The end of QE and rising market volatility favour total return credit strategies.

Written by

Jon Mawby

Co-Head of Absolute & Total Return Credit

Share this article

Long-short credit strategies are coming into their own. After years of being supported by easy central bank money, credit markets are having to come to grips with the unwinding of quantitative easing by the world’s most important central bank – the US Federal Reserve – and less friendly policies elsewhere.

That shift is starting to fuel market volatility. Jon Mawby, manager of Pictet Total Return-Kosmos strategy, explains how this volatility will favour investment approaches that have the flexibility to trade any strategy in any region across the corporate capital structure.

How is the fixed income investment environment changing? How prepared are investors?

Many investors are yet to realise that central banks have moved from a coordinated policy of quantitative easing to coordinated quantitative tightening. In part that’s because central banks had to be more vocal about their efforts to shore up markets during the crisis, whereas now they’re trying to normalise policy without triggering ructions. At the same time, policymakers know they can’t go it alone: they are only too aware of the distortions the European Central Bank caused when it set off on its own path and raised rates in 2011.

It started to become clear post the Sintra meeting in 2017 [the European Central Bank forum on central banking that was held in Portugal] that central banks were moving to a more co-ordinated tightening of policy. If you look at the Bank of Japan with its ‘stealth taper’ or the Bank of England with two rate rises since its post-Brexit emergency cut in 2016, in neither case is a tightening of policy justified by most measures of economic fundamentals. Labour markets might be tight across the globe but inflation remains relatively subdued with the traditional Phillips curve relationship between inflation and unemployment appearing to be much weaker than in the past.

Why, then, are central banks ignoring muted price pressures and continuing to tighten policy? At its core this round of policy normalisation is driven by two factors: first, central banks are worried about the political consequences of their past policies; and, second, they want room to ease when the world moves into its next downturn.

In combination, [central banks'] policies have indirectly fuelled populist politics around the world.

These factors make this round of policy tightening very different from that seen in previous cycles. Central bankers fear that in causing asset prices to become hugely inflated, they’ve caused the fabric of society to tear. Thanks to low wage growth and austerity, the middle classes have been stretched to breaking point, while an ever bigger proportion of wealth has become concentrated among what has become known as the “1 per cent”. This hasn’t been healthy for a world in which economic growth is based on credit creation and expansion.

Purchasing power has simultaneously shifted out of the hands of an economic segment with high marginal propensity to consume – traditionally seen as the economy’s engine – to one that has a much lower propensity to consume. As such, falling unemployment hasn’t set off the same inflationary impulse we’ve seen historically.

Zero interest rates have created another problem: what has, in effect, been a massive shift of pricing power from labour to capital. Ultra-easy monetary policy has made capital very cheap, or in some cases free, for corporations. This has discouraged investment in favour of financial engineering in the form of debt funded buyback and dividends. The net effect has been to create distortions that transfer value from bondholders to shareholders.

In combination, these policies have indirectly fuelled populist politics across the world. Central banks are consequently trying to normalise policy for a number of reasons that aren’t necessarily related to the build-up of inflationary pressures.

What does this mean for the market volatility?

It is difficult to see how normalisation won’t trigger further bouts of volatility similar to those we saw over the summer and, previously, during the taper tantrum in 2013 and again in early 2016. These are all periods that followed shifts to tighter monetary policy regimes. These precedents are particularly relevant for a market that has seen bond yield spreads repressed to artificially low levels, which has made normal price discovery all but impossible. Central banks also seem less willing to step in with soothing rhetoric as they try and prepare markets for higher rates. It’s no surprise that Turkey, which was one of the largest beneficiaries of QE, became one of the first casualties of global quantitative tightening.

