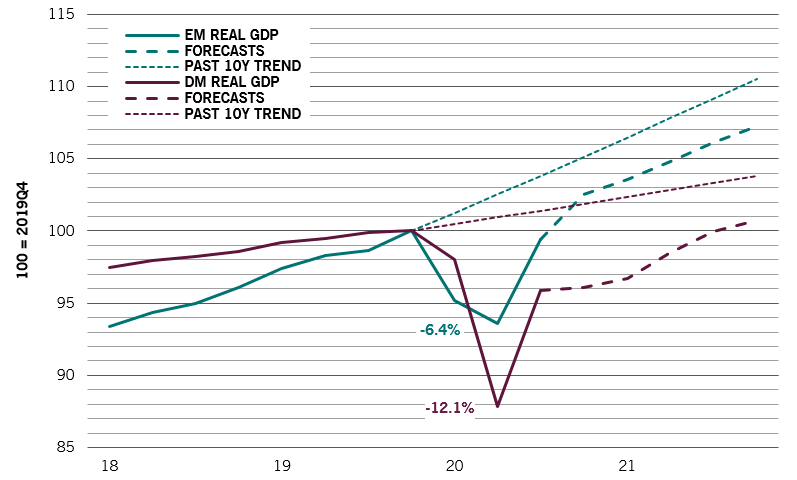

Widening growth differential

After contracting in 2020 – albeit far less than developed markets – we forecast real GDP growth in emerging markets to rise strongly in 2021, further widening the gap with developed markets. Growth will be led by the Asia ex Japan region (8.5 per cent), followed by EMEA (4.5 per cent) then Latin America (+3.6 per cent).

Widening growth differential

Fig. 1: GDP growth Emerging Markets vs Developed Markets

Source: Pictet Asset Management, CEIC, Refinitiv, January 2021

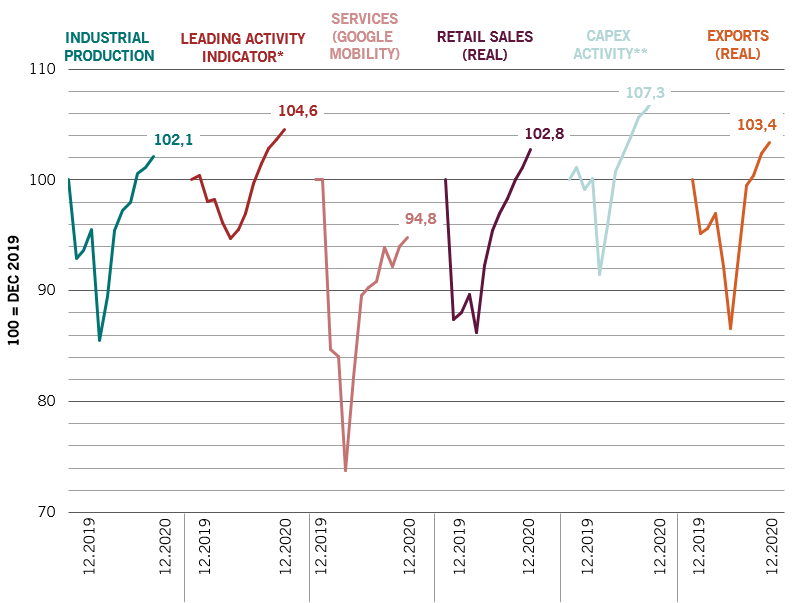

Main EM activity indicators have already rebounded above pre-Covid levels (see Fig.2 below) apart from 'services', which areless important for emerging economies than developed markets.

Back to rude health

Fig. 2: Emerging Markets main activity indicators

Source: Pictet Asset Management, CEIC, Refinitiv, CPB Netherlands, Google LLC, https://www.google.com/covid19/mobility/

*GDP-Weighted average of 39 countries leading indicator / **GDP-weighted average of countries new orders & capacity utilisation

This time, is it different?

