Turkey is on the verge of a balance of payments crisis unless it delivers policy reforms.

Written by

Nikolay Markov

Senior Economist

Share this article

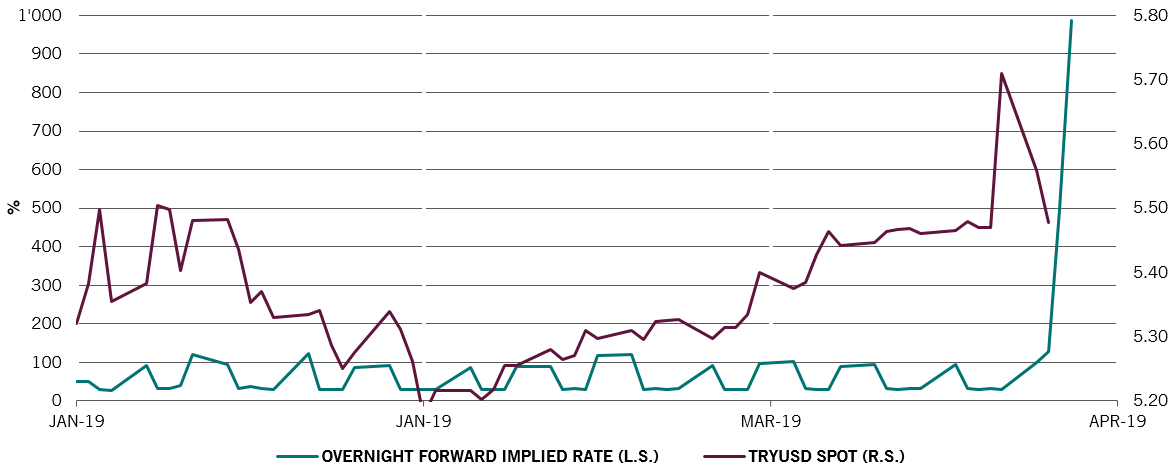

The big squeeze

After last year’s August currency crisis, the Turkish lira hit the headlines again in late March with a surge in its implied overnight forward rate and exchange rate. The reasons behind this flash rally are convoluted but effectively it was led by short positioning as well as quasi capital controls introduced by the government last summer.

The bout of market volatility came just as local elections saw the incumbent AKP government of President Erdogan lose some of its power, especially in major urban centres.

How will the administration react to this setback – should we expect a swing into great economic populism or more of a progressive reformist agenda? Until there is clarity, concerned investors are likely to exert continued downward pressure on the currency.

Source: Pictet Asset Management, CEIC, Datastream, April 2019

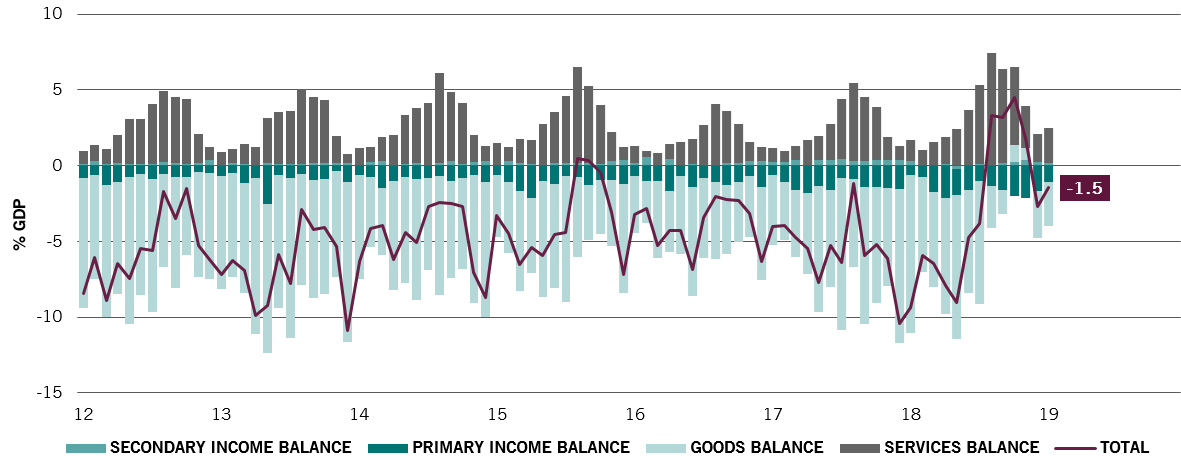

A tangled web

Turkey has the second highest inflation in developing markets after its equally troubled EM 'twin' - Argentina. Even though our indicators show Turkish inflation may have peaked for now, we think precarious economic conditions and political uncertainty mean the risk of a full-fledged balance of payments crisis remains.

