After Argentina and Turkey where next?

Turkey and Argentina have dominated the headlines but the South African rand and Brazilian real are the next worst performing currencies since the onset of the crisis. Is this justified?

Written by

Sabrina Khanniche

Senior Economist

Anjeza Kadilli

Senior Economist

The next to fall?

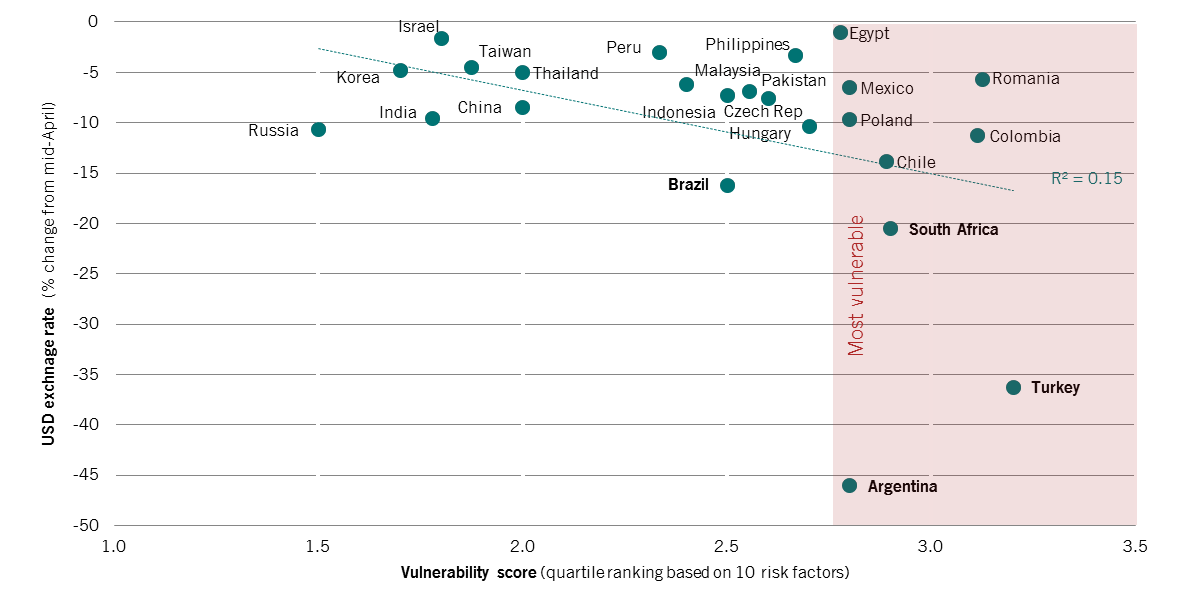

Our proprietary EM vulnerability score card shows that the correction may be justified for South Africa but less so for Brazil.

What is happening in these markets and should we expect more weakness from both currencies?

EM currencies vs USD (%) & vulnerability scores (ranks)