What makes us think the timing is right for emerging markets? After all, emerging markets have endured a lost decade in terms of returns whilst the US economy, fueled by stimulus, has raced ahead. Many EM assets − equities, bond, currencies − appear very cheap today.

So why do we now think the timing is right?

Admittedly, we have had this view for a while, so why do we think the time is now right? Below are our five reasons why we think emerging markets might deliver.

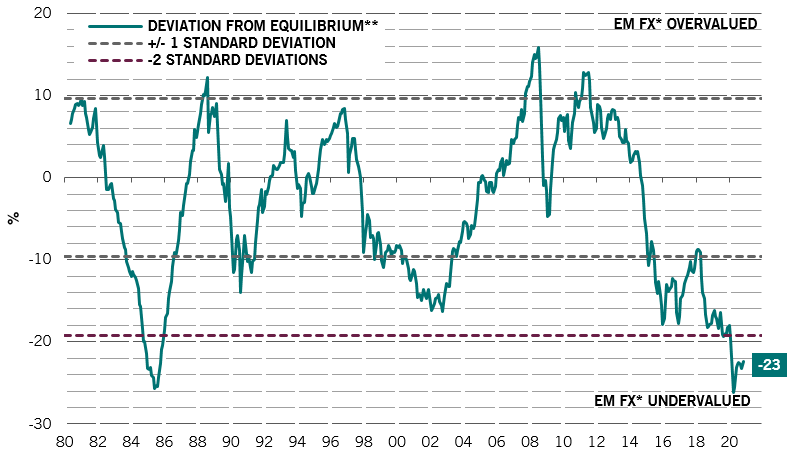

1. Weak US dollar and low US yields

EM currencies stand at historical lows against the dollar (see chart below). Our base case is the US dollar to weaken after years of strength, which will boost emerging markets, especially those with liabilities denominated in the US currency.

Can it go lower?

Fig.3: EM currencies valuation 1980-2020

Source: Pictet Asset Management, CEIC, Datastream. January 2021

*Unweighted 31 EM exchange rates vs USD **based on relative prices, relative productivities & net foreign assets

This consensus view of weaker US dollar could be derailed in two scenarios: if the global picture gets very bad, or if the US is doing better than the rest of the world.

First: we believe that globally we are through the worst, and emerging markets in particular. Vaccine deployment supports a constructive economic outlook, barring another exogenous black swan event.

The second scenario of the US outpacing global growth under the Biden administration is a possibility. Following the 2020 COVID relief package of $900bn, a second tranche of about US1tn is likely to be adopted in Q1. As a result we upgraded our forecast of US real GDP growth to 5.5 per cent for 2021. But this is still lower than our 6 per cent estimate for global growth.

Strong US growth could push US rates and the stronger dollar higher, which would affect the debt of most vulnerable EM countries. Yet, this risk remains contained since the Fed is committed to maintain rates low for long and EM imbalances are generally low with vulnerabilities in only two countries: Turkey & South Africa.

