Torn and frayed: the new bond market

Bond markets are not functioning as smoothly as they used to. Sébastien Eisinger and Elena Mendez Fraboulet explain how Pictet Asset Management's fixed income team is adapting to the challenges posed by deteriorating trading conditions.

Liquidity – the ability to buy or sell securities without affecting their price – is said to be deteriorating in bond markets. Do you see signs of this too?

EMF. We see evidence of declining liquidity every day. Our bond traders have fewer counterparties to trade with than they did a few years ago. And, what’s more, those counterparties’ trading books are smaller than they were in the past because of tighter financial regulations.We see evidence of declining liquidity every day.

This means it is more difficult for investment managers to buy and sell bonds at what they would consider to be an attractive price. These problems used to be confined to the high-yield bond markets, but they are now a feature of investment-grade debt, where liquidity used to be taken for granted.

SE. The figures showing how far market infrastructure has weakened are quite remarkable. Before banks were hit with new regulations in 2007, broker-dealer inventories of US corporate bonds – the amount they’d be happy to hold to trade at a future date – were just above USD400 billion.

Now, that figure is closer to USD50 billion. And that fall comes at a time when issuance of bonds among corporations is rising at record pace. Between 2000 and 2008, the volume of new corporate bonds averaged at just under USD800 billion per year. In the years 2009 to 2015, that figure has climbed to USD1.24 trillion.(1)

What changes have Pictet Asset Management made to their investment process to mitigate the risks associated with harsher trading conditions? Have your bond traders acquired a more prominent role, for instance?

SE. Our traders have always had a major role to play in our investment process – their responsibilities have traditionally extended beyond the execution of buy and sell orders. Yet with liquidity becoming harder to source, the traders' role is evolving. It now involves providing portfolio managers with detailed guidance on liquidity so that trade ideas can be assessed for their viability through the lens of available liquidity.

The traders' role is evolving.

Also, traders are making greater use of new technology. The technologies we’re phasing in are helping traders conduct essential pre-trade, in-trade, and post-trade analysis, enabling them to find liquidity in the most efficient and effective way. Traders are also utilising different trading styles to help secure best execution for our clients. This includes using pre-trade platforms, dark trading pools; and algorithmic, or rules-based trading. Using these different styles allows us to be better informed on what strategy works best for particular orders and, hence, our clients.

EMF. Tougher trading conditions have also made it more costly to alter the composition of a portfolio. Our investment managers have adapted in a number of ways. I’d say that managers now tend to change the make-up of their underlying investments less frequently than they used to.

Yet at the same time, and to hedge investments against short-term volatility and to reduce other risks, managers are making greater use of derivatives. These instruments are often more liquid than many types of bond and can be used to alter a portfolio’s sensitivity to changes in interest rates, yield curves or credit market indices.

Credit default swap indices, for instance, are remarkably liquid instruments that offer investment managers a very cost-efficient way of altering the credit beta of a portfolio – or its sensitivity to the shifts in the perceived creditworthiness of corporate borrowers.

So, to summarise, investment managers are holding on to their investments for longer but making better use of liquid derivatives to protect the portfolio from short-term market fluctuations.

What steps are you taking to more accurately measure the liquidity risks inherent in fixed income portfolios?

EMF. When clients ask ‘how liquid are my investments?’, what they are really asking is: ‘what proportion of my investments could I realistically sell, within a reasonable timeframe, without incurring significant trading costs?’

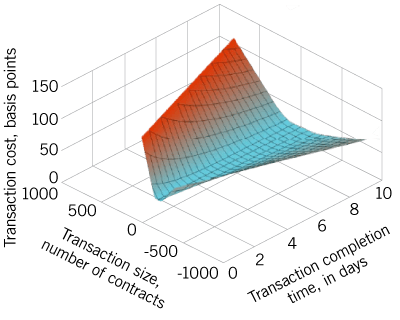

Transaction costs, size and execution

An illustration of the relationship between transaction cost, transaction size and transaction execution time

The fixed income risk team here is working with a new tool that we hope will provide the answer to this complex question. The new model – LiquidityMetrics, developed by MSCI – quantifies portfolio liquidity by estimating the relationship between the size of a transaction and the length and cost of its execution, measured respectively in days and basis points.

