EM corporate bonds are a rare source of income in a low yield world.

Written by

Alain Nsiona Defise

Co-Head of Emerging Markets - Corporate

Share this article

Emerging market corporate bonds are a beacon for investors struggling to find sufficient income. Not only do they offer the sort of yields that have all but disappeared elsewhere, but they’re underpinned by solid economic fundamentals. And because these bonds mature sooner on average than their sovereign emerging market counterparts, they’re better placed to weather rising global interest rates.

In a world starved of income, emerging market (EM) corporate bonds are coming into their own. Yields are some of the highest available among the major fixed income asset classes. In fact, they’re only surpassed by those on EM local currency debt and US high yield credit.

This makes EM corporate particularly attractive given how abnormally compressed spreads have become across much of the rest of the fixed income universe – and the huge volume of negative yielding developed government and top-rated European corporate debt.

The broad index of EM corporate bonds – the JPMorgan CEMBI broad diversified – offered yields of 5.4 per cent at the end of December, substantially above those on offer from US and European investment grade bonds and the European high yield credit market.

Investors have noticed. EM corporate bonds had posted total returns of some 9.7 per cent in 2016, the best performing part of the corporate credit universe apart from US high yield. What’s more, EM corporate bonds have weathered the very recent shakeout in global bonds better than most other classes of fixed income.

Solid fundamentals underpin EM corporates

In part, EM firms are able to deliver solid income thanks to relatively strong and stable economic growth in their home countries. We expect emerging economies to deliver 4.3 per cent GDP growth in 2017, compared with just 1.8 per cent in the developed world, extending a trend that’s evolved over the past couple of years. Meanwhile, emerging market inflation has been falling, giving central banks scope to ease monetary policy and spur growth.

Premium growth

Change in GDP on previous year

Source: Pictet Asset Management, CEIC, Datastream. Forecasts from 2016.

Solid economic fundamentals help to underpin EM corporations’ creditworthiness, which is usually better than at of equivalently-rated developed market borrowers. And, significantly, that quality comes at a discount because EM company bonds trade at wider spreads.

To some, this differential boils down to domestic sovereign risk premia. Some observers argue that the discount is justified because, unlike their developed country counterparts, EM companies’ creditworthiness can be constrained by the actions of their governments. And yet with close analysis it’s possible to find companies that are relatively insulated from domestic factors.

For example, a number of Turkish corporate bonds we’ve been invested in since before last summer’s coup attempt weathered the country’s subsequent political upheavals thanks to their strong fundamentals. They maintained their investment grade credit ratings even though the sovereign was downgraded by Moody’s.

It’s ironic that EM corporates should be disentangling themselves from sovereign factors at a time that their developed economy counterparts are so heavily under the sway of their domestic central banks.

Weathering bond market volatility

Recent market volatility reflects concerns that there could be a general move towards tighter monetary policy in the developed world. Investors are still digesting the significance of the Bank of Japan’s recent shift from targeting quantities of assets purchases to controlling the level of Japanese yields. There is talk the European Central Bank could start tapering next year. And the US Federal Reserve in broadly expected to keep tightening policy at a steady pace after raising rates in December.

So far the fallout to EM corporate bonds has been relatively modest. Yet if monetary conditions become significantly less friendly, EM corporate bonds should fare better than, say, their sovereign counterparts, which are far more sensitive to changes in interest rates.

The yield offered by EM corporates is comparable to that on hard currency EM government bonds, but with substantially shorter duration, at 4.8 years compared to 7 years for the sovereign debt.

EM corporate bonds stack up well against the alternatives, given a mix of shorter duration and solid yield, together with default and recovery rates1 that are broadly in line with developed market counterparts.

