Green appetite

Governments everywhere are racing to lock in historically low borrowing costs by issuing ever longer dated debt – in recent years Mexico and Argentina even managed to sell century bonds. That presents several new challenges for fixed income investors. Particularly those who own emerging market bonds.

Not only do bondholders have to weigh the usual near-term factors like political, economic and commodity cycles but, in lending money to sovereigns over such extended periods, they now also have to consider the impact of longer term trends such as climate change and social development. Both can affect creditworthiness in profound ways.

This has called for new approaches to investment thinking. Economic and financial forecasts are having to be recast with climate dynamics in mind. Meanwhile, modelled pathways of climatic change are themselves subject to expectations about future technological change as well as the evolution of political thinking in these countries. The number of moving parts only grows as investors realise they also have a role to play in shaping how governments approach making their economies sustainable and low-carbon.

It’s a complex problem. But not an insurmountable one.

The greening of EM debt

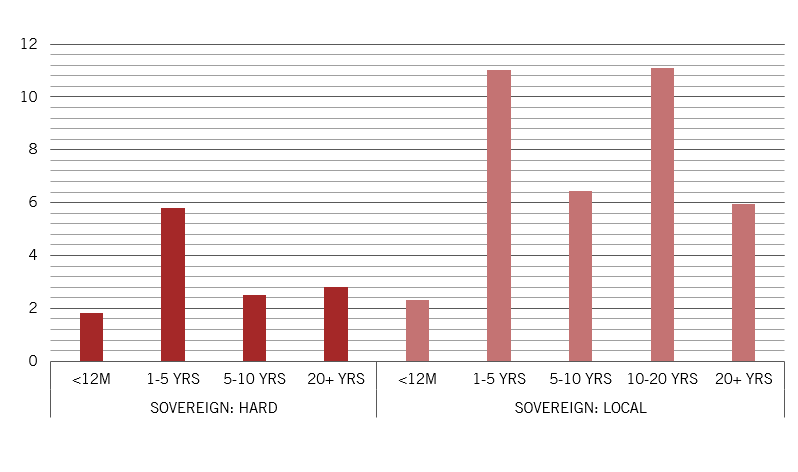

In 2015, some 17 per cent of emerging market hard currency debt had a maturity of 20 years or more. By the start of 2021, that proportion had grown to 27 per cent. Even local currency denominated emerging market debt, which tends to be shorter-dated, has moved along the maturity curve. Over the same time period, the proportion of local currency debt with a maturity of five years or longer had risen 11 percentage points to 58 per cent.1

That shift reflects growing demand for yield from investors starved of income. But at the same time, bondholders have recognised the importance of taking a long-term view on environmental issues. This is apparent in both the appetite for green bonds – capital earmarked for environmental- or climate-related projects – and, more generally, bonds that fall under the environmental, social and governance (ESG) umbrella.

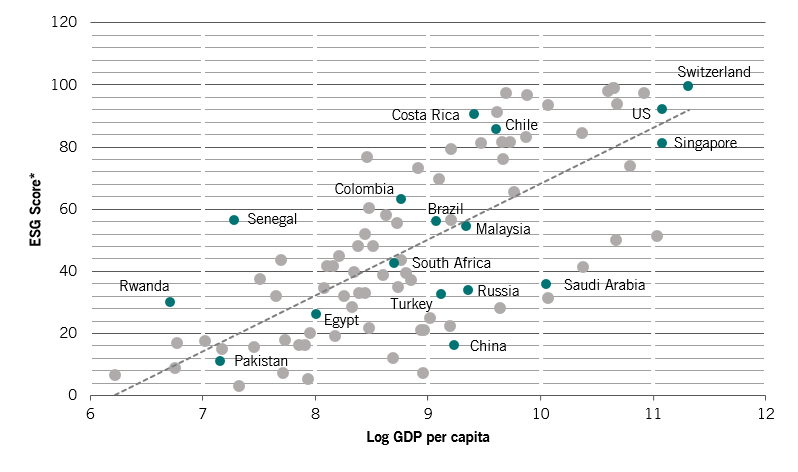

Governments are happy to meet that demand. Increasingly, they recognise the need to make efforts to mitigate climate change, and given that emerging market economies make up half the world’s output, they have a significant role to play in meeting global greenhouse gas emissions goals.

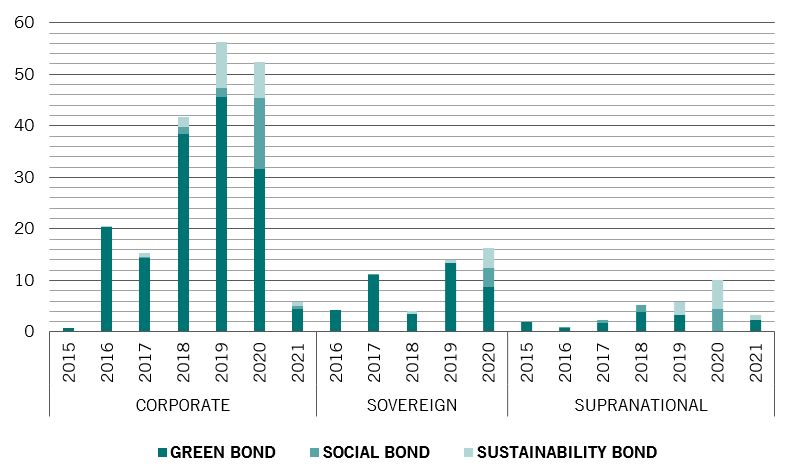

In the five years to the end of 2020, annual issuance of green, social and sustainability bonds by emerging market governments grew nearly four-fold to USD16.2 billion.2 And demand is only increasing. For instance, in the first few weeks of January, Chile met 70 per cent of its expected USD6 billion debt issuance for 2021, all in green and social bonds and it plans only to issue sustainable and green bonds during the remainder of the year.3 In September 2020, Egypt became the first Middle Eastern government to issue a green bond. It raised USD750 million to finance or refinance green projects. Investors were enthusiastic – the bond was five times oversubscribed.4

And generally, these bonds have longer maturities than conventional fixed income securities. Some 46 per cent of USD36.8 billion of outstanding emerging market ESG bonds priced in local currency terms have a maturity of more than 10 years, while for emerging markets hard currency ESG bonds, it’s 41 per cent of USD12.9 billion of outstanding bonds.5

These bonds allow investors to track performance, while green agendas can also help governments to improve their credit ratings, which then lifts the value of their debt, thus rewarding bond holders.

Overall, green bonds generate positive feedback effects. The rising volumes of green and sustainable bond issuance highlights investors' willingness to take more of a long-term approach to EM investing. But at the same time, governments are being made more accountable – in order to issue these bonds, governments are having to publish their sustainability frameworks in greater detail. This additional accountability helps to mitigate political risks that are a key consideration in EM investing. Investors, however, will need to analyse and monitor developments closely to ensure proceeds are used as intended.

Indeed, green bonds are the most exciting development in emerging market financing for decades and, we think, will have an equivalent impact to the Brady bonds of the 1980s6 – albeit this is dependent on improved disclosure and monitoring and industry standardisation of green labels.