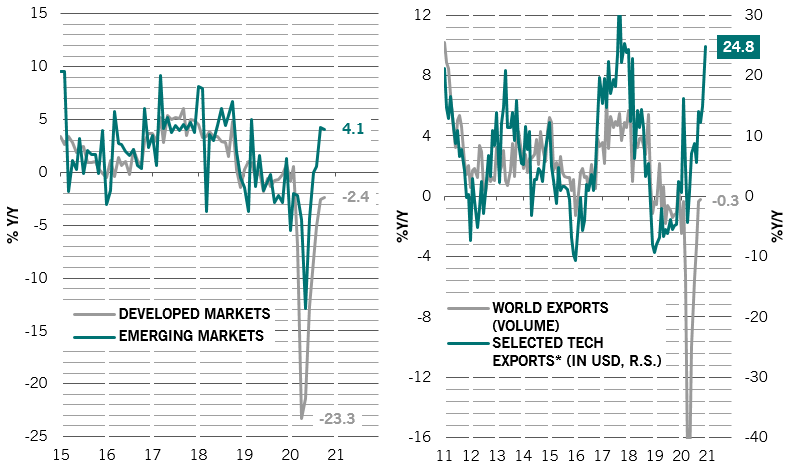

2. Global trade is looking strong again

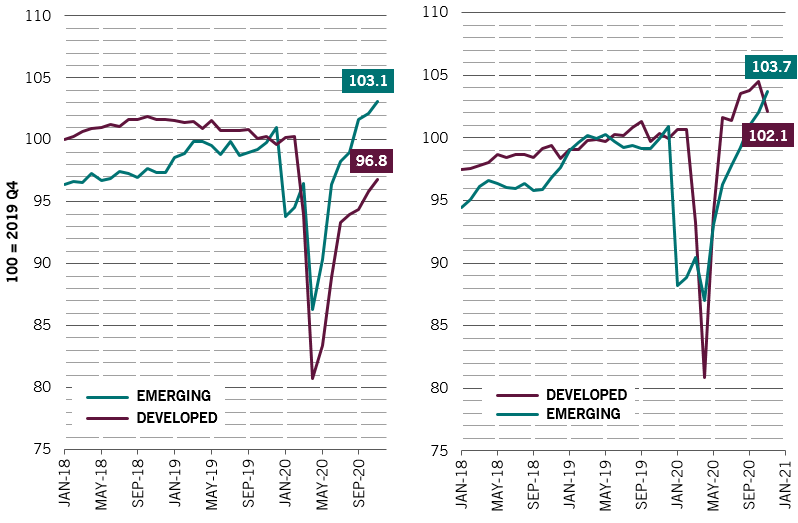

Emerging market industrial production has rebounded, whilst developed markets are still depressed as shown below left. We believe this has been driven in part by emerging markets meeting the demand for goods from locked-down developed markets where government payouts have supported retail consumption (see strong developed retail sales in right hand chart).

Global demand & supply recoveries in EM & DM

Fig. 4a: EM vs DM industrial production / Fig.4b: EM vs DM retail sales

Source: Pictet Asset Management, CEIC, Refinitiv, January 2021

Export growth is also on a positive trend (chart below left). Asian leadership in technology seems to be the driver (green line in right chart) and we believe this is a long-term structural trend. Moreover, since EM growth is two-times more sensitive to global trade than developed market, we expect the current synchronized recovery to be one of the main drivers of the widening growth gap between the two regions.

Asian technology leads the way

Fig. 5a (left): World real exports (%Y/Y) & export orders / Fig. 5b (right) : World real exports & selected Asian nominal tech exports (%Y/Y)

Source: Pictet Asset Management, CPB Netherlands, CEIC, Refinitiv, January 2021

3. China's continued strength

Another fundamental driver of EM outperformance is China’s ever greater role in terms of trade and financial linkages. All China's main activity indicators are above pre-pandemic levels driven by strong domestic and overseas demand. Consumption, which had been lagging, has gained momentum thanks to much better labour market conditions. Credit impulse remains expansionary. We expect real GDP growth to surge to 9.5 per cent in 2021 from 2.3 per cent in 2020.

We expect China's real GDP growth to surge to 9.5 per cent in 2021.

President Xi’s 14th five-year plan and 2035 long-term targets show that China’s ambition is to reach a “high income” status by 2025 and to double its real GDP per capita by 2035.

