Asset allocation: shifting into neutral for global bonds

For the world economy, it is no longer full steam ahead: our business cycle analysis suggests that growth has peaked. That doesn’t necessarily mean a slowdown – much less a recession – is around the corner. In fact, we expect growth will remain resilient, holding at around its long-term trend levels over the next five years.

However, it does signal a shift in gear, and it won’t be long before financial markets start to adjust accordingly. As the first step of that adjustment, we have dialed our positions back to neutral across the board. This has meant upgrading bonds, downgrading cash and leaving equity allocation unchanged from last month.

May 2018

Source: Pictet Asset Management

With our global leading indicator falling for the past five months in a row and the Citi Economic Surprise Index dipping into the red, bonds certainly look like a more attractive proposition – or at least a less unattractive one. Positioning is also potentially supportive, with a near record 55 per cent of fund managers surveyed by the Bank Of America-Merrill Lynch underweight US government bonds.

On the face of it, central bank policy offers a further argument in favour of fixed income. Our global liquidity gauge points to a tightening in monetary conditions. However, the slowing growth could give policymakers pause for thought.

While we think that the weakness in the first quarter is an “air pocket” in an environment of solid growth, a second quarter of sub-par data may prompt the US Federal Reserve to slow down the pace of its tightening compared to the two to three hikes currently priced in by markets. It may also encourage China into launching new stimulus measures.

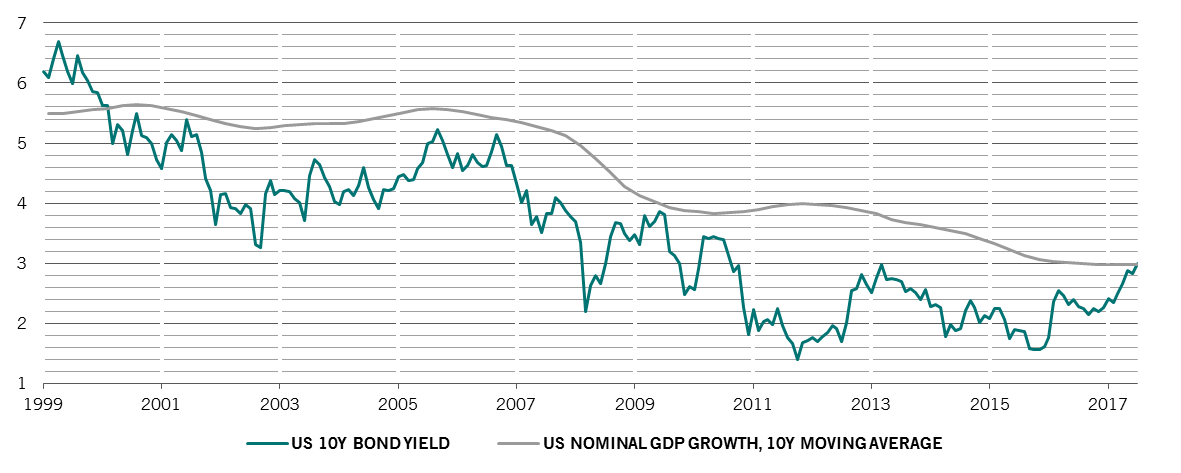

Valuations, too, do not offer a compelling “buy” signal for equities nor bonds. True, benchmark 10-year US Treasury yields have breached the landmark 3 per cent yield level for the first time since 2014 (see chart). But, in aggregate, bonds remain expensive on our models: rising inflation, a tighter Fed and still solid growth would suggest an overshoot in yields is possible.

On balance, therefore, we see reason to upgrade bonds, but only by one notch: to neutral from underweight. That puts them on a par with our equity position.

US 10-year government bond yields and nominal GDP growth, %

While a correction here is likely over the medium term, we think it is too early to call the end to the bull market. Recent weakness has taken stock market valuations down to neutral levels, offering potential fresh entry points. Any sign of scaling back on the Fed’s tightening plans could provide a catalyst for a final hurrah. Technical indicators broadly support our top level asset allocation, with neutral short-term sentiment readings for both bonds and equities.