This fragility is expressed in Turkey’s volatile current account which, as shown below, has flipped back into deficit. Further significant depreciation in the Turkish lira risks a negative feedback loop that will further widen the economic recession.

Fig. 2: TURKEY's current account breakdown

Source: Pictet Asset Management, CEIC, Datastream, January 2019

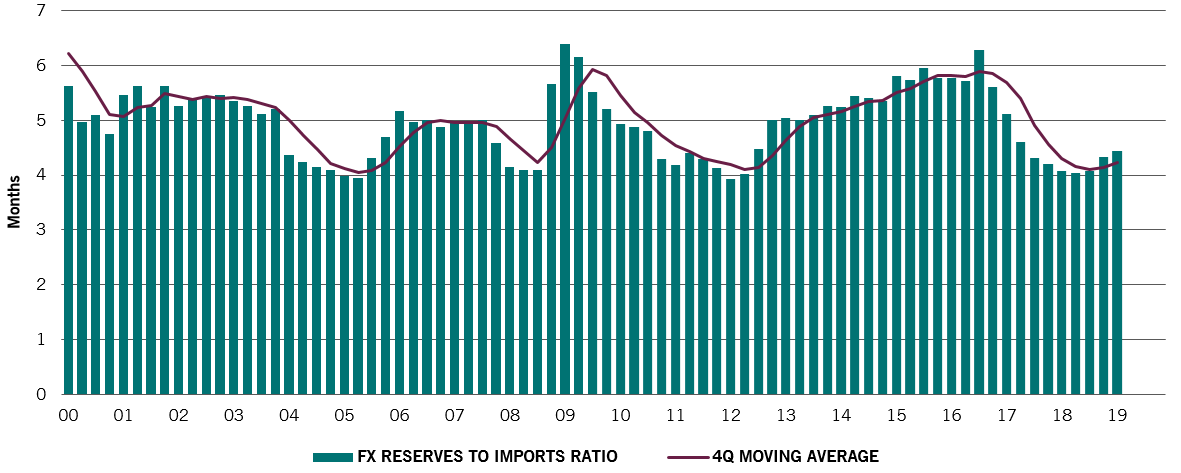

Running out of road?

Further fragility is evident in Turkey’s FX reserves, which are equivalent to just four months of imports. By contrast Brazil has 25 months and China 16 months.