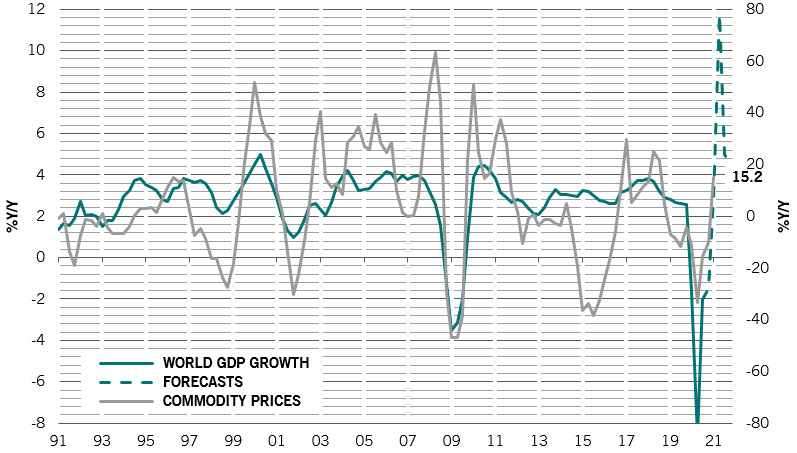

4. Commodity prices likely to remain in a positive trend

Strong commodity prices are another key element to support EM outperformance given many EM countries' dependence on exports (Latam, Russia, South Africa, Indonesia). Two key determinants of commodity prices are the US dollar and World GDP growth (a simple proxy for commodity demand). As outlined above we expect the USD to weaken, and for every 1 per cent decline in the dollar (vs US main trade partners), commodity prices rise by 2 per cent. We are also constructive on global GDP growth. As shown in Figure 6 above, commodity prices are already up by 15 per cent y/y, in line with the global demand recovery.

In sync...

Fig.6: World GDP growth (left axis) & commodity price growth (right axis)

Source: Pictet Asset Management, CPB Netherlands, CEIC, Refinitiv, January 2021

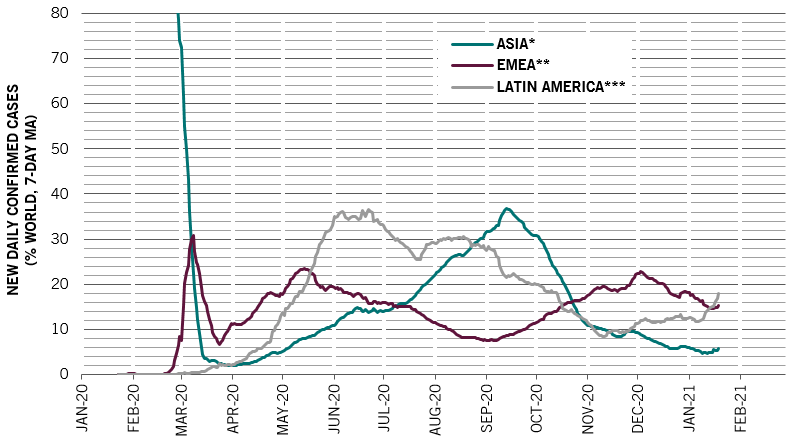

5. Asia is through the 2nd wave of Covid

Asia is the main engine of emerging markets growth and the region now seems past the second wave of Covid, despite a rising number of cases in Malaysia and Indonesia. The number of daily new confirmed cases in Asia represents (as of 19 January) just 5.7 per cent of global total, down from 36 per cent at the peak in October. This compares to 15 per cent for the EMEA region and 18 per cent for Latam.

Through the worst of it?

Fig. 7: Daily new confirmed COVID-19 cases in EM region (%world case)

Source: Pictet Asset Management, CEIC, Refinitiv, January 2021

*12 countries / **21 countries / ***9 countries

Risks to our bullish view:

The main risk to our bullish case for emerging markets is continued dollar strength. However other EM tail risks that cannot be discounted are the following:

Commodity prices plunge in case of new significant covid infections waves or/and lower than expected vaccines efficiency

Broad-based vaccines availability & effective mass immunity might be harder to achieve than anticipated

Medium and long-term inflationary risks stemming from large money printing & QE programs

Rising income inequality within EM and relative to DM and potentially more social unrest

About

Patrick Zweifel

Patrick Zweifel joined Pictet in 1997. He is Chief Economist at Pictet Asset Management, having assumed the position in 2009. Before that, he was head of the “Macro Research Team” at Pictet Private Wealth Management, where he was responsible for emerging markets and Japan, and for the development of quantitative models on major asset classes. Before joining Pictet he was a research assistant in econometrics and monetary theory and worked on international research projects for the World Bank and the European Union. He holds a PhD in Econometrics from the University of Lausanne.