In other words, if clients wished to sell some of their invested assets, the model would be able to tell them whether and to what extent the trading cost and execution time would vary according to the size of the intended transaction. All things being equal, the greater the transaction size, the greater the potential cost and the longer the execution time. The most liquid portfolios, then, would be those for whom the transaction size has little or no bearing on trading cost or execution time.

Does the growth of fixed income funds offering daily liquidity make matters worse? And what about the very largest bond funds – do they represent a systemic risk at a time when liquidity is in decline?

SE. Some investment industry experts believe that the growing number of bond funds offering investors daily liquidity – or the ability to liquidate holdings with one day’s notice – threatens to become a source of market instability. There is some truth in that. If some bonds in a certain fund are not liquid enough to trade daily, then does it make sense to offer a client daily liquidity in that fund? I don’t think so. It is a mismatch that can cause problems.

Also, in offering daily liquidity, asset managers must ensure they deliver adequate protection to those clients that do not wish to trade frequently. If one client engages in a large transaction at short notice, that trade could potentially affect the value of the entire portfolio – to the detriment of other clients in the fund. There are a range of anti-dilutive measures to protect a portfolio against this risk, but in some instances those tools are inadequate. So when we believe offering daily liquidity might compromise the investments of those clients who don’t need or want to trade that frequently, then we don’t offer that alternative. We need to act in the interest of all our clients.

Asset managers must ensure they deliver adequate protection to those clients that do not wish to trade frequently.

The thing is you can sell and buy most bonds at short notice – provided you are willing to compromise enough on the price. And it is our duty as investment managers to remind investors of this fact at all times. To the asset management industry’s credit, I think it is beginning to get this message across, but it probably needs to do so even more clearly.

EMF. The popularity of funds offering daily liquidity is not the only problem. The rise of the 'mammoth' bond fund can be too. As recent events have shown, when these funds have to liquidate large positions in less liquid instruments, this causes a lot of market volatility. Not only that, but their sheer size also makes it difficult for them to generate good returns for their investors. So I’d say that poorer liquidity means that asset management companies will probably need to become more disciplined in managing the size of their bond funds. Capacity limits will probably need to be lower. It is something that Pictet Asset Management has taken a very close look at in recent years.

Do you believe electronic trading is viable in bond markets? To what extent does Pictet Asset Management make use of automated trading platforms?

SE. Electronic trade has always been difficult to establish in fixed income. The market does not lend itself easily to electronic trading because there are simply too many fixed income securities. Many of the systems currently in use simply try to bring together investors who are trading in exactly the same security. That is very difficult to do. Yet there is another way, but it will require a change in attitude among market participants as well as heavy investment in technology.

If asset managers want the market to be more liquid in future, they will have to become the price-setters.

What might make for a viable platform is one which allows all members of the fixed income community – that’s both market intermediaries such as investment banks and end investors such as asset managers - to exchange their bid-ask spreads.

To establish such a platform, though, would require asset managers to accept a new role – that of price setter. For too long, the investment management industry has been piggybacking on the liquidity provided by investment banks. It has not really facilitated trade in any meaningful way. But those days are gone.

If asset managers want the market to be more liquid in future, it is they – not the investment banks – that will have to become the price-setters. And that will require new skills.

But the key point to make is that we are in a period of experimentation. We are experimenting with various models and trying to find the one that works best for our fixed income managers and our clients.

So does all this mean that Pictet Asset Management’s fixed income business is venturing into unfamiliar territory?

SE. Not really. Especially when you consider that we have considerable experience in investing in one of Europe’s most illiquid bond markets: Switzerland. There are many lessons that we have learned from investing in Swiss bonds over the years we can now apply to other markets that are experiencing Swiss-like bouts of illiquidity.

When it comes to less liquid bond markets, we know what to expect and how to deal with the problem.

Our experience of managing high-yield and emerging market debt – from the time when these were both niche markets – also puts us in a pretty good position. When it comes to less liquid bond markets, we know what to expect and how to deal with the problem.

A presente comunicação promocional foi preparada por Pictet Asset Management (Europe) S.A.. Não se dirige nem se destina a ser distribuído ou utilizado por qualquer pessoa ou entidade que seja cidadão ou tenha residência, domicílio ou se encontre num local, estado, país ou jurisdição onde tal distribuição, publicação, colocação à disposição ou uso seja contrária à lei ou regulamentação em vigor. Deve ler a última versão do prospeto, o modelo Pré-Contratual quando aplicável, o Documento de informação fundamental e os relatórios anuais e semestrais antes de decidir investir.