Brazil: fighting fit

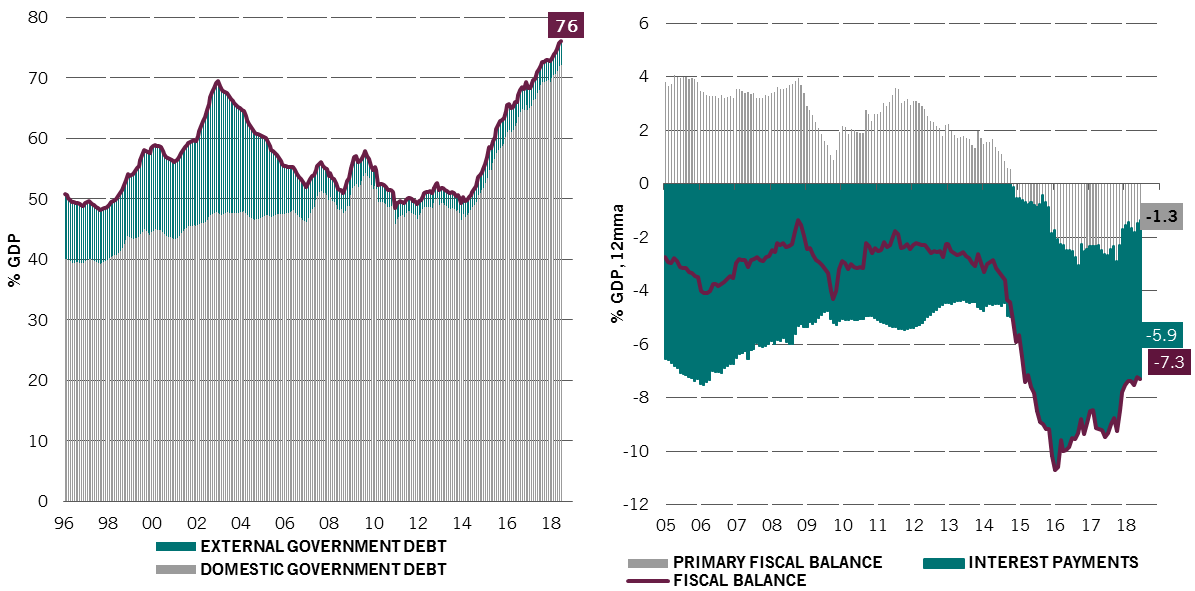

Between the four markets, Brazil seems in best economic health. Whilst Argentina, Turkey and South Africa have significant current account deficits, Brazil’s is relatively narrow. Meanwhile, it has significant foreign currency reserves (USD370 bn) equivalent to 27 months of imports to defend its currency.

More of an issue is public debt of 76% of GDP (the second largest in EM after Egypt), which is expected to rise for a couple of years even in the most optimistic scenarios.

The mitigating factor is that roughly 95% of public debt is owned by domestic holders, who are more captive due to a range of factors, and therefore less volatile than debt owned by overseas investors.

FIGURE 2 LEFT CHART: BRazil's Public debt decomposed by domestic & external (% GDP) / RIGHT CHART: Brazil's fiscal balance (% GDP)

Elections take centre stage

It appears Brazil’s vulnerability is largely due to the uncertain outcome of next month's elections (the first round is on the 7th October, the second on the 28th).

Candidates span the political spectrum. At this stage the two front-runners are Fernando Haddad (official candiate of the Workers Party backed by jailed former President Lula) and right wing Jair Bolsonaro, who was recently stabbed in the street whilst on the campaign trail.

Brazil's vulnerability is due to the uncertain outcome of next month's elections.

We believe that regardless of who wins, the public debt issue will be addressed. The depth of the reforms will depend however on the political and personal profile of the winner.

South Africa: running out of steam?

Across the Atlantic, South Africa is arguably more vulnerable than Brazil to global developments due to its weak macro fundamentals and volatile political environment.

The honeymoon period President Ramaphosa enjoyed after his February election is now over and the currency has weakened again. South Africa technically entered recession in Q2 for the first time since 2009. The rand was also hit by concerns that a change in the constitution later this month could result in Zimbabwe-style land seizures.