Fig. 3: Turkey FX reserves to MONTHS OF imports

Source: Pictet Asset Management, CEIC, Datastream, January 2019

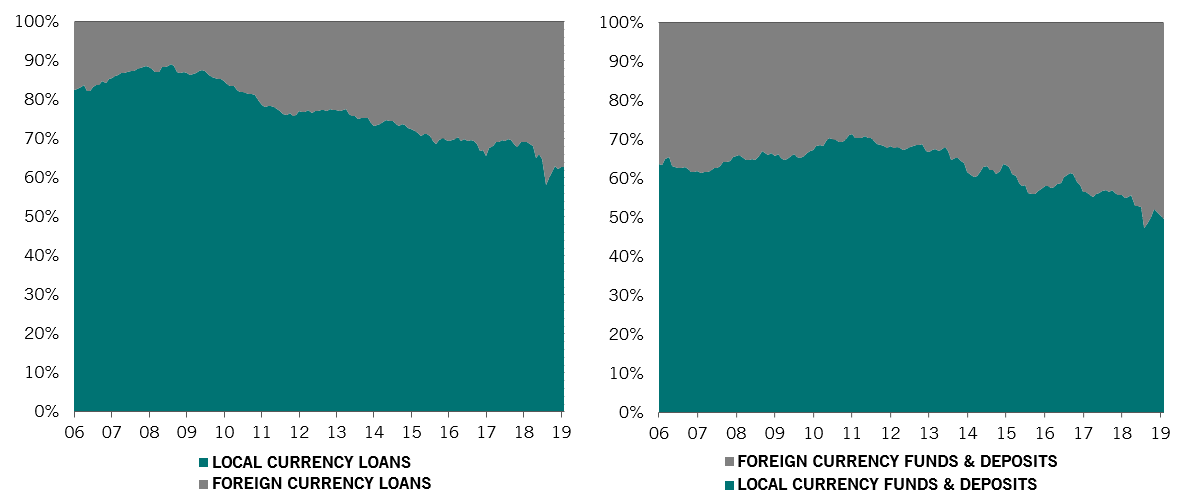

Growing dollar reliance

Another concern is the increasing dollarisation of loans in the economy (see left-hand chart below). However, this is currently being more than tracked by an increase in dollar deposits, as the right chart shows, which implies the risk of currency mismatch remains muted for now.

Source: Pictet Asset Management, CEIC, Datastream, February 2019

Where now politically?

Overall, we see the outcome of the recent elections as rather mixed in terms of investment opportunities. At the margin, given the weaker AKP position we could see a switch to a more market-friendly environment where authorities start implementing some of the highly needed short-term and structural policy reforms. If this happens then Turkey might avoid tumbling into the abyss of greater economic crisis.

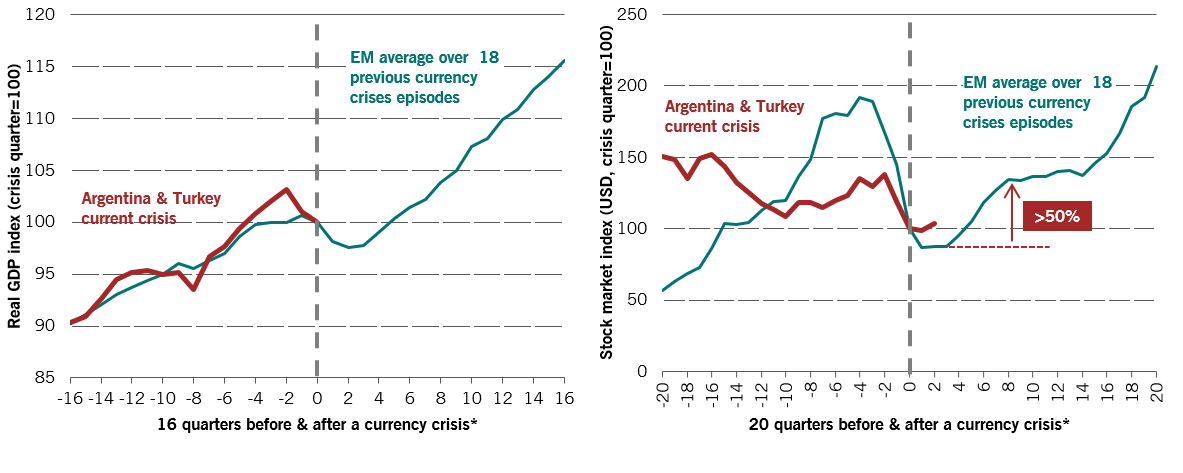

What about markets?

Looking at 18 previous episodes of currency crisis* in emerging markets below shows that it typically takes four to six quarters on average for GDP to recover to the level before the onset of any currency crisis. Meanwhile in terms of equity markets our backtest shows on average they bottom for 4 quarters before entering a steep recovery phase.

This would suggest that Turkey (and Argentina) possibly have at least two more quarters to endure before a recovery in either GDP or equity markets begins. A continuation of the political crisis and/or failure to address necessary structural reforms will only push this process further out into the future.

Fig. 5A (lhs): EM real GDP before & after currency crises / Fig 5b (rhs): EM stock markets before & after currency crises

Source: Pictet Asset Management, CEIC, Datastream. *Our definition of a currency crisis is where Real trade-weighted exchange rate down more than 10% q/q. By this framework there have been 18 episodes since the early 90s: Argentina (02), Brazil (99), Bulgaria (97), Colombia (99), Egypt (03), India (93), Indonesia (97), Korea (97), Malaysia (97), Mexico (95), Philippines (97), Romania (99), Russia (98), South Africa (04), Turkey (94 & 02), Ukraine (98)

Nikolay Markov joined Pictet Asset Management in 2013. He is a Senior Economist, Lead on CEE and Other advanced economies.