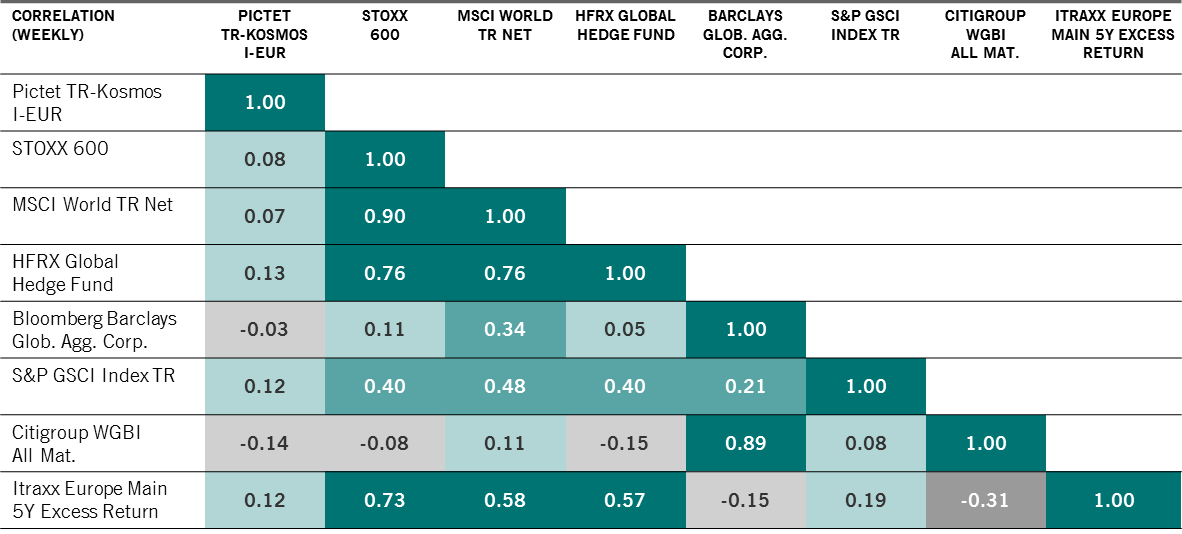

Uncorrelated

Weekly correlation matrix between Pictet TR-Kosmos long short credit and key indices1

Source: Bloomberg and Pictet Asset Management. One week percentage change. Data from 30.06.2011 to 30.09.2018.

This change is likely to trigger bouts of markets turbulence that will expose companies with weak balance sheets, weak operating models and weak governance.

Presumably, it helps to be flexible when volatility hits?

It’s essential not to be tied to indices that end up becoming heavily concentrated in the riskiest companies with the highest levels of debt. Equally, flexibility means you can avoid sectoral or geographic biases.

One essential feature of having flexibility is to not allow your assets and liabilities to become mismatched. The 2008 crisis taught us that asset-liability mismatches can become a huge issue in times of market volatility. Holding large illiquid positions means that if there’s a sudden flurry of client redemptions – as happens during big market crises – the portfolio manager is often left having to sell the fund’s highest quality and most liquid positions. It’s essential to be able to meet redemptions in that circumstance, which is why it makes sense to avoid parts of the market that don’t have clear pricing or are structurally less liquid. Liquidity is a big issue and often one that’s frequently mispriced in the bond market.

Given how expensive many assets have become, what should corporate bond investors do?

Today most of the investment grade universe doesn’t offer much in terms of coupon and, given current valuations, there is a risk of a pronounced correction. This, in turn, makes credit selection more important than ever. There are also more opportunities to take advantage of by setting up short positions – particularly among BBB-rated companies, which have an increasing presence in indices, and are especially vulnerable to credit rating downgrades during an economic downturn2.

Credit by its nature is negatively asymmetric in its return profile – which is to say there’s more potential downside than upside. That’s even more acute at the end of this cycle as historically low yields expose investors to potentially losing many years of coupon income in the event a company suffers a credit rating downgrade or a financial restructuring.

An absolute return strategy like Kosmos has the added benefit of not being judged on relative performance. So in market conditions when everything’s expensive, it can de-allocate or invest in more defensive structures in the form of both long/short credit relative value or trades around a company’s capital structure that, over time, will give it the ability to benefit from volatility rather than be captive to it.

Jon Mawby joined Pictet Asset Management in 2018 and is Co-Head of Absolute & Total Return Credit. At the time of joining, he was Senior Investment Manager in the Developed Markets Credit team.