Estes documentos estão disponíveis gratuitamente em Inglês, no sitio web www.assetmanagement.pictet ou em suporte papel na Pictet Asset Management (Europe) S.A., 6B, rue du Fort Niedergruenewald, L-2226 Luxembourg, ou ainda nos escritórios do agente local do Fundo, distribuidor ou agente centralizador, se aplicável.

O Documento de informação fundamental também se encontra disponível na língua local de cada país onde o compartimento se encontra registado. O prospeto, o Modelo Pré-Contratual quando aplicável, os relatórios anuais e semestrais poderão estar igualmente disponíveis noutras línguas, consulte por favor o sitio web para saber quais as línguas disponíveis. Apenas a última versão destes documentos pode servir de base para a tomada de decisões de investimento.

Um resumo dos direitos dos investidores (em Inglês e nas differentes línguas do nosso website) está disponíve aqui e em www.assetmanagement.pictet sob a rubrica "Recursos", no final da página.

A lista de países nos quais o Fundo se encontra registado pode ser obtida a todo o tempo da Pictet Asset Management (Europe) S.A., a qual pode decidir pôr termo às formas previstas para a comercialização do Fundo ou compartimentos do Fundo em qualquer desses países.

A informação e os dados apresentados neste documento não poderão ser considerados como uma oferta ou solicitação para comprar, vender ou subscrever quaisquer títulos, instrumentos ou serviços financeiros.

As informações, opiniões e previsões apresentadas neste documento reflectem um parecer à data da sua publicação e estão sujeitas a alterações sem aviso prévio. A Pictet Asset Management (Europe) S.A. não tomou quaisquer medidas no sentido de assegurar que os fundos referidos neste documento se adequam a qualquer investidor em particular e não deverão ser considerados como substituto do exercício de uma avaliação própria e independente. O tratamento fiscal a aplicar depende das circunstâncias específicas de cada investidor e poderá estar sujeito a alterações posteriores.

Antes de tomar uma decisão de investimento recomendamos a todos os investidores que verifiquem se esse investimento é adequado tomando em consideração, nomeadamente, os seus conhecimentos e a sua experiência em termos financeiros, os seus objectivos de investimento e a sua situação financeira e que obtenham aconselhamento profissional adequado antes de tomar qualquer decisão de investimento.

O valor e o retorno dos títulos ou instrumentos financeiros mencionados neste documento podem oscilar para cima ou para baixo e, consequentemente, os investidores poderão não receber a totalidade do valor inicialmente investido.

Estas diretrizes de investimento são diretrizes internas que estão sujeitas a alterações em qualquer altura, e sem aviso prévio, no âmbito do prospeto do fundo. Os instrumentos financeiros mencionados são apresentados com uma finalidade meramente ilustrativa e não poderão ser considerados como uma oferta direta, recomendação ao investimento ou aconselhamento ao investimento. A referência a um determinado título não é uma recomendação para comprar ou vender esse título. As alocações efetivas estão sujeitas a alterações e podem já ter sido alteradas desde a data do material de comercialização.

Rendibilidades passadas não são garantia de rendibilidades futuras. A informação sobre a rendibilidade não inclui comissões e taxas cobradas aquando da subscrição ou resgate das unidades de participação.

Os dados de índices aqui contidos permanecem propriedade do Fornecedor de Dados. As Declarações de Exoneração de Responsabilidade dos Fornecedores de Dados encontram-se disponíveis em assetmanagement.pictet, na secção “Recursos” do rodapé.

Este documento é uma informação de marketing publicada pela Pictet Asset Management e não está abrangido pelos requisitos do MiFID II/MiFIR especificamente relacionados com o research de investimentos. Este material não contém informação suficiente para dar suporte a qualquer decisão de investimento e não poderá ser considerado, por si, como base de avaliação das vantagens de investir em quaisquer produtos ou serviços oferecidos ou distribuídos pela Pictet Asset Management.

A Pictet AM não adquiriu quaisquer direitos ou licença para reproduzir as marcas registadas, logotipos ou imagens apresentadas neste documento, exceto o facto de deter os direitos de utilização das marcas registadas de qualquer entidade do grupo Pictet. Com uma finalidade meramente ilustrativa.