How every aspect of the thematic portfolio construction process is geared to helping investors secure better returns from their equity investments.

Deel dit artikel

Why do we believe Pictet Asset Management’s Thematic Equity strategies have the potential to generate investment returns that are superior to mainstream stocks? There are a number of reasons.

Stock returns fuelled by powerful, long-term trends

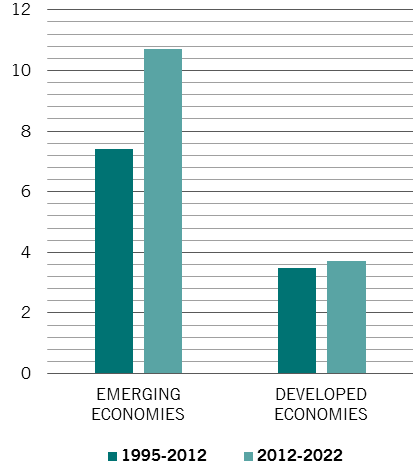

On the up: health spending rises worldwide

Rate of growth in health expenditure, %

Source: World Bank, Boston Consulting Group

The first is that returns from thematic equities stem from trends that are both long term in nature and largely unaffected by the ups and downs of the economic cycle.

In the health industry, for example, many companies have benefited from a persistent rise in health care spending worldwide. This is due to a major structural trend, the rise in life expectancy of the populations of the developed world. As Fig.1 shows, investment in health is rising at an accelerating pace, particularly in the emerging world. Experience shows this is unlikely to be derailed by any slowdown in the broader economy.

In the clean energy industry, meanwhile, the transformative power of climate change continues to drive investment in alternative sources of power. The technological advances that are emerging as a result of this wave of investment are helping slash the cost of renewable power. Production costs for onshore wind and solar power are expected to fall by 40 per cent and 60 per cent respectively by 2040.

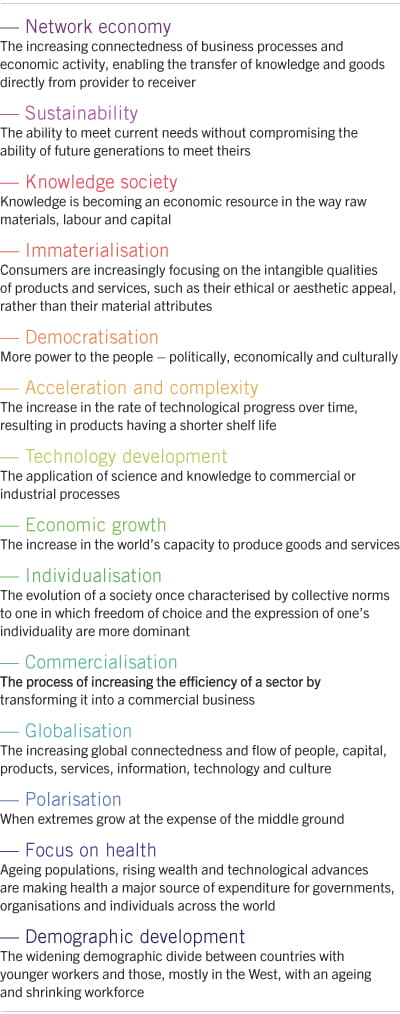

At Pictet Asset Management, we dedicate significant resources to the study of the non-economic megatrends that are reshaping the investment landscape. The 14 trends we have identified (see Fig. 2) form the basis of each of our thematic equity strategies.

Megatrends underpinning thematic equity strategies at pictet asset management

Source: Copenhagen Institute for Future Studies, Pictet Asset Management

Specialised companies better placed to deliver better returns

The second positive attribute that thematic stocks share is specialisation. The companies we invest in are attractive because they’re specialists in a particular field, not generalists whose activities span a broad range of industries or sectors.

And specialisation tends to be associated with higher returns.

There is a large body of evidence showing that the stocks of specialised firms do better than those of large, diversified companies over the long run. Essentially, large firms suffer from what is known as the “conglomerate discount”. Or, put another way, broadly diversified companies are worth less than the sum of their parts.

A study by the Boston Consulting Group (BCG) found that more complex the business, the more inefficient its investment. And, more importantly, the same study also established that wasteful investment acted as a drag on company stock prices.

By contrast, specialised firms – sometimes known as “pure play” companies – typically have a much clearer view of their strategic priorities and concentrate spending in areas that promise the strongest growth. Their capital allocation is more efficient which, in turn, builds a premium into their share prices over time, the BCG research found.

The companies we invest in are attractive because they're specialists in a particular field not generalists whose activities span a broad range of industries.

The upshot for investors is clear: a portfolio composed of the stocks of specialised companies – firms with three or fewer large divisions - should do better than a portfolio of diversified firms over the long run, other things being equal.