Before joining Pictet, he was a Senior Portfolio Manager at ManGLG where he was lead portfolio manager for the unconstrained bonds and investment grade strategies. Jon worked at GLG Partners for 6 years having joined to build out their capability in unconstrained bonds. In a career spanning 18 years Jon has also worked at ECM, Gartmore, Morley (Aviva Investors) and Goldman Sachs primarily managing credit portfolios across the full product spectrum from long only to long/short.

Jon holds a B.A. (Hons), Economics from Durham University and is a CFA Charterholder.

Share this article

Important legal information

This marketing material is issued by Pictet Asset Management (Europe) S.A.. It is neither directed to, nor intended for distribution or use by, any person or entity who is a citizen or resident of, or domiciled or located in, any locality, state, country or jurisdiction where such distribution, publication, availability or use would be contrary to law or regulation. The latest version of the fund‘s prospectus, Pre-Contractual Template (PCT) when applicable, Key Information Document (KID), annual and semi-annual reports must be read before investing. They are available free of charge in English on www.assetmanagement.pictet or in paper copy at Pictet Asset Management (Europe) S.A., 6B, rue du Fort Niedergruenewald, L-2226 Luxembourg, or at the office of the fund local agent, distributor or centralizing agent if any.

The KID is also available in the local language of each country where the compartment is registered. The prospectus, the PCT when applicable, and the annual and semi-annual reports may also be available in other languages, please refer to the website for other available languages. Only the latest version of these documents may be relied upon as the basis for investment decisions.

The summary of investor rights (in English and in the different languages of our website) is available here and at www.assetmanagement.pictet under the heading "Resources", at the bottom of the page.

The list of countries where the fund is registered can be obtained at all times from Pictet Asset Management (Europe) S.A., which may decide to terminate the arrangements made for the marketing of the fund or compartments of the fund in any given country.

The information and data presented in this document are not to be considered as an offer or solicitation to buy, sell or subscribe to any securities or financial instruments or services.

Information, opinions and estimates contained in this document reflect a judgment at the original date of publication and are subject to change without notice. The management company has not taken any steps to ensure that the securities referred to in this document are suitable for any particular investor and this document is not to be relied upon in substitution for the exercise of independent judgment. Tax treatment depends on the individual circumstances of each investor and may be subject to change in the future. Before making any investment decision, investors are recommended to ascertain if this investment is suitable for them in light of their financial knowledge and experience, investment goals and financial situation, or to obtain specific advice from an industry professional.

The value and income of any of the securities or financial instruments mentioned in this document may fall as well as rise and, as a consequence, investors may receive back less than originally invested.

The investment guidelines are internal guidelines which are subject to change at any time and without any notice within the limits of the fund's prospectus.

The mentioned financial instruments are provided for illustrative purposes only and shall not be considered as a direct offering, investment recommendation or investment advice. Reference to a specific security is not a recommendation to buy or sell that security. Effective allocations are subject to change and may have changed since the date of the marketing material.

Past performance is not a guarantee or a reliable indicator of future performance. Performance data does not include the commissions and fees charged at the time of subscribing for or redeeming shares.

Any index data referenced herein remains the property of the Data Vendor. Data Vendor Disclaimers are available on assetmanagement.pictet in the “Resources” section of the footer.

This document is a marketing communication issued by Pictet Asset Management and is not in scope for any MiFID II/MiFIR requirements specifically related to investment research. This material does not contain sufficient information to support an investment decision and it should not be relied upon by you in evaluating the merits of investing in any products or services offered or distributed by Pictet Asset Management.

Pictet AM has not acquired any rights or license to reproduce the trademarks, logos or images set out in this document except that it holds the rights to use any entity of the Pictet group trademarks. For illustrative purposes only.

Cookie Policy

This website uses cookies to enhance user navigation and to collect statistical data. To refuse the use of cookies, change your settings or for more information, please click on the following link: Cookies policy. By continuing to browse this website, you accept the use of cookies for the above purposes.