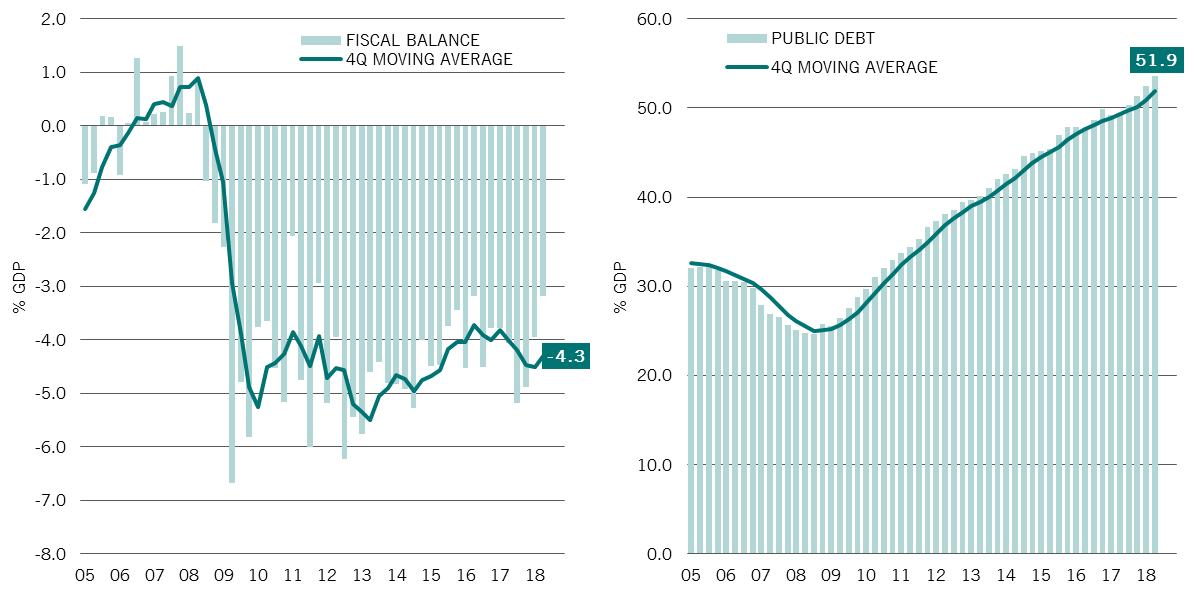

On the domestic side, the fiscal deficit is significant. Announced tax increases are unlikely to curtail spiralling public sector expenditure exacerbated by struggling state owned enterprises (SOEs).

FIGURE 3 LEFT CHART: South Africa government fiscal balance to GDP ratio / RIGHT CHART: South Africa government debt to GDP ratio

On the external front, the current account deficit remains high. This reflects weaker demand and is financed by volatile portfolio flows (stocks and bonds) prone to changes in global financing conditions and sovereign credit ratings. The depreciation of the rand is likely to push up inflation, which is already close to its upper target range. This would limit the central bank's scope for more accommodative monetary policy.

Final thoughts...

Both emerging markets need to be watched closely. But we believe South Africa is most likely to feel the heat in coming months.

It is more globally exposed than Brazil, and vulnerable to trade issues and wider tensions between China and the US (its second and third trading partners respectively). We also feel uncertain political governance could increase the strain on its already weak fiscal position.

