Alternatives are prized by investors. They're also in short supply.

Par

Andrew Cole

Head of Multi Asset London

Partagez cet article

Alternative assets are as prized as blue diamonds. Unfortunately, they’re just as rare – most of what glitters in the investment universe is actually rhinestone.

That’s because for all their perceived distinctiveness, most investments that carry the ‘alternative’ label tend to be made up of fairly ordinary underlying assets. More often than not, their only distinctive features are higher management fees and insufficient compensation for the fact that they are hard to buy and sell.

This shouldn’t be surprising. Most assets tend to behave in the same way because they are influenced by the same fundamentals, such as changes in interest rates and inflation. That’s why we’ve rejected most of the alternatives we’ve looked at.

Yet while true alternatives are hard to find, that doesn’t mean they’re not worth the effort. Particularly today, when bonds and equities tend to move more closely together than in the past.

Holding a separate group of assets that follow their own independent course is the sort of diversification that makes investors less vulnerable to broad macroeconomic forces.

And even if pure alternatives aren’t available, finding ones that have the right mix of bond- and equity-like characteristics can also help – as long as they come at an attractive price. A key asset allocation skill is not to overpay for diversification. Expensive assets are a drag on portfolio returns regardless of whether they move in lockstep with the broader market or not.

Just wearing fancy dress?

A close look at property highlights some of the problems investors face when assessing alternative investments. Property comes in two forms: a building site and the final construction. Owning a building site is much like owning stock in a high-growth company with the expectation that the return will come in the form of a capital gain. Meanwhile, the finished building broadly acts like a debt instrument, the main difference being that its coupons are called rents. So it’s not an alternative in the sense that it isn’t immune to the traditional driving forces of bonds and equities.

But that’s not to say property does not offer investors diversification. It can protect against inflation and has contractual cash flows that aren’t necessarily fully synchronised with traditional asset classes.

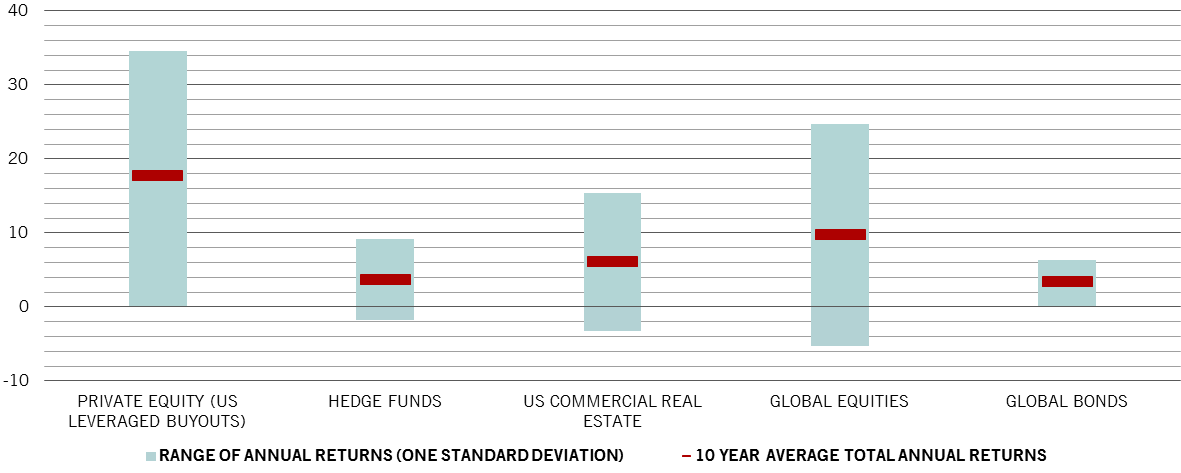

a volatile universe

Comparing the range of long-term returns for alternative and traditional asset classes

Source: Datastream, MSCI, JP Morgan, Prequin, HFRX, NCREIF. Returns are indicative and are based on indices that may be hypothetical. Data covering period 20.03.2008-20.03.2018 except for commercial real estate which is to 31.12.2017.

Private equity is an asset class that gains from the fact that debt has tax advantages. It’s an investment best suited to long-term stable institutional pools of capital, like endowments and sovereign wealth funds, which can take advantage of the extra returns available as a trade-off for locking up money over long periods.

Elsewhere, there are infrastructure assets – such as toll roads, airports or hydro-electric projects. But because they’re typically contracts with the public sector, they end up mimicking the public bond market, albeit with lower liquidity and higher fees. Nor do they offer the prospect of equity-like capital gains.