Before joining Pictet, he was working in the Monetary Policy Analysis Unit of the Swiss National Bank where he performed research on monetary policy rules for Switzerland. Prior to working at the Swiss National Bank he was a teaching and research assistant at the University of Geneva and participated in international academic conferences.

Nikolay holds a PhD in Economics from the University of Geneva and obtained a PhD program certificate from the Swiss National Bank doctoral institute in Gerzensee.

Share this article

Important legal information

This marketing material is issued by Pictet Asset Management (Europe) S.A.. It is neither directed to, nor intended for distribution or use by, any person or entity who is a citizen or resident of, or domiciled or located in, any locality, state, country or jurisdiction where such distribution, publication, availability or use would be contrary to law or regulation. The latest version of the fund‘s prospectus, Pre-Contractual Template (PCT) when applicable, Key Information Document (KID), annual and semi-annual reports must be read before investing. They are available free of charge in English on www.assetmanagement.pictet or in paper copy at Pictet Asset Management (Europe) S.A., 6B, rue du Fort Niedergruenewald, L-2226 Luxembourg, or at the office of the fund local agent, distributor or centralizing agent if any.

The KID is also available in the local language of each country where the compartment is registered. The prospectus, the PCT when applicable, and the annual and semi-annual reports may also be available in other languages, please refer to the website for other available languages. Only the latest version of these documents may be relied upon as the basis for investment decisions.

The summary of investor rights (in English and in the different languages of our website) is available here and at www.assetmanagement.pictet under the heading "Resources", at the bottom of the page.

The list of countries where the fund is registered can be obtained at all times from Pictet Asset Management (Europe) S.A., which may decide to terminate the arrangements made for the marketing of the fund or compartments of the fund in any given country.

The information and data presented in this document are not to be considered as an offer or solicitation to buy, sell or subscribe to any securities or financial instruments or services.

Information, opinions and estimates contained in this document reflect a judgment at the original date of publication and are subject to change without notice. The management company has not taken any steps to ensure that the securities referred to in this document are suitable for any particular investor and this document is not to be relied upon in substitution for the exercise of independent judgment. Tax treatment depends on the individual circumstances of each investor and may be subject to change in the future. Before making any investment decision, investors are recommended to ascertain if this investment is suitable for them in light of their financial knowledge and experience, investment goals and financial situation, or to obtain specific advice from an industry professional.

The value and income of any of the securities or financial instruments mentioned in this document may fall as well as rise and, as a consequence, investors may receive back less than originally invested.

The investment guidelines are internal guidelines which are subject to change at any time and without any notice within the limits of the fund's prospectus.

The mentioned financial instruments are provided for illustrative purposes only and shall not be considered as a direct offering, investment recommendation or investment advice. Reference to a specific security is not a recommendation to buy or sell that security. Effective allocations are subject to change and may have changed since the date of the marketing material.

Past performance is not a guarantee or a reliable indicator of future performance. Performance data does not include the commissions and fees charged at the time of subscribing for or redeeming shares.

Any index data referenced herein remains the property of the Data Vendor. Data Vendor Disclaimers are available on assetmanagement.pictet in the “Resources” section of the footer.

This document is a marketing communication issued by Pictet Asset Management and is not in scope for any MiFID II/MiFIR requirements specifically related to investment research. This material does not contain sufficient information to support an investment decision and it should not be relied upon by you in evaluating the merits of investing in any products or services offered or distributed by Pictet Asset Management.

Pictet AM has not acquired any rights or license to reproduce the trademarks, logos or images set out in this document except that it holds the rights to use any entity of the Pictet group trademarks. For illustrative purposes only.

Cookie Policy

This website uses cookies to enhance user experience and to collect statistical data. You may refuse to accept cookies or change your settings by clicking the following link: Cookies policy. By continuing to browse this website, you accept the use of cookies for the above purposes.