Hex Romana

Italy may have a government but the country's problems haven't gone away. That's a worry for the euro zone.

Par

Andrea Delitala

Head of Multi Asset Euro

Luca Paolini

Stratégiste en Chef

Italy has a new government. For now, crisis has been averted. But that doesn’t mean the political and market turmoil is over. Like a virus, the threat of a euro zone break-up triggered by Italy will linger for years to come. And this risk is likely to remain factored into asset prices.

With the agreement of a coalition between the populist Northern League and Five Star Alliance, the febrile mood that infected Italian politics and markets has suddenly cooled. Now that talk of anti-euro policies is no longer making headlines, investors are able to turn their focus back to some of Italy’s more positive fundamentals. After years of stagnation, the economy is growing at more than 1 per cent in inflation adjusted terms. The current account is showing a surplus of more than 2 per cent of GDP. As is the fiscal balance, once adjusted for the economic cycle and interest costs. Reforms to the labour market and other areas of the economy are being implemented.

Italy’s debt profile is also not quite as troubling as the headlines suggest. The average duration of Italian government’s liabilities has lengthened, while domestic investors hold the lion’s share of this debt.

Finally, membership of the euro is popular among Italians – the latest survey shows 70 per cent support.

Italy, then, is no Greece. But over the long run, that’s precisely its problem. It would be too big to save if its debts became unsustainable. And there remains a residual risk that the euro zone’s third largest economy will end up triggering a break-up of the euro – whether by design or accident.

In part that’s because the Italian economy is still uncompetitive relative to the single currency’s other big hitters. Italy also has among the lowest ratios of working age to total population of all major developed countries, at under 65 per cent compared to an average of 66.4 per cent for the OECD overall. And with a low birth-rate and ageing population – 21 per cent of Italians are over 65 – that proportion will only get worse. Italy has one of the world’s worst labour productivity rates and only Greece has lower GDP per hour worked in the OECD. Our fair value estimates suggest that were Italy to adopt a new, floating currency, it would immediately have to devalue by up to 30 per cent to regain lost competitiveness.

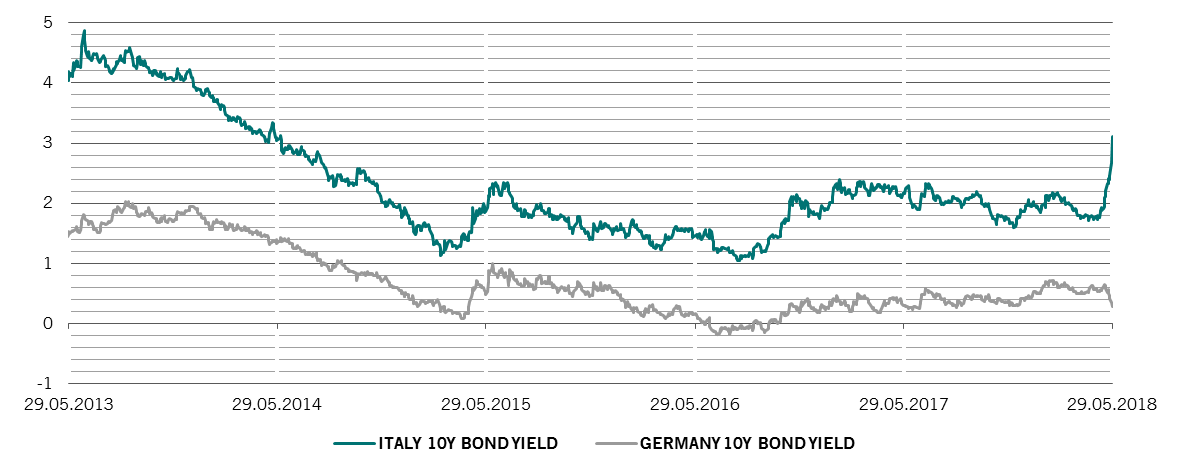

spreading fear

Italian and German 10-year government bond yields, %

Meanwhile, the rise of populism has in large part been a reaction to a flood of migrants and asylum seekers from Africa and the Levant.

These factors are likely to set Italy’s new government on a collision course with the European Commission. With domestic growth prospects relatively poor, it wants to pump the economy with a big fiscal spending programme, which means government budget deficits.The latest estimates are for an additional EUR120bn of spending, which is around 7 per cent of GDP.

This would necessitate EC approval – which is unlikely to be forthcoming given that Italy already has Europe’s highest debt to GDP ratio of over 130 per cent. Brussels – and most crucially Germany – is unlikely to tolerate deficits incompatible with the stability of Italy's debt to GDP ratio. Any drop in the country's primary surplus below around 0.6 per cent from the current 1.9 per cent is like to contravene the EU's fiscal compact. At the same time, the new Italian coalition will want the rest of the EU to take a bigger share of the migrant burden. This too is likely to be fraught, not least because the likes of Germany have also tilted towards populism in response to their own immigration problems.

The upshot is that the market is unlikely to return to previous complacency. As recently as April, bond investors were assigning virtually zero risk to breakup of the euro zone. By May 29, the gap in yields between Italian government bonds (BTPs) and their German equivalents had widened to effectively discount a one in five chance that Italy would leave the euro, according to our proprietary model. That may still only have been half the 40 per cent probability reached during the 2011-12 crisis, but it was significant. And though it’s shrunk with the subsequent rally, the risk won’t disappear altogether – the current spread is just over 200 basis points, leaving the probability of Italiexit at around 5 per cent.