Expensive alternatives and those that aren't even assets

Many investors are attracted to alternatives like artworks, wine, stamps, diamonds, rare cars etc. But these are, in fact, speculative assets. The decision to buy tends to be based on the expectation that someone will pay a higher price at a later date for something with no obvious intrinsic economic value. And they’re often hard to handle. Selling a portfolio of these assets can take many months and considerable legwork – all the while incurring significant insurance and storage costs.

Alternatives like artworks, wine, stamps, diamonds, rare cars etc. are, in fact, speculative assets.

As for commodities, not only do we not see them as alternatives, we don’t even regard them as long-term assets. There’s no evidence that commodity prices rise over time. In fact, technological improvements – be they more efficient machinery, better processes or something like the mid-20th century’s Green Revolution, when thanks to scientific innovation and technology, agricultural productivity rocketed – have generally contributed to a downward trend in long run commodity prices.

What’s more, commodities are often liabilities. Take timber. It generates no income, you have to pay to store and insure it and, over time, it rots. Forests, on the other hand, are assets. Investors can choose the pace at which trees are harvested and planted as well as the species mix, whether slow growing deciduous or fast evergreen.

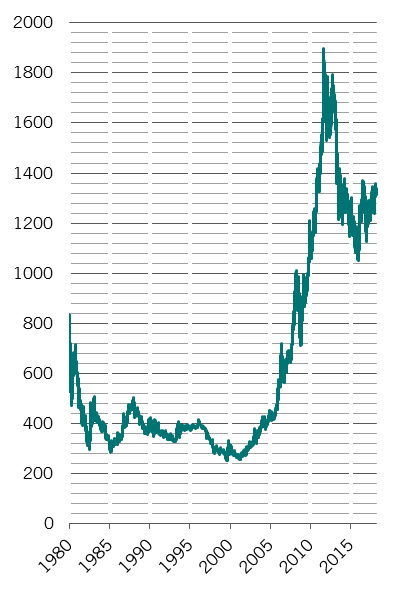

Glittering gold

Gold is also interesting.

Bullionaires

Gold price, dollars per ounce

Source: Bloomberg. Data covering period 31.12.1979- 22.03.2018.

Not because of its commodity characteristics, but because it acts as a proto-currency. It’s true that, as with other commodities, gold doesn’t generate an income and incurs storage and insurance costs. But it isn’t a wasting asset, doesn’t tarnish and has historically worked as a store of value. And in a time when yields across assets generally are wafer thin or even negative, gold’s lack of income generation stops being a mark against it.

Gold comes into its own when people start to worry about central banks using the printing press to erode away the value of currencies, as well as during times of political turmoil and war. People buy it as a safe haven. Today’s worries about North Korea, the erratic Trump presidency and central banks’ growing balance sheets underscore its attractions as a long-term investment.

Research has shown that it also works as a hedge against stocks during normal market conditions.1 Which is to say that it works as a portfolio diversifier.

Valuing alternatives

Overall, most assets labelled “alternative” aren’t when looked at closely, they behave just like conventional assets. But there are some viable options available. The big question investors need to ask is whether the returns are sufficient to compensate for these assets’ typical lack of liquidity. What’s most important to remember is that whether the asset you buy is conventional or “alternative”, the price you pay for an asset will have a meaningful impact on your ultimate return.

A propos de

Andrew Cole

Andrew Cole a rejoint Pictet Asset Management en 2014. Il dirige l’équipe Multi Asset à Londres et peut s’appuyer sur plus de 40 ans d’expérience en investissement. Andrew a commencé sa carrière en 1979 et a rejoint le département des obligations mondiales de Baring Asset Management en 1986. Depuis 2001, il gère des portefeuilles multi-actifs avec un objectif de performance absolue. Il a été nommé Head of Multi Asset London en 2017. Andrew siège au sein des groupes de recherche Macroéconomie et Valorisation. Il est aussi membre avec droit de vote de la PSU, le comité d’investissement senior de Pictet Asset Management, qui est responsable de définir la politique d’allocation d’actifs.

La présente documentation marketing est publiée par Pictet Asset Management (Europe) S.A. Elle n’est pas destinée à des personnes physiques ou morales qui seraient citoyennes d’un Etat, ou qui auraient leur domicile ou leur résidence dans un lieu, un Etat ou une juridiction où sa publication, sa diffusion, sa consultation ou son utilisation seraient contraires aux lois ou aux règlements en vigueur. Avant tout investissement, il convient de lire les dernières versions du prospectus, du modèle précontractuel le cas échéant, du Document d’information clé ainsi que des rapports annuel et semestriel du fonds, disponibles en anglais et sans frais sur le site assetmanagement.pictet ou sous forme imprimée auprès de Pictet Asset Management (Europe) S.A., 6B, rue du Fort Niedergruenewald, L-2226 Luxembourg, et de l’agent local, du distributeur ou de l’agent centralisateur du fonds, le cas échéant.