This marketing material is issued by Pictet Asset Management (Europe) S.A.. It is neither directed to, nor intended for distribution or use by, any person or entity who is a citizen or resident of, or domiciled or located in, any locality, state, country or jurisdiction where such distribution, publication, availability or use would be contrary to law or regulation. The latest version of the fund‘s prospectus, Pre-Contractual Template (PCT) when applicable, Key Information Document (KID), annual and semi-annual reports must be read before investing. They are available free of charge in English on www.assetmanagement.pictet or in paper copy at Pictet Asset Management (Europe) S.A., 6B, rue du Fort Niedergruenewald, L-2226 Luxembourg, or at the office of the fund local agent, distributor or centralizing agent if any.

The KID is also available in the local language of each country where the compartment is registered. The prospectus, the PCT when applicable, and the annual and semi-annual reports may also be available in other languages, please refer to the website for other available languages. Only the latest version of these documents may be relied upon as the basis for investment decisions.

The summary of investor rights (in English and in the different languages of our website) is available here and at www.assetmanagement.pictet under the heading "Resources", at the bottom of the page.

The list of countries where the fund is registered can be obtained at all times from Pictet Asset Management (Europe) S.A., which may decide to terminate the arrangements made for the marketing of the fund or compartments of the fund in any given country.

The information and data presented in this document are not to be considered as an offer or solicitation to buy, sell or subscribe to any securities or financial instruments or services.

Information, opinions and estimates contained in this document reflect a judgment at the original date of publication and are subject to change without notice. The management company has not taken any steps to ensure that the securities referred to in this document are suitable for any particular investor and this document is not to be relied upon in substitution for the exercise of independent judgment. Tax treatment depends on the individual circumstances of each investor and may be subject to change in the future. Before making any investment decision, investors are recommended to ascertain if this investment is suitable for them in light of their financial knowledge and experience, investment goals and financial situation, or to obtain specific advice from an industry professional.

The value and income of any of the securities or financial instruments mentioned in this document may fall as well as rise and, as a consequence, investors may receive back less than originally invested.

The investment guidelines are internal guidelines which are subject to change at any time and without any notice within the limits of the fund's prospectus.

The mentioned financial instruments are provided for illustrative purposes only and shall not be considered as a direct offering, investment recommendation or investment advice. Reference to a specific security is not a recommendation to buy or sell that security. Effective allocations are subject to change and may have changed since the date of the marketing material.

Past performance is not a guarantee or a reliable indicator of future performance. Performance data does not include the commissions and fees charged at the time of subscribing for or redeeming shares.

Any index data referenced herein remains the property of the Data Vendor. Data Vendor Disclaimers are available on assetmanagement.pictet in the “Resources” section of the footer.

This document is a marketing communication issued by Pictet Asset Management and is not in scope for any MiFID II/MiFIR requirements specifically related to investment research. This material does not contain sufficient information to support an investment decision and it should not be relied upon by you in evaluating the merits of investing in any products or services offered or distributed by Pictet Asset Management.

Pictet AM has not acquired any rights or license to reproduce the trademarks, logos or images set out in this document except that it holds the rights to use any entity of the Pictet group trademarks. For illustrative purposes only.

Cookie Policy

This website uses cookies to enhance user navigation and to collect statistical data. To refuse the use of cookies, change your settings or for more information, please click on the following link: Cookies policy. By continuing to browse this website, you accept the use of cookies for the above purposes.