Our thematic strategies are designed to take advantage of this tendency. For each thematic strategy we manage, there are explicit rules for the construction of the portfolio. Each stock must have a high “thematic purity” for it to qualify as a potential thematic investment. Thematic purity is a proprietary, numerical indicator of how specialised a company’s activities are.

The higher the rating, the more specialised the firm. If, for example, a company within our Pictet-Water strategy is found to have a purity of 50, this means that half of its enterprise value is derived from marketing products and services that cater to the water industry. The average purity of the companies in our thematic portfolios is at least 65.

Specialist investment managers, not generalists

The specialist skill of our investment managers is another distinguishing feature of Pictet AM's thematic approach. Each thematic strategy is managed by a dedicated investment team, which carries out its own research and constructs its own portfolio. Every team member is a portfolio manager, sharing responsibility for the management of the strategy.

By dedicating all their attention to a clearly-defined group of stocks, investment managers develop distinctive, specialist expertise. This gives thematic equity investment managers a valuable advantage over traditional global equity funds, which work rather differently.

Most mainstream global equity funds are run by managers that are supported by several analysts, whose task it is to generate lists of their best ideas within their designated industry sectors. Often, portfolio managers struggle to process the vast amounts of data emanating from the thousands of stocks that form their universe.

An additional problem is that global or regional equity funds rarely confine themselves to the very best investment ideas their analysts have identified.

Thematic equity investment managers focus on a narrower range of companies and industry segments... this detailed knowledge can simplify the investment process, producing a more focused portfolio.

By contrast, thematic equity investment managers focus on a narrower range of companies and industry segments. This means they are able to build specialist expertise. And this detailed knowledge can simplify the investment decision making process, producing a more focused portfolio whose sources of return and risk are not only distinct but also more clearly understood. This, in turn, can increase the probability of generating better returns. There is ample evidence that selecting stocks from within specific industries – rather than across a broad range of sectors – can deliver better returns.

Thematic stocks don't feature in mainstream indices

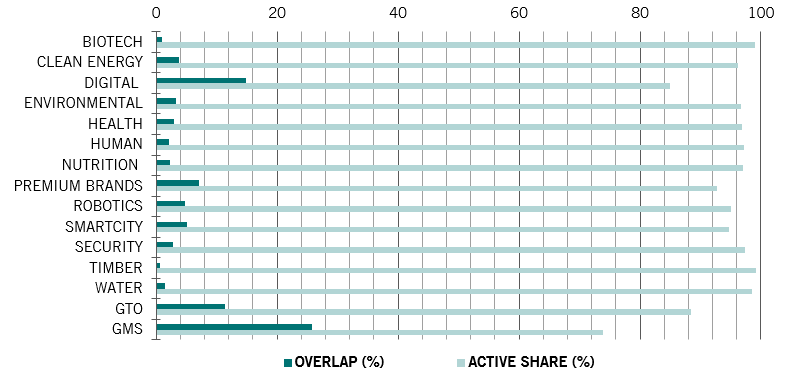

Companies that qualify as thematic investments share another attractive attribute: they do not feature prominently in traditional stock market indices. This has important investment implications. The stocks that find their way into the vast majority of the world’s equity funds are, by and large, constituents of major indices such as the FTSE 100 or the S&P 500 Index.

The result: a portfolio that is destined to generate sub-par returns.

By contrast, thematic equity strategies invest in specialised firms that are not represented in established benchmarks. Essentially, the approach is index agnostic.

Source: Pictet Asset Management, MSCI, Bloomberg, as of 31.08.2018. Overlap = sum of all overlapping fund holdings with index, adding up the min of the two weights. *GEO is an abbreviation for the Global Environmental Opportunities strategy, GTO is an abbreviation for Global Thematic Opportunities and GMS is an abbreviation for Global Megatrend Selection. Data taken from USD share classes of each strategy.

Built to deliver

So with specialist investment managers investing in specialised companies in dynamic industries, we believe we can build a portfolio that draws on the very best of human ingenuity. It’s what sets our actively-managed thematic equity funds apart. It’s also what can help investors get the most from their equity investments.

Dit promotiedocument wordt uitgegeven door Pictet Asset Management (Europe) S.A.. Het richt zich niet tot en is niet bedoeld voor verspreiding aan of gebruik door enige persoon of entiteit die inwoner is van of gevestigd is in enige plaats, staat, land of rechtsgebied waar een dergelijke verspreiding, publicatie, beschikbaarheid of gebruik zou indruisen tegen wet- of regelgeving. Alvorens te beleggen, moeten de recentste versie van het fondsprospectus, het Precontractuele model indien van toepassing, het Essentiële-informatiedocument en de jaar- en halfjaarverslagen worden gelezen. Deze zijn kosteloos beschikbaar, in het Engels op www.assetmanagement.pictet of in papieren vorm bij Pictet Asset Management (Europe) S.A., 6B, rue du Fort Niedergruenewald, L-2226 Luxembourg of bij het kantoor van de eventuele lokale agent, distributeur of centraal administratiekantoor van het fonds.