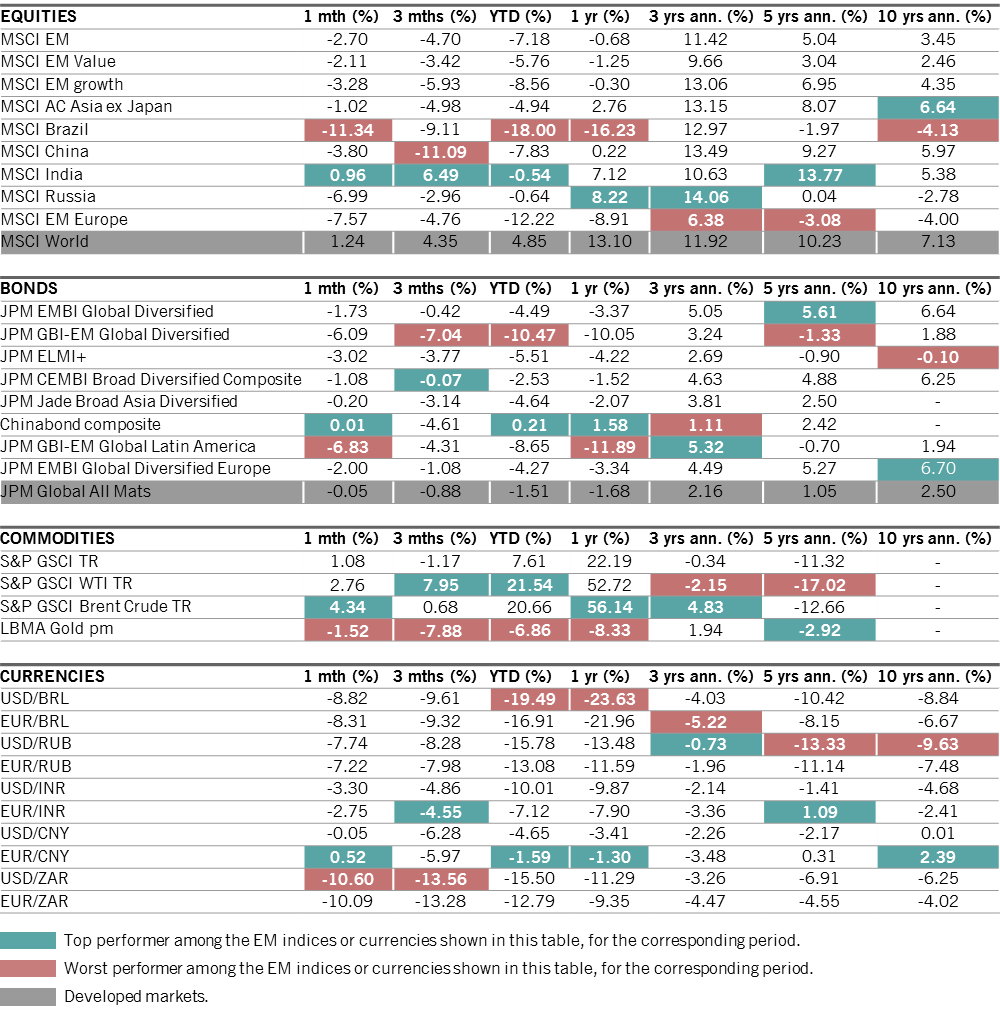

MARKET WATCH

MARket watch data

31.08.2018

READ MORE

A tale of two emerging market crises

Argentina and Turkey have been at the heart of the recent sell-off. Investors should look to policymakers and governments for clues as to where these markets are headed.

August 2018

Some unintended effects of US-China trade tensions

As tensions between the US and China over trade tariffs escalate, a potentially brighter picture of trade dynamics is emerging.

April 2018

Turkey: a canary in the emerging market coalmine?

Investors are concerned that Turkey's currency crisis could destabilise emerging markets and the world economy. That's unlikely.

August 2018

Important legal information

This marketing material is issued by Pictet Asset Management (Europe) S.A.. It is neither directed to, nor intended for distribution or use by, any person or entity who is a citizen or resident of, or domiciled or located in, any locality, state, country or jurisdiction where such distribution, publication, availability or use would be contrary to law or regulation. The latest version of the fund‘s prospectus, Pre-Contractual Template (PCT) when applicable, Key Information Document (KID), annual and semi-annual reports must be read before investing. They are available free of charge in English on www.assetmanagement.pictet or in paper copy at Pictet Asset Management (Europe) S.A., 6B, rue du Fort Niedergruenewald, L-2226 Luxembourg, or at the office of the fund local agent, distributor or centralizing agent if any.

The KID is also available in the local language of each country where the compartment is registered. The prospectus, the PCT when applicable, and the annual and semi-annual reports may also be available in other languages, please refer to the website for other available languages. Only the latest version of these documents may be relied upon as the basis for investment decisions.

The summary of investor rights (in English and in the different languages of our website) is available here and at www.assetmanagement.pictet under the heading "Resources", at the bottom of the page.

The list of countries where the fund is registered can be obtained at all times from Pictet Asset Management (Europe) S.A., which may decide to terminate the arrangements made for the marketing of the fund or compartments of the fund in any given country.

The information and data presented in this document are not to be considered as an offer or solicitation to buy, sell or subscribe to any securities or financial instruments or services.

Information, opinions and estimates contained in this document reflect a judgment at the original date of publication and are subject to change without notice. The management company has not taken any steps to ensure that the securities referred to in this document are suitable for any particular investor and this document is not to be relied upon in substitution for the exercise of independent judgment. Tax treatment depends on the individual circumstances of each investor and may be subject to change in the future. Before making any investment decision, investors are recommended to ascertain if this investment is suitable for them in light of their financial knowledge and experience, investment goals and financial situation, or to obtain specific advice from an industry professional.

The value and income of any of the securities or financial instruments mentioned in this document may fall as well as rise and, as a consequence, investors may receive back less than originally invested.

The investment guidelines are internal guidelines which are subject to change at any time and without any notice within the limits of the fund's prospectus. The mentioned financial instruments are provided for illustrative purposes only and shall not be considered as a direct offering, investment recommendation or investment advice. Reference to a specific security is not a recommendation to buy or sell that security. Effective allocations are subject to change and may have changed since the date of the marketing material.

Past performance is not a guarantee or a reliable indicator of future performance. Performance data does not include the commissions and fees charged at the time of subscribing for or redeeming shares.

Any index data referenced herein remains the property of the Data Vendor. Data Vendor Disclaimers are available on assetmanagement.pictet in the “Resources” section of the footer. This document is a marketing communication issued by Pictet Asset Management and is not in scope for any MiFID II/MiFIR requirements specifically related to investment research. This material does not contain sufficient information to support an investment decision and it should not be relied upon by you in evaluating the merits of investing in any products or services offered or distributed by Pictet Asset Management.

Pictet AM has not acquired any rights or license to reproduce the trademarks, logos or images set out in this document except that it holds the rights to use any entity of the Pictet group trademarks. For illustrative purposes only.