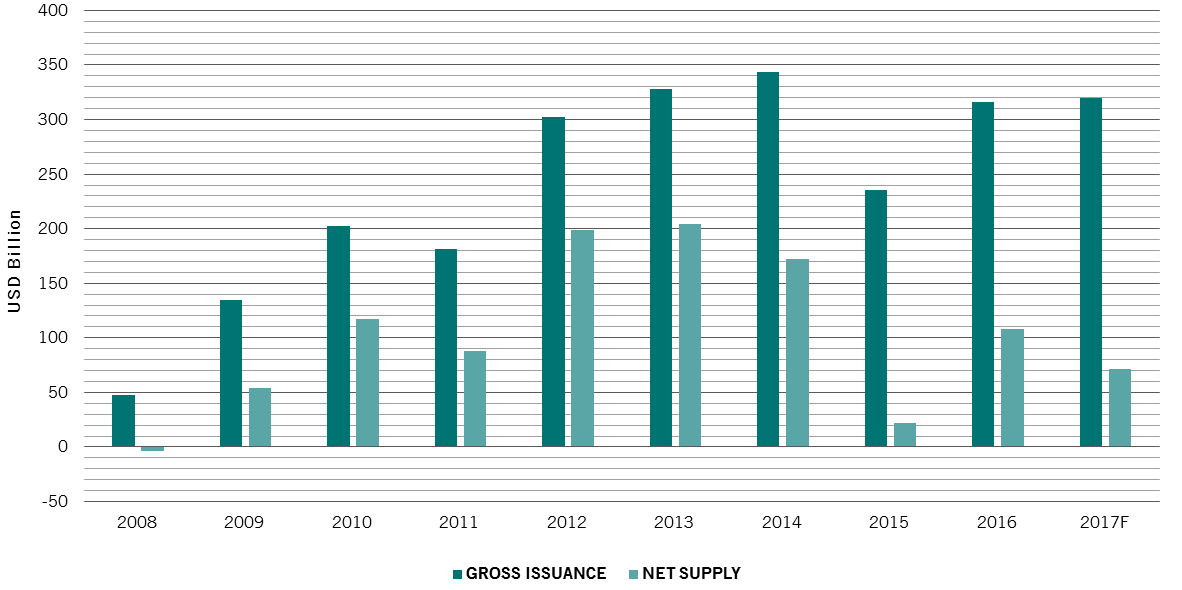

Worrying less about dollar borrowing

Meanwhile, technical factors are also increasingly favourable for the asset class. Hitherto, various observers – including the International Monetary Fund – have flagged concerns about booming dollar borrowing among EM corporates. A major concern is what happens to EM companies’ ability to service their debts if the dollar starts to rise on the back of tighter Fed policy. But while gross supply of EM corporate paper has remained relatively high, recently much of it has been used to refinance existing debt. Net new issuance dropped substantially in 2015 and only partially recovered in 2016.

less than it seems

Gross and net EM corporate annual supply

Source: BofA Merrill Lynch Global Research as at 07.01.2017

What’s more, the impact of a rising dollar on the market isn’t universally negative. It’s true that the greenback’s strength makes it harder for firms that borrow in dollars but generate revenues in local currencies to service their debts. But companies with dollar-denominated borrowing which also sell dollar-priced goods and have local currency costs (often commodity producers) will tend to benefit from a stronger US currency.

Bottom up management

Notwithstanding the generally favourable macro and technical backdrop for EM corporates, we protect our investors from the vagaries of both global economic forces and idiosyncratic political risk by focusing on bottom up company analysis. This allows us to find interesting prospects in even unfriendly environments.

What’s more, because they are largely held by institutions, which tend to be less subject to rapid shifts in sentiment than retail investors, EM corporate bonds tend to be less volatile than, say, EM sovereign debt.

Our current positioning is built of a combination of defensive positions – which include Chinese and Indian oil and gas names – investments with prospects of intermediate returns, including Turkish non-financials and Russian names likely to benefit most from the country’s recovery, and more ambitious holdings geared more heavily into a global rebound, like Latin American energy names and Brazilian industrials.

This marketing material is issued by Pictet Asset Management (Europe) S.A.. It is neither directed to, nor intended for distribution or use by, any person or entity who is a citizen or resident of, or domiciled or located in, any locality, state, country or jurisdiction where such distribution, publication, availability or use would be contrary to law or regulation. The latest version of the fund‘s prospectus, Pre-Contractual Template (PCT) when applicable, Key Information Document (KID), annual and semi-annual reports must be read before investing. They are available free of charge in English on www.assetmanagement.pictet or in paper copy at Pictet Asset Management (Europe) S.A., 6B, rue du Fort Niedergruenewald, L-2226 Luxembourg, or at the office of the fund local agent, distributor or centralizing agent if any.

The KID is also available in the local language of each country where the compartment is registered. The prospectus, the PCT when applicable, and the annual and semi-annual reports may also be available in other languages, please refer to the website for other available languages. Only the latest version of these documents may be relied upon as the basis for investment decisions.

The summary of investor rights (in English and in the different languages of our website) is available here and at www.assetmanagement.pictet under the heading "Resources", at the bottom of the page.

The list of countries where the fund is registered can be obtained at all times from Pictet Asset Management (Europe) S.A., which may decide to terminate the arrangements made for the marketing of the fund or compartments of the fund in any given country.

The information and data presented in this document are not to be considered as an offer or solicitation to buy, sell or subscribe to any securities or financial instruments or services.

Information, opinions and estimates contained in this document reflect a judgment at the original date of publication and are subject to change without notice. The management company has not taken any steps to ensure that the securities referred to in this document are suitable for any particular investor and this document is not to be relied upon in substitution for the exercise of independent judgment. Tax treatment depends on the individual circumstances of each investor and may be subject to change in the future. Before making any investment decision, investors are recommended to ascertain if this investment is suitable for them in light of their financial knowledge and experience, investment goals and financial situation, or to obtain specific advice from an industry professional.

The value and income of any of the securities or financial instruments mentioned in this document may fall as well as rise and, as a consequence, investors may receive back less than originally invested.

The investment guidelines are internal guidelines which are subject to change at any time and without any notice within the limits of the fund's prospectus.

The mentioned financial instruments are provided for illustrative purposes only and shall not be considered as a direct offering, investment recommendation or investment advice. Reference to a specific security is not a recommendation to buy or sell that security. Effective allocations are subject to change and may have changed since the date of the marketing material.

Past performance is not a guarantee or a reliable indicator of future performance. Performance data does not include the commissions and fees charged at the time of subscribing for or redeeming shares.

Any index data referenced herein remains the property of the Data Vendor. Data Vendor Disclaimers are available on assetmanagement.pictet in the “Resources” section of the footer.

This document is a marketing communication issued by Pictet Asset Management and is not in scope for any MiFID II/MiFIR requirements specifically related to investment research. This material does not contain sufficient information to support an investment decision and it should not be relied upon by you in evaluating the merits of investing in any products or services offered or distributed by Pictet Asset Management.

Pictet AM has not acquired any rights or license to reproduce the trademarks, logos or images set out in this document except that it holds the rights to use any entity of the Pictet group trademarks. For illustrative purposes only.

Cookie Policy

This website uses cookies to enhance user navigation and to collect statistical data. To refuse the use of cookies, change your settings or for more information, please click on the following link: Cookies policy. By continuing to browse this website, you accept the use of cookies for the above purposes.