Het Essentiële-informatiedocument is ook verkrijgbaar in de lokale taal van elk land waar het compartiment is geregistreerd. Mogelijk zijn het prospectus, het Precontractuele model indien van toepassing, en de jaar- en halfjaarverslagen ook verkrijgbaar in andere talen. Raadpleeg de website voor de andere beschikbare talen. Uitsluitend de meest recente versie van deze documenten is geschikt als basis voor beleggingsbeslissingen.

De samenvatting van de rechten van beleggers (in het Engels en in de verschillende talen van onze website) vindt u hier en op www.assetmanagement.pictet onder de kop "Middelen” onderaan de pagina.

De lijst van landen waar het fonds is geregistreerd is verkrijgbaar bij Pictet Asset Management (Europe) S.A., die kan beslissen om de gemaakte afspraken voor de marketing van het fonds of compartimenten van het fonds in elk gegeven land te beëeindigen.

De in dit document verstrekte informatie en gegevens mogen niet worden beschouwd als een aanbod of uitnodiging om effecten of financiële instrumenten te kopen, te verkopen of erop in te schrijven.

De informatie, opinies en ramingen vermeld in dit document weerspiegelen een oordeel op de oorspronkelijke publicatiedatum en kunnen zonder kennisgeving worden gewijzigd. Beheermaatschappij heeft geen stappen ondernomen teneinde te waarborgen dat de effecten waarnaar in dit document wordt verwezen geschikt zijn voor een bepaalde belegger en dit document vervangt niet een eigen onafhankelijke beoordeling. De fiscale behandeling is afhankelijk van de individuele omstandigheden van elke belegger en kan in de toekomst gewijzigd worden.

Alvorens een beleggingsbesluit te nemen, wordt elke belegger aangeraden te controleren of deze belegging geschikt is, rekening houdend met zijn kennis en zijn ervaring in financiële zaken, zijn beleggingsdoelstellingen en zijn financiële situatie, of om specifiek professioneel advies in te winnen.

De waarde en de opbrengsten verbonden met de effecten of financiële instrumenten vermeld in dit document kunnen zowel dalen als stijgen en als gevolg hiervan is het mogelijk dat beleggers hun oorspronkelijke inleg niet geheel terugkrijgen.

Deze beleggingsrichtlijnen zijn interne richtlijnen die binnen de beperkingen van het fondsprospectus op elk moment en zonder kennisgeving kunnen worden gewijzigd. De genoemde financiële instrumenten worden slechts ter illustratie vermeld en mogen niet worden beschouwd als een direct aanbod, beleggingsaanbeveling of beleggingsadvies. Verwijzing naar specifieke effecten is geen aanbeveling om deze effecten te kopen of verkopen. De feitelijke allocaties kunnen worden gewijzigd en kunnen sinds de datum van het marketingmateriaal zijn veranderd.

Resultaten uit het verleden zijn geen garantie of betrouwbare indicator voor toekomstige resultaten. De behaalde resultaten gelden exclusief de commissies en vergoedingen die berekend worden bij inschrijving op of terugkoop van aandelen.

Eventueel hierin vermelde indexgegevens blijven eigendom van de gegevensaanbieder. De Data Vendor Disclaimers (disclaimers van de gegevensaanbieders) zijn te raadplegen op assetmanagement.pictet, onder het kopje ‘Middelen’ onder aan de pagina.

Dit document is een door Pictet Asset Management uitgegeven marketingcommunicatie en valt niet onder enige specifiek aan beleggingsonderzoek gerelateerde MiFID II/MiFIR-vereisten. Dit materiaal bevat niet voldoende informatie om een beleggingsbesluit te ondersteunen. U kunt er niet op vertrouwen om te beoordelen of een belegging in door Pictet Asset Management aangeboden of gedistribueerde producten of diensten u voordelen biedt.

Pictet AM heeft geen rechten of licentie om de handelsmerken, logo's of afbeeldingen in dit document te reproduceren maar heeft wel het recht om het handelsmerk van entiteiten van de Pictet-groep te gebruiken. Uitsluitend ter illustratie.

Cookiebeleid

De op deze site gebruikte cookies hebben tot doel om het surfen te vergemakkelijken en om gegevens te verzamelen voor statistische doeleinden. Als u meer informatie wilt hebben, bezwaar wilt maken of de parameters wilt veranderen, klik dan op de volgende link: Cookiebeleid. Als u verder gaat met uw bezoek aan deze site, dan accepteert u het gebruik van cookies voor de bovenvermelde doeleinden.