Le Document d’information clé est en outre disponible dans la ou les langues nationales de chacun des pays où le compartiment concerné est enregistré. De même, le prospectus, le modèle précontractuel le cas échéant ainsi que les rapports annuel et semestriel sont susceptibles d’être publiés dans d’autres langues, pour lesquelles il convient de consulter le site susmentionné. Seules les dernières versions des documents visés ci-dessus peuvent être considérées comme des publications officielles sur lesquelles fonder les décisions d’investissement.

Le résumé des droits des investisseurs est disponible (en anglais et dans les différentes langues de notre site internet) ici et sur www.assetmanagement.pictet sous la rubrique "Ressources", en pied de page.

La liste des pays où le fonds est enregistré peut être obtenue en tout temps auprès de Pictet Asset Management (Europe) S.A., qui peut décider de mettre fin aux dispositions prises dans le cadre de la commercialisation du fonds ou de ses compartiments dans un pays donné.

Les informations ou données contenues dans le présent document ne constituent ni une offre, ni une sollicitation à acheter, à vendre ou à souscrire à des titres ou à d’autres instruments ou services financiers.

Les informations, avis et évaluations qu’il contient reflètent un jugement au moment de sa publication et sont susceptibles d’être modifiés sans notification préalable. La société de gestion n'a pris aucune mesure pour s'assurer que les fonds auxquels faisait référence le présent document étaient adaptés à chaque investisseur en particulier, et ce document ne saurait remplacer un jugement indépendant. Le traitement fiscal dépend de la situation personnelle de chaque investisseur et peut faire l’objet de modifications.

Avant de prendre une décision d'investissement, il est recommandé à tout investisseur de vérifier si cet investissement est approprié compte tenu, notamment, de ses connaissances et de son expérience en matière financière, de ses objectifs d'investissement et de sa situation financière, ou de recourir aux conseils spécifiques d'un professionnel de la branche.

La valeur et les revenus tirés des titres ou des instruments financiers mentionnés dans le présent document peuvent fluctuer à la hausse ou à la baisse, et il est possible que les investisseurs ne récupèrent pas la totalité du montant initialement investi.

Les directives d’investissement sont des directives internes susceptibles d’être modifiées à tout moment, sans préavis, dans le respect des limites précisées dans le prospectus du fonds. Les instruments financiers auxquels il est fait référence sont mentionnés uniquement à des fins d’illustration et ne sauraient être considérés comme une offre commerciale directe, une recommandation de placement ou un conseil en placement. La référence à un titre particulier ne constitue pas une recommandation d’achat ou de vente du titre en question. Les allocations existantes sont sujettes à modification et peuvent avoir évolué depuis la date de publication initiale de la documentation marketing.

La performance passée ne saurait préjuger ou constituer une garantie des résultats futurs. Les données relatives à la performance n’incluent ni les commissions, ni les frais prélevés lors de la souscription à des ou du rachat de parts.

Toute donnée relative à un indice figurant dans le présent document demeure la propriété du fournisseur de données concerné. Les mentions légales des fournisseurs de données sont consultables sur le site assetmanagement.pictet, sous la rubrique «Ressources», en pied de page.

Ce document est une communication marketing publiée par Pictet Asset Management. Il n’est pas visé par les dispositions de la directive MiFID II et du règlement MiFIR se rapportant expressément à la recherche en investissement. Il ne comporte pas suffisamment d’informations pour servir de fondement à une décision d’investissement. Vous ne devriez dès lors pas vous appuyer sur son contenu pour examiner l’opportunité d’investir dans des produits ou des services proposés ou distribués par Pictet Asset Management.

Pictet AM n’a acquis ni droits ni licences l’autorisant à reproduire les marques, logos ou images figurant dans le présent document, mais détient le droit d’utiliser les marques des entités du groupe Pictet. Uniquement à des fins d’illustration.

Politique en matière de cookies

Les cookies utilisés sur ce site ont pour finalité de faciliter la navigation ainsi que de récolter des données dans un but statistique. Vous trouverez plus d’informations ainsi que la possibilité de vous y opposer ou de changer les paramètres en cliquant sur le lien suivant: Politique en matière de cookies. En poursuivant votre navigation sur ce site, vous acceptez l'utilisation de cookies aux fins susmentionnées.