Because Italian banks, while well capitalised, have large holdings of Italian government bonds, even this gauge might underestimate the potential for euro zone fragmentation. According to the Bank for International Settlements, BTPs account for 20 per cent of Italian bank assets. That’s among the highest levels in the world.

Our estimates suggest that every 100 basis point widening in the BTP/Bund yield spread reduces Italian banks’ capital by 30 basis points. A 300 basis point widening could begin to cause the sector serious discomfort, not least because sovereign bond losses could spark deposit outflows and make it difficult for banks to sell on non-performing loans.

Whatever happens, a lasting Pax Romana seems unlikely.

Informations juridiques importantes

Le modèle précontractuel le cas échéant, le Document d’information clé ainsi que le prospectus doivent être lus avant toute décision d’investir. Le prospectus (en anglais et en français), le modèle précontractuel le cas échéant, le Document d’information clé (en français et en néerlandais), ainsi que les derniers rapports annuels et semi-annuels (en anglais et en français) sont disponibles gratuitement auprès de notre agent financier belge CACEIS Belgium S.A., 86C /b320, Avenue du Port, 1000 Bruxelles ou auprès de la société de gestion, Pictet Asset Management (Europe) S.A., 6B, rue du Fort Niedergruenewald, L-2226 Luxembourg, ainsi qu’au format électronique sur www.assetmanagement.pictet.

Le résumé des droits des investisseurs est disponible (en français et en néerlandais) sur www.assetmanagement.pictet sous la rubrique "Ressources", en pied de page.

La liste des pays où le compartiment est enregistré peut être obtenue en tout temps auprès de Pictet Asset Management (Europe) S.A., qui peut décider de cesser la commercialisation du compartiment dans un pays donné.

Les VNI sont consultables sur www.beama.be.

Servie de plainte et de médiation : Pour toute réclamation, vous pouvez vous adresser à Pictet Asset Management (Europe) S.A., Service Compliance, 6B, rue du Fort Niedergruenewald, L-2226 Luxembourg ou au Service de Médiation pour le Consommateur, North Gate II, Boulevard du Roi Albert II 8 à 1000 Bruxelles ou sur le site www.mediationconsommateur.be. Le Service de Médiation pourra suggérer des solutions pour le règlement du différend. A défaut d’accord sur les solutions proposées, chaque partie a la possibilité de saisir les tribunaux compétents.

Ce document promotionnel est émis par Pictet Asset Management (Europe) S.A. Il n’est pas destiné à être distribué à ou utilisé par des personnes physiques ou des entités qui seraient citoyennes d’un Etat ou auraient leur domicile ou résidence dans un lieu, Etat, pays ou une juridiction dans lesquels sa distribution, publication, mise à disposition ou utilisation seraient contraires aux lois ou règlements en vigueur.

Les informations, avis et évaluations qu’il contient reflètent un jugement au moment de sa publication et sont susceptibles d’être modifiés sans notification préalable. Pictet Asset Management (Europe) S.A. n’a pris aucune mesure pour s’assurer que les fonds auxquels faisait référence le présent document étaient adaptés à chaque investisseur en particulier, et ce document ne saurait remplacer un jugement indépendant. Le traitement fiscal dépend de la situation personnelle de chaque investisseur et peut faire l’objet de modifications. Avant de prendre une décision d’investissement, il est recommandé à tout investisseur de vérifier si cet investissement est approprié compte tenu, notamment, de ses connaissances et de son expérience en matière financière, de ses objectifs d’investissement et de sa situation financière, ou de recourir aux conseils spécifiques d’un professionnel de la branche.

La valeur et les revenus tirés des titres ou des instruments financiers mentionnés dans le présent document peuvent fluctuer à la hausse ou à la baisse, et il est possible que les investisseurs ne récupèrent pas la totalité du montant initialement investi.

Ce document promotionnel n’a pas pour objet de remplacer la documentation détaillée émise par le fonds ou les informations que les investisseurs doivent obtenir du ou des intermédiaires financiers en charge de leurs investissements dans les parts ou actions des fonds mentionnés dans ce document.

Les directives d’investissement sont des directives internes susceptibles d’être modifiées à tout moment, sans préavis, dans le respect des limites précisées dans le prospectus du fonds. Les instruments financiers auxquels il est fait référence sont mentionnés uniquement à des fins d’illustration et ne sauraient être considérés comme une offre commerciale directe, une recommandation de placement ou un conseil en placement. La référence à un titre particulier ne constitue pas une recommandation d’achat ou de vente du titre en question. Les allocations existantes sont sujettes à modification et peuvent avoir évolué depuis la date de publication initiale de la documentation marketing.

Toute donnée relative à un indice figurant dans le présent document demeure la propriété du fournisseur de données concerné. Les mentions légales des fournisseurs de données sont consultables sur le site assetmanagement.pictet, sous la rubrique «Ressources», en pied de page.

Ce document est une communication marketing publiée par Pictet Asset Management. Il n’est pas visé par les dispositions de la directive MiFID II et du règlement MiFIR se rapportant expressément à la recherche en investissement. Il ne comporte pas suffisamment d’informations pour servir de fondement à une décision d’investissement. Vous ne devriez dès lors pas vous appuyer sur son contenu pour examiner l’opportunité d’investir dans des produits ou des services proposés ou distribués par Pictet Asset Management.

Pictet AM n’a acquis ni droits ni licences l’autorisant à reproduire les marques, logos ou images figurant dans le présent document, mais détient le droit d’utiliser les marques des entités du groupe Pictet. Uniquement à des